Expert Speak | 19 June, 2026

The Japan–EU Offshore Wind Opportunity

Spotlight:

- Offshore wind has emerged as a strategic priority for both Japan and the European Union (EU), two resource-poor regions striving to reduce reliance on fossil-fuel, advance decarbonisation, and shield their economies from recurring energy shocks.

- Both regions face structurally similar challenges— rising costs, auction failures, and supply-chain dependence on China— strengthening the case for cooperation rather than protectionism.

- Joint development of supply-chains for wind turbines, permanent magnets, and HVDC infrastructure could bolster resilience in both regions, with benefits extending to industrial consumers and economies across the wider Indo-Pacific.

Both the EU and Japan identify offshore wind as a key component of their decarbonisation strategies with ambitious deployment targets. The EU aims to install 86–89 GW of offshore wind capacity by 2030 and 355 GW by 2050 while Japan targets achieving 10 GW by 2030 and 45 GW by 2040.

The offshore wind industry is grappling with inflationary pressures, rising financing costs, and challenges related to auction design, contributing to a wave of cancellations.

However, both regions are falling behind. The offshore wind industry is grappling with inflationary pressures, rising financing costs, and challenges related to auction design, contributing to a wave of cancellations. These include Vattenfall’s 1.4 GW Norfolk project in the United Kingdom (UK), or Ørsted’s Ocean Wind 1 and 2 projects in the United States (US). Multiple auctions have attracted insufficient bids or none at all, as seen in the UK’s 2023 Allocation Round 5, in Denmark in 2024, and in the Netherlands, Lithuania and Germany in 2025. In the EU, an estimated 9 GW of auctions scheduled for 2025 either failed or were postponed. Recently, TotalEnergies communicated that it is seeking to quit a major offshore wind energy project in Germany.

Similarly, in 2021, a Mitsubishi-led consortium won development rights for three offshore wind projects totalling 1.7 GW in Japan’s inaugural auction. By February 2025, the company recorded a ¥522 billion impairment loss after costs more than doubled amid inflation, yen depreciation, and rising turbine and supply-chain costs; exposing the vulnerability of an auction design in which low bids offered no buffer against cost escalation.

By end-2025, the EU had installed 21.5 GW; Japan had reached only 253.4 MW.

Between 2020 and 2024, average offshore wind construction costs in Japan rose by roughly 20 percent, while turbine costs increased by 10–15percent between 2021 and 2023. Similar trends were observed in Europe, where capital costs rose 18 percent between 2019 and 2024.

In response, countries have begun reconsidering their auction designs. The Japanese government revised core auction guidelines to address speculative low bidding and project delays. Under the new rules, developers may reflect up to 40 percent of cost inflation in electricity prices between the auction award and the start of construction. Evaluation criteria also shifted beyond price to include project feasibility and local contributions. European markets, meanwhile, have moved toward two-sided Contracts for Difference providing long-term price certainty. At the same time, Japan is institutionalising a more state-coordinated model of offshore wind development, with centralised site investigations and coordinated transmission capacity.

As Japan advances toward large-scale deployment, it encounters many of the same market challenges faced by Europe’s more mature sector.

Both regions are thus at a shared moment of reassessment. As Japan advances toward large-scale deployment, it encounters many of the same market challenges faced by Europe’s more mature sector. While industrial policy and protectionist measures are experiencing a global revival, this article argues that the convergence of high ambition and structural constraint makes Japan–EU cooperation strategically significant for both regions.

Revival of Industrial Policy

The sector is rapidly adapting to new geopolitical realities. The second Trump administration has initiated a domestic “war on wind”, while China is consolidating its position as the dominant global player. In 2024, China commissioned 50 percent of offshore wind capacity installed worldwide— approximately 41.8 GW.

Although Chinese original equipment manufacturers (OEMs) have primarily served their vast domestic market, European OEMs have long dominated international offshore wind supply chains, albeit with heavy reliance on Chinese components. Now, Chinese manufacturers are increasingly expanding into international markets, including Europe and Japan, exerting competitive pressure on long-established European OEMs. Mingyang, for example, supplied turbines for the Nyuzen offshore wind project in Japan and secured a deal to produce and supply turbines in Italy.

To safeguard Europe’s clean-tech manufacturing base, the second von der Leyen Commission has placed industrial policy at the core of its agenda, with a clear focus on China. Under the Foreign Subsidies Regulation, the EU investigated Chinese wind turbine manufacturers in five markets, opening an in-depth investigation into Goldwind’s wind activities in Europe. The Net-Zero Industry Act (NZIA) introduced a resilience-based non-price criterion for renewable-energy auctions, explicitly referencing the People’s Republic of China in its implementing regulation. The Commission’s proposal for an Industrial Accelerator Act represents the latest initiative to reduce Europe’s dependence on Chinese supply-chains.

Japan has similarly integrated offshore wind into a broader industrial policy framework. Its “Vision for Offshore Wind Power Industry”, targets 60 percent domestic supply-chain content by 2040, prioritises the localisation of foundations, towers, cables, and installation services, even as Japan continues to rely on foreign turbine technology.

Much of Japan’s coastal and offshore seabed exceeds the 50–60 metre depth threshold suitable for bottom-fixed turbines, meaning that achieving national targets will depend heavily on the commercial maturation of floating offshore wind.

In January 2025, the government awarded ¥12.6 billion in subsidies to five companies under the GX Supply Chain Construction Support Project, aimed at strengthening offshore wind supply chains, particularly for floating wind technologies.

Offshore wind is thus increasingly viewed not only as a decarbonisation technology but also as a strategic industrial sector.

Japan–EU Collaboration

At the 2025 EU–Japan Energy Dialogue, the European Commission and Japan’s Ministry of Economy, Trade and Industry (METI) reaffirmed their commitment to deepen cooperation on clean energy supply chains, including wind power, solar, hydrogen, and related technologies .

This engagement builds on the broader EU–Japan Strategic Partnership Agreement 2025, a framework for energy and industrial cooperation under which the EU–Japan Green Alliance supports joint action on offshore wind, carbon pricing, and other clean energy initiatives.

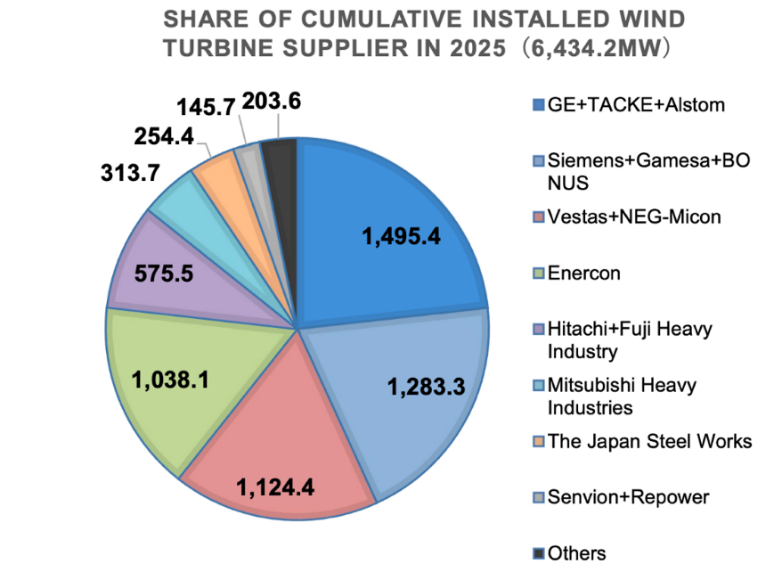

European players view the Japanese offshore wind market as an avenue for future growth. Japan’s METI has established cooperation frameworks with Siemens Gamesa and Vestas to support the development of offshore wind supply chains and domestic manufacturing capacity, public–private initiatives that integrate European turbine expertise with Japan’s industrial and energy objectives. These partnerships further strengthen the position of European manufacturers as key suppliers of wind turbines in Japan. The market is also strategically important for major European developers such as RWE and Ørsted, and marine engineering firms including Jan de Nul and DEME. Crucially, these opportunities are typically pursued in collaboration with local stakeholders, contributing to the development of Japanese know-how and reinforcing domestic supply chains.

Source: JCWA, 2026

Japan likewise plays an important role in the European offshore wind sector. Japanese firms, including JERA Nex bp and Sumitomo, are active participants in the European market. Furthermore, Japan hosts major players in high voltage direct current (HVDC) system manufacturing, such as Hitachi Energy and Sumitomo Electric.

Whether the focus is policy design, supply-chain anchoring, or project execution, both sides are increasingly engaging not merely as individual markets but as strategic partners navigating a rapidly evolving global energy landscape.

Beyond direct project development, Japan can support the EU’s ambition to diversify its supply chain under the NZIA. One example concerns permanent magnets for wind turbines, which were included in the cooperation agreements with Siemens Gamesa. Similarly, the Vestas memorandum outlines collaboration with Nippon Steel to supply steel for wind tower production across Europe, Asia, and Japan.

Whether the focus is policy design, supply-chain anchoring, or project execution, both sides are increasingly engaging not merely as individual markets but as strategic partners navigating a rapidly evolving global energy landscape.

Way Forward

Japan’s evolving policy toolkit: centralised surveys, grid coordination, and auction redesign, signals a move toward state-enabled market shaping, that echoes trends already visible in Europe. Meanwhile, industrial partnerships and cross-investment flows suggest that the future offshore wind landscape will be defined less by isolated national strategies and more by interconnected regional ecosystems.

Yet translating this potential into deeper cooperation will require addressing several structural barriers. Maritime cabotage rules offer a concrete illustration. Japan’s coastal shipping regime restricts domestic transport to Japanese-flagged vessels, which at scale will constrain access to international installation fleets and add material project costs.

While the EU introduces protectionist measures such as EU-made criteria, it continues to keep the door open to partners that share similar values and strategic objectives. Japan’s parallel efforts to localise elements of the offshore wind supply chain while maintaining openness to foreign technology providers reflect a comparable balancing act between industrial competitiveness and international collaboration.

Collaboration beyond project investment could extend to joint supply-chain development, technology partnerships in floating offshore wind, and coordination on regulatory frameworks that reduce non-trade barriers affecting project development

In this context, three areas of collaboration stand out:

- Turbine technology: Europe’s OEMs, principally Siemens Gamesa and Vestas, possess the offshore engineering depth that Japan still needs to develop at scale, and deepening these technology transfer arrangements would accelerate Japan’s deployment while sustaining demand for European manufacturers.

- Permanent magnets: Japan’s advanced materials industry offers the EU a credible diversification pathway beyond Chinese rare-earth supply chains, supporting the resilience objectives of the Net-Zero Industry Act.

- HVDC infrastructure: With mounting supply chain pressure on HVDC systems, collaboration between leading European and Japanese firms could play a significant role in easing bottlenecks that threaten deployment timelines on both sides and limits grid infrastructure development across the wider Indo-Pacific.

Together these three define a cooperation agenda that is complementary rather than competitive.

At the 7th EU-Japan High-Level Economic Dialogue, both sides reaffirmed joint work on strengthening supply chains in clean energy, including offshore wind. Project economics, supply-chain volatility, and policy recalibration will continue to shape deployment speed in both Japan and the EU. For industrial consumers and economies across the Indo-Pacific, many of which face their own offshore wind ambitions and similar supply-chain vulnerabilities, a stronger Japan–EU industrial base offers an alternative sourcing ecosystem and a potential template for supply-chain cooperation that does not depend on Chinese manufacturing dominance. How Japan and Europe navigate this transition, whether together or in parallel, will help determine not only the future of offshore wind, but also the architecture of the global energy transition itself.

This analysis draws on the authors’ contribution to the BE-WISE Research Project, full paper can be accessed here.

Parul Bakshi is Fellow, Energy and Climate, ORF Middle East.

Simon Rogissart is PhD Researcher, Ghent Institute for International and European Studies, Ghent University