Special Reports | 06 June, 2026 Download Report (PDF)

Pathways to Green Steel: Trilateral Opportunities for India, Japan, and South Korea

Steel is among the world's most emissions-intensive and hard-to-abate industries, yet it remains indispensable to economic development and green-technology infrastructure alike. This report examines how India, Japan, and South Korea, collectively the largest group of advanced steel producers outside China, can leverage their complementary industrial strengths to accelerate the transition to low-carbon steelmaking. Drawing on an assessment of key production technologies, supply-chain readiness, and evolving policy frameworks, the report argues that a structured trilateral approach can offer a viable pathway for advancing steel decarbonisation by harmonising certification standards, enabling technology transfer, and mobilising investment at scale. Coordinated action across these three economies would strengthen Indo-Pacific supply-chain resilience and position the region as a leader in industrial decarbonisation.

Attribution: Parul Bakshi and Krishna Vohra, Pathways to Green Steel: Trilateral Opportunities for India, Japan, and South Korea, Observer Research Foundation, June 2026.

Introduction

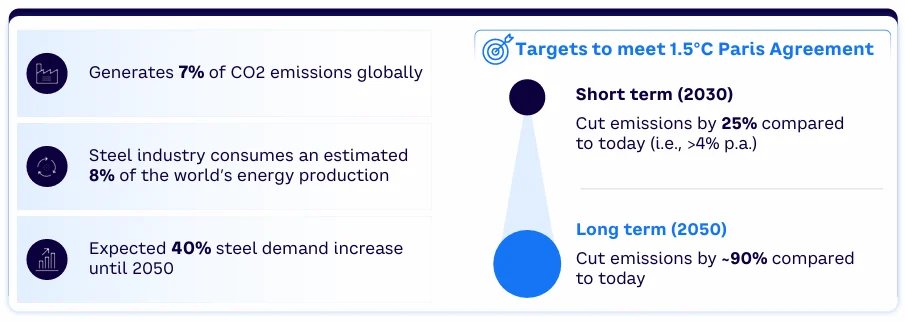

Steel sits at the centre of both, global industrialisation and decarbonisation. It is indispensable to economic development but remains one of the world’s highest-emitting and hardest-to-abate sectors because of the high CO₂ emissions embedded in its manufacturing process. Globally, the steel industry accounts for approximately 7 percent of total CO₂ emissions, producing 2.8 gigatonnes of CO₂ annually.[1] The emission intensity per tonne of finished steel increased by 1.8 percent between 2019 and 2023, reflecting both the scale and urgency of decarbonising this sector.[2]

The indispensability of steel spans nearly every economic sector, including green-technology applications (such as wind turbines, EVs, and solar infrastructure), with global demand projected to reach nearly 2.5 billion tonnes by 2050.[3] This underscores the need for targeted decarbonisation of steelmaking, driven by evolving global policy regimes, rising net-zero commitments under the Paris Agreement, and growing investor pressure.

Figure 1: Global Steel Sector and Decarbonisation Targets

Source: Arthur D. Little[4]

“Green steel” is broadly defined as steel produced with significantly lower CO₂ emissions than conventional steelmaking. This is achieved by substituting fossil fuels with low-carbon or renewable energy sources and by deploying carbon-reduction technologies.[a]

Different certification standards and taxonomies agree that green steel involves measurable reductions in greenhouse-gas emissions over the production process. These reductions are often quantified through emissions-intensity targets ranging from 0.05 to 0.4 tonnes of CO₂ per tonne of steel, depending on the production pathway and scrap content.[5]

At the same time, carbon-pricing and trade mechanisms are injecting new urgency into this transformation. The European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM), for example, will require steel exporters to the EU to report embedded carbon and eventually pay for it unless they adopt low-emission technologies. This regulatory push means that both large steel producers and Micro, Small, and Medium Enterprises (MSMEs) will need to decide whether to decarbonise or risk exclusion from key export markets.

This decarbonisation imperative is further complicated in the Indo-Pacific by structural market imbalances. The region faces dual pressures: chronic overcapacity and a surge in low-cost imports, particularly from China and Southeast Asia, which are destabilising domestic steel markets.[6] Because of the sheer scale of China’s steel industry, which accounted for 46 percent of global steel capacity in 2024,[7] even marginal shifts in its domestic production cascade into global oversupply, depressing prices and placing heavy competitive pressure on neighbouring producers. Several countries, such as Australia[8] and Taiwan,[9] have already adopted defensive trade measures in response to steel dumping from China, underscoring the systemic nature of the challenge. Indeed, China’s persistent overcapacity and aggressive export pricing have become a unifying catalyst for major Indo-Pacific steel producers—India, Japan, and South Korea—driving deeper alignment on trade safeguards, low-carbon steelmaking, and supply-chain diversification.

In India, the consequences are already visible. An October 2025 Reserve Bank of India (RBI) report found that low-priced imports have increasingly displaced domestic production, with nearly 45 percent of inbound steel sourced from South Korea (14.6 percent), China (9.8 percent), the US (7.8 percent), Japan (7.1 percent), and the UK (6.2 percent). The report also noted a sharp surge in shipments from China, Japan, South Korea, Indonesia, and Vietnam in 2024–25.[10]

With subdued domestic demand and rising import competition, India imposed a safeguard duty on the import of flat steel products in December 2025.[11] Market analysts expect these measures—designed to protect domestic industries from serious injury caused by sudden surges in imports—to suppress imports and push domestic steel prices upward.[12]

These challenges add urgency to the Indo-Pacific’s decarbonisation push while simultaneously derisking the supply chain and positioning new industrial ecosystems. For policymakers, this means that decisions on technology choices, financing models, and international partnerships will shape the competitiveness of the region’s steel sector for decades ahead.

India, Japan, and South Korea collectively represent the largest group of advanced steel producers outside China, giving them strategic weight in shaping green-steel markets. Yet each faces distinct, though complementary, pressures, making this an opportune moment to pursue trilateral alignment that supports both industrial growth and decarbonisation goals.

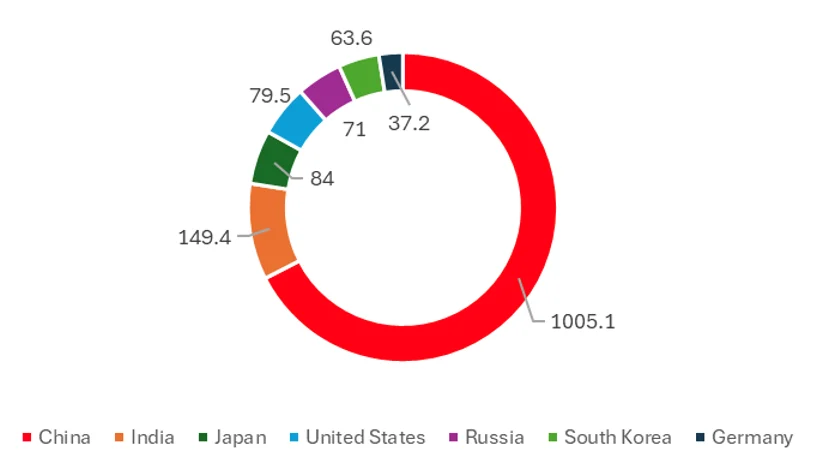

Figure 2: Global Crude Steel Production (2024, in Million Tonnes)

Source: Authors’ own, based on World Steel Association data.[13]

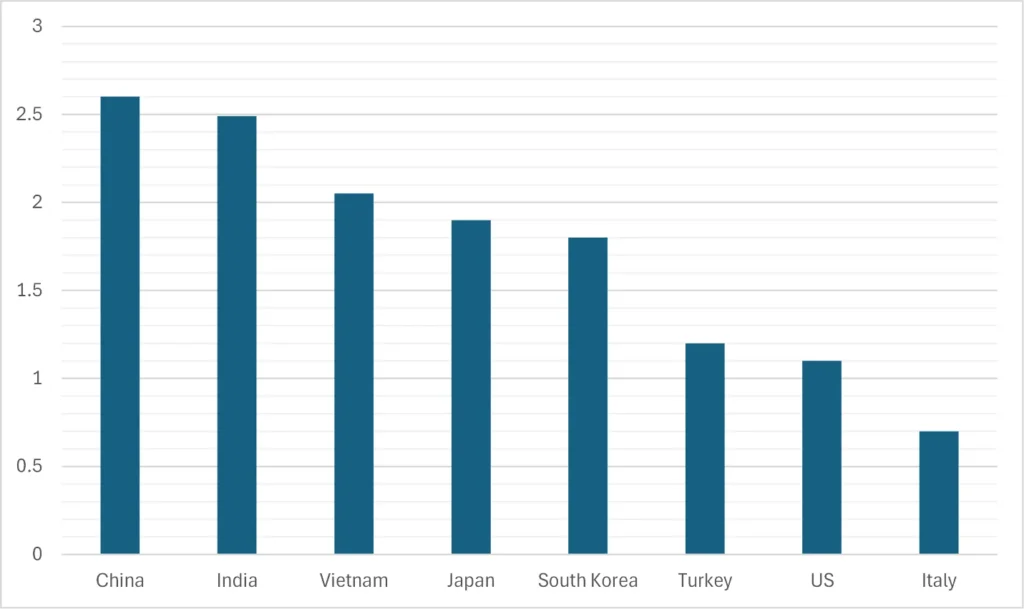

Figure 3: Overall Emission Intensity per Tonne of Crude Steel Produced

Source: Authors’ own, based on Global Efficiency Intelligence data.[14]

Note: In tonnes of CO2 equivalent/tonne of crude steel manufactured (t-CO2e/tcs)

Recent technological advances are also coming into sharper focus, from hydrogen-based direct-reduction processes to carbon-capture installations in blast furnaces. These tools offer pathways to a more sustainable future, but their deployment will require major investment, coordination, and policy coherence. Understanding the current technological landscape and the supply-chain realities that shape what is feasible today versus over the next decade is therefore essential before evaluating the policy instruments and partnerships that can accelerate decarbonisation.

This report examines the state of green-steel technologies, supply-chain readiness, and production pathways; evaluates opportunities for India–Japan–South Korea trilateral cooperation; and outlines practical policy options for governments, industry, and development partners. By situating India’s emerging green-steel landscape alongside Japan’s and South Korea’s technological depth and industrial-scaling capabilities, it illustrates how a structured trilateral approach can unlock shared economic gains, enhance supply-chain security, and accelerate the region’s broader decarbonisation agenda. It also assesses how such coordinated diplomatic engagement can strengthen investment flows, technology transfer, and industrial resilience across the Indo-Pacific.

State of Technology: Supply Chain and Methods of Production

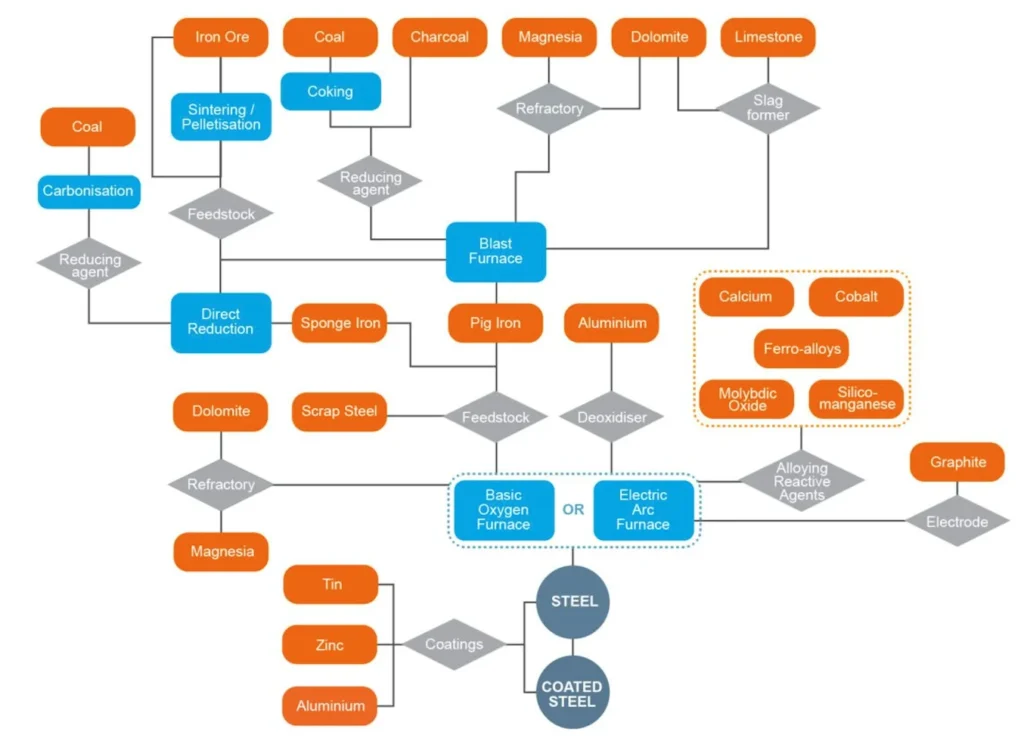

The steel supply chain is complex and resource-intensive, spanning the mining and transport of iron ore and coal, raw-material processing, ironmaking, steel conversion, casting, and downstream fabrication and distribution. Conventional steel supply chains are built around coal, coke, and fossil-fuel–based energy inputs, resulting in high baseline emissions across all stages of production.

Figure 4: Simplified Steel Industry Supply Chain Model

Source: World Steel Association.[15]

Transitioning to “green steel” requires reconfiguring these supply chains to support renewable electricity, hydrogen production and distribution, and robust scrap-recycling logistics for a circular economy.

Today, the steel industry is dominated by two primary technologies: the blast furnace–basic oxygen furnace (BF–BOF) route and the electric arc furnace (EAF) route. Decarbonisation potential varies sharply between these pathways, making upstream energy sourcing, feedstock quality, and scrap availability as important as the plant-level technologies themselves.

BF–BOF Route

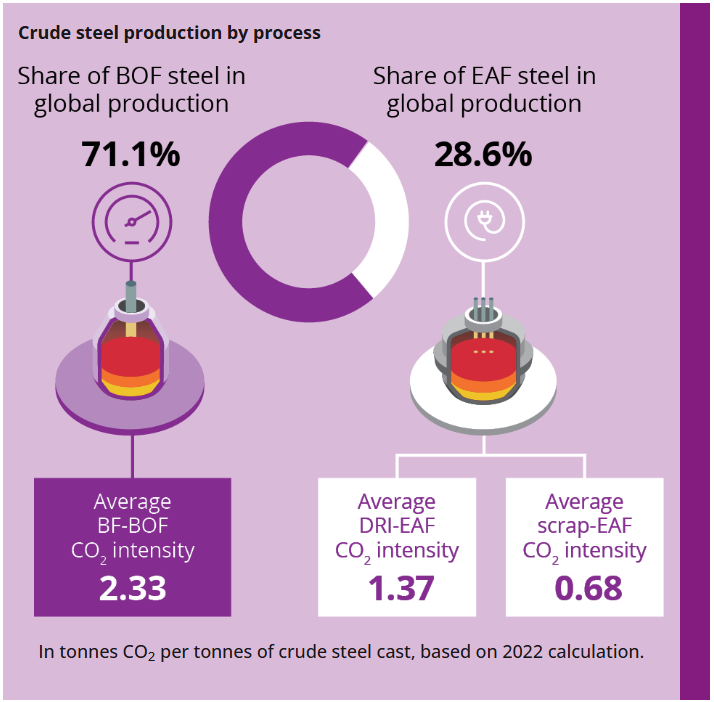

The BF–BOF route begins with the reduction of iron ore to pig iron using coke in a blast furnace, followed by refining in a basic oxygen furnace. This pathway accounts for over 70 percent of global steel production. After China, the largest BOF operators[16] are India (82 mtpa), Japan (77 mtpa), and South Korea (53 mtpa).[17]

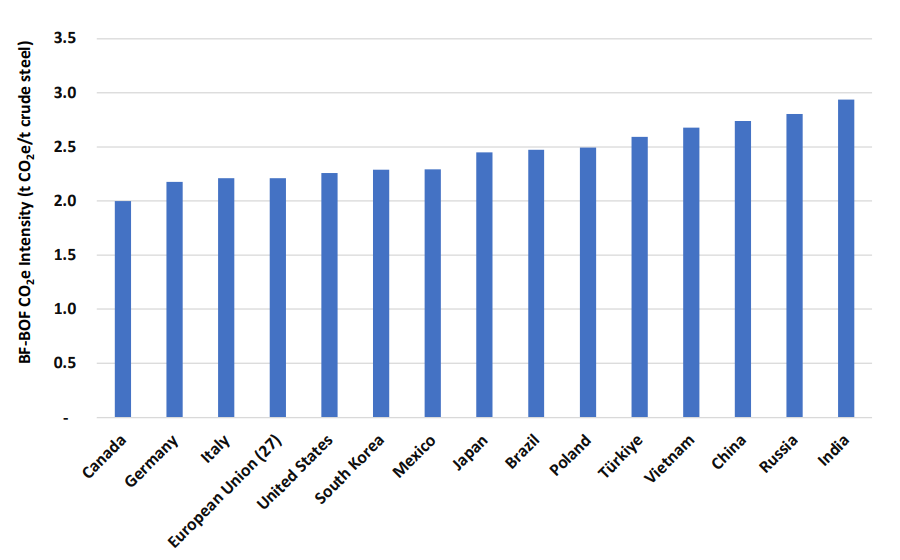

Globally, the emission intensity of this pathway averaged about 2.3 tonnes of CO₂e per tonne (tCO₂e/t) of crude steel in 2023.[18] India is typically higher, ranging from 2.5 to 3 tCO₂e/t, largely due to lower-grade ore, less efficient plants, and higher dependence on fossil-fuel inputs. Japan and South Korea have estimated emission intensities of 2.3 and 2.4 tCO₂e/t, respectively.[19] This entrenched process is the focal point for decarbonisation efforts due to its extremely high baseline emissions.

Figure 5: Average BF-BOF CO₂e Intensity

Source: Hasanbeigi, Steel Climate Impact 2025[20]

EAF Route

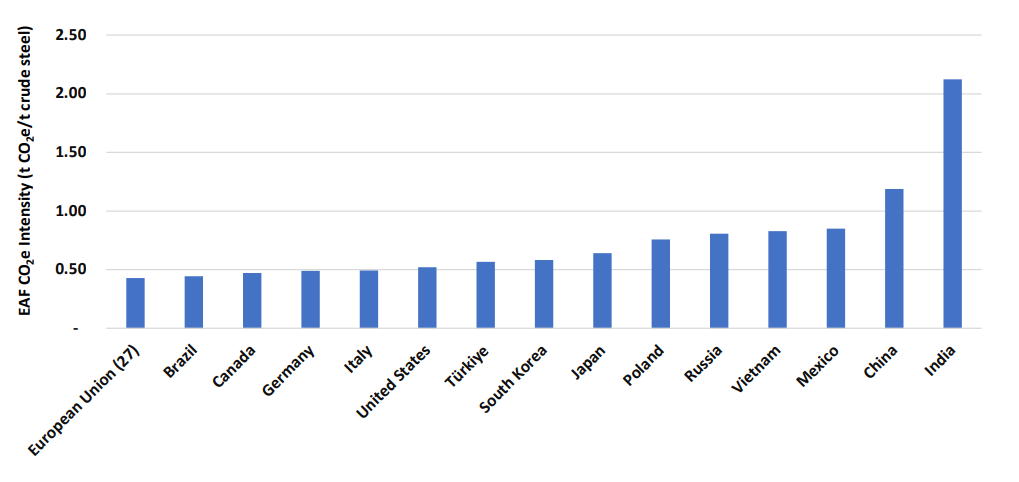

EAFs produce steel by using electricity to melt scrap steel and, increasingly, direct reduced iron (DRI).[21] In many mature economies such as the US and Italy, EAFs produce more than 50 percent of steel, reflecting long-standing investment in lower-emission routes.[22] In India, however, the EAF share is currently around 22 percent, with reliance on coal-based DRI.[23] Similarly, Japan’s EAF share stands at approximately 20-25 percent[24] and South Korea’s around 30–35 percent, reflecting continued reliance on BF-BOF plants.[25]

Figure 6: EAF Emission Intensity per tonne of Crude Steel

Source: Hasanbeigi, Steel Climate Impact 2025[26]

DRI-based EAFs can produce high-quality steel with much lower emissions, especially when powered by renewable energy. This route is increasingly viewed as the most scalable transition pathway for countries with strong iron ore reserves, such as India. India’s comparatively higher EAF emission intensity reflects its reliance on coal-based DRI feedstock, a gap that hydrogen-based DRI could substantially close, given the country’s relatively low scrap-EAF share.

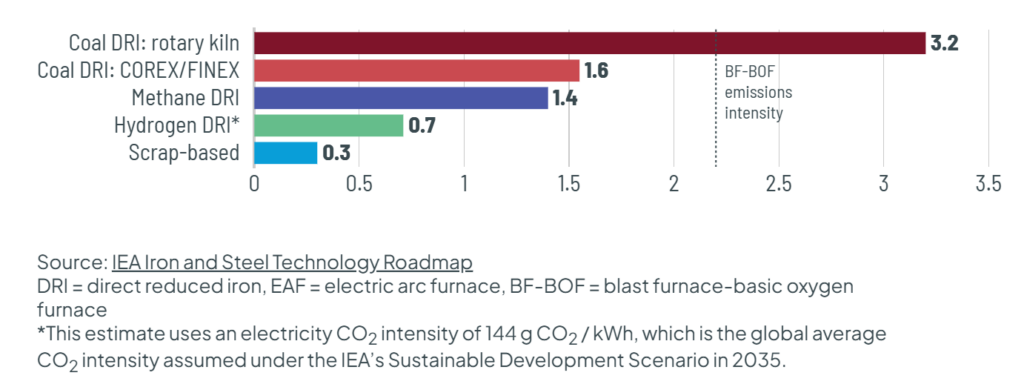

Figure 7: Emissions Intensities of Select EAF Production Routes, in GtCO₂e Per Tonne of Steel

Source: Global Energy Monitor.[27]

Hydrogen-Based DRI

The emergence of green hydrogen as a reducing agent has been central to the pursuit of near-zero-emission steelmaking. When used in the DRI process, green hydrogen can achieve emissions reductions of up to 90 percent compared to BF-BOF production.[28] Industry analyses indicate that green-hydrogen-based DRI can lower emissions intensity from approximately 2.2 tCO₂/t (BF-BOF) to 0.3 tCO₂/t, provided the electricity used for hydrogen and EAF operations is fully renewable.[29]

This pathway is at the core of European initiatives such as HYBRIT[30] (Sweden) and Stegra[31] which demonstrate the technical feasibility of near-zero-emission steel production at industrial scale. India, Japan, and South Korea are all piloting hydrogen-DRI technologies, though at different stages of commercial readiness.

Figure 8: Global BF-BOF and EAF Steel Production and Average Emission Intensity

Source: World Steel Association, 2024[32]

Hydrogen Injection in Blast Furnaces

In contrast, hydrogen injection into blast furnaces delivers only partial emissions reductions. Japan’s COURSE50 and Super COURSE50 programmes, led by Nippon Steel and JFE Steel, have demonstrated 30–33 percent emissions reduction at the blast furnace level.[33] The upper limit of these reductions remains uncertain due to the continued reliance on coke and process-related carbon emissions.

Hydrogen-injection retrofits can extend the operational life of existing blast furnaces, but experts caution that scarce green hydrogen would be more efficiently used in hydrogen-DRI production, where emissions reductions are significantly higher.[34]

Carbon Capture, Utilisation, and Storage (CCUS)

CCUS applied to BF-BOF also functions as a partial-abatement strategy. Current pilots globally show 40–65 percent capture rates, with 90 percent considered a theoretical maximum achievable only in highly controlled conditions.[35]

However, CCUS entails a significant cost premium, high energy demand, and challenges related to transport and storage infrastructure. Operational CCUS capacity in the iron and steel sector stands at just 1.75 million metric tonnes of CO₂ annually, accounting for only 3.9 percent of global CCUS capacity and capturing less than 1 percent of the sector’s fuel-related emissions in 2024.[36]

Nevertheless, for countries with large installed BF-BOF capacity, CCUS remains one of the few retrofit options with meaningful emissions impact.[37]

While the pathways discussed above represent the most widely examined routes for steelmaking, these are not exhaustive. Across the industry, both existing steelmakers and emerging startups are actively exploring low-emission alternatives, including electrolysis-based primary steelmaking and the utilisation of biomass in the BF-BOF route.[38] Most of these innovations remain at pilot or demonstration stage and have yet to be deployed at commercial scale.

Technology Mix in India, Japan, and South Korea

As of 2023, Japan and South Korea predominantly rely on the BF-BOF route, which accounts for roughly 73 percent[39] and 70 percent[40] of their steelmaking processes, respectively, with the remaining 27 percent and 30 percent produced through EAFs. India’s production profile is more technologically varied, with the BOF route accounting for about 42.7 percent of steelmaking, EAFs contributing around 21.9 percent, and the remaining 35.4 percent produced through induction furnaces. Unlike EAFs, induction furnaces use electromagnetic fields rather than electric arcs to melt metal and are typically associated with smaller-scale production.[41] These structural differences reflect variations in industrial structures and access to raw materials.

South Korea’s DRI-EAF share is growing because of strong industrial downstream demand and access to international scrap markets.[42] Japan is also increasing its focus towards EAFs as part of its decarbonisation strategy, led by Nippon Steel, which has announced investments of around US$6 billion by 2029, supported by up to US$1.7 billion in government subsidies to expand EAF capacity.[43] India’s rapidly expanding DRI sector, meanwhile, positions it for hydrogen-DRI leadership once green hydrogen costs fall, though renewable power reliability and grid integration remain key constraints.

A clear understanding of these technology options provides the foundation for analysing how India, Japan, and South Korea are designing policies, incentives, and industrial programmes to scale green steel, while offering insight into where coordinated action or policy alignment could accelerate regional decarbonisation.

India’s Green Steel Policy Landscape and Industrial Transition

India remains among the most carbon-intensive steel producers because of its reliance on the BF–BOF route and coal-based DRI for EAF operations,[44] emitting about 20-25 percent more CO2 per tonne than China.[45] To accelerate decarbonisation, India has announced a suite of policy missions, regulatory reforms, and industrial collaborations, including the allocation of approximately US$2.2 billion towards CCUS technologies in the Union Budget 2026-27.[46]

With the aim of reducing emissions intensity to 2.2 tCO2 per tonne by 2030, India formalised its first Green Steel taxonomy in 2024, establishing a graded certification system based on emissions intensity.[47] The Ministry of Steel (MoS) now issues a “percentage greenness” rating if emissions fall below 2.2 tCO₂e per tonne of finished steel (tfs). [48] The taxonomy defines the following:

- Five-star green-rated steel: emission intensity below 1.6 t-CO₂e/tfs.

- Four-star green-rated steel: emission intensity between 1.6 and 2.0 t-CO₂e/tfs.

- Three-star green-rated steel: emission intensity between 2.0 and 2.2 t-CO2e/tfs.

The taxonomy and rating system demonstrate India’s intent to decarbonise a key hard-to-abate industry while reducing overall emissions. This commitment is reflected in early industry uptake, with ArcelorMittal Nippon Steel India (AM/NS India) becoming the first integrated steel producer in the country to receive a “green steel” certificate under the taxonomy for achieving lower carbon emissions during production.[49]

However, the minimum threshold will need to move closer to the global benchmarks to align India’s net-zero ambitions. For context, India’s threshold for green steel sits slightly above the global average of 1.9 t-CO₂e/tfs, according to the World Economic Forum’s Net-Zero Industries Tracker Report on Steel.[50]

The National Green Hydrogen Mission, launched in 2023, with an outlay of US$2.4 billion, aims to scale domestic green hydrogen production and explicitly targets the replacement of coal-based DRI with hydrogen-based processes in the steel industry.[51] Procurement reforms are also advancing through action plans introduced by the MoS and the Bureau of Indian Standards (BIS).

India’s Strategic Interventions for Green Hydrogen Transition (SIGHT) programme, a core pillar of the National Green Hydrogen Mission, provides roughly US$2.1 billion in incentives to accelerate domestic electrolyser manufacturing and green hydrogen production.[52] Designed to support the Mission’s broader target of 5 million tonnes of annual green hydrogen capacity by 2030, SIGHT aims to shift hard-to-abate sectors such as steel away from coal-based DRI toward hydrogen-based processes.

India has also begun piloting hydrogen-based steelmaking technologies:

- Tata Steel launched India’s first full-scale hydrogen-injection trial at its Jamshedpur blast furnace in 2023, successfully reducing coke consumption and emissions intensity.[53]

- JSW Steel is developing a green hydrogen-DRI pilot at Vijayanagar, targeted for completion by end-2025.[54]

- AM/NS India released its first Climate Action Report outlining a transition toward 100 percent renewable electricity by 2030 and identifying green hydrogen, scrap-EAF expansion, and CCUS as priority pathways.[55]

India’s Steel Scrap Recycling Policy 2019 estimates a requirement of 70-80 MTPA of scrap to achieve its 250 MTPA steel production target by 2030. However, achieving this target will be challenging, as India still relies on scrap steel imports; in FY 2023-24, 25 percent of scrap steel used in production was imported.[56]

Nonetheless, domestic scrap supply is expected to grow with rising steel consumption, particularly from end-of-life vehicles (ELVs), though this will require large-scale processing infrastructure. In line with this shift towards circular steelmaking, Tata Steel has planned capital expenditures of approximately US$1.76 billion for its scrap-based EAF operations in India, the United Kingdom, and the Netherlands in FY 2025-26.[57] Additionally, the MoS has estimated the need for up to 3,000 scrap-collection and dismantling centres nationwide to support expanded EAF capacity.[58]

The Carbon Credit Trading Scheme (CCTS), expected to launch in India in 2026, is emerging as an important near-term policy lever. Even at modest initial levels (US$ 10/tCO₂), carbon pricing simultaneously improves green steel economics while adding costs to high-emission BF-BOF plants. As initial CCTS pricing may be conservative to allow gradual industry adjustment, particularly for MSMEs, there remains a need for complementary support mechanisms such as financial incentives and technical assistance in the near-term.[59]

India’s green hydrogen and green steel outlook reflects a sector on the cusp of rapid transformation. The government has provided a strong foundation of policy backing, and major steel producers have demonstrated a clear willingness to adapt to the standards for low-carbon steel. With targets to expand crude steel capacity to 300 MTPA by 2030 and deploy at least 5 MTPA of green hydrogen by 2030, India is positioning itself as a potential global leader in low-carbon steel production.[60]

However, the commercial viability gap remains substantial. TERI’s financial modelling shows that, under current baseline assumptions, a greenfield hydrogen-DRI-EAF plant faces a negative net present value of approximately US$478 million, compared to a positive US$417 million for conventional BF-BOF production.[61] This viability gap underscores why, despite policy ambitions, no commercial-scale green steel projects have reached a final investment decision in India as of early 2025. Translating these ambitions into widespread decarbonisation will require accelerated action: investment in electrolyser manufacturing, supply chain reforms, and capacity building for both industry giants and MSMEs.

According to TERI’s assessment, India’s reinvestment cycle could provide a critical opportunity to narrow this viability gap. The organisation estimates that 43 million tonnes of existing BF-BOF capacity will require major reinvestment before 2030 to upgrade or replace ageing equipment, presenting a critical near-term window for adopting lower-emission steelmaking pathways. The Hydrogen-based DRI with Electric Smelter Furnace (H₂-DRI-ESF-BOF) configuration emerges as particularly promising for brownfield sites, allowing retention of existing BOF infrastructure while enabling the use of lower-grade iron ore through the electric smelter furnace. TERI highlights that this hybrid approach requires approximately 35 percent less capital investment than greenfield plants (US$980 million vs. US$1,480 million for a 2 Mt plant), while making use of existing auxiliary infrastructure and downstream operations, making it more commercially attractive for existing integrated producers facing reinvestment decisions.[62]

For India’s MSMEs, access to green hydrogen technologies and finance remains a significant barrier. Emissions accounting, technology integration, and compliance with emerging standards are considerably more demanding for smaller firms. This is more pronounced in downstream industries, where enterprises often lack the scale, technical expertise, and capital needed to adapt to new infrastructure and reporting requirements. Ensuring that policy support, incentives, and financing mechanisms effectively reach MSMEs will therefore be critical to a just and broad-based green-hydrogen transition.

India’s ambition is clear, but achieving it will hinge on the pace of industrial modernisation and the coherence of policy support across central and state levels, given that industrial regulation, land allocation, power supply, and infrastructure development are jointly governed and implemented by both tiers of government.

Japan’s Decarbonisation Framework for Green Steel

Japan’s steel industry is moving aggressively toward decarbonisation through a combination of government-driven policy frameworks, large-scale investments, and company-level technology pilots.

Japan’s steel sector is shaped by a structural dependence on imported iron ore; in 2023, it imported 102 million tonnes of ore despite producing 87 million tonnes of steel, reflecting both limited reserves and declining ore quality.[63]

The nation’s Green Transformation (GX) Basic Policy, adopted in 2023, commits the country to a 46 percent reduction in emissions by 2030 and full decarbonisation by 2050, with targeted measures promoting hydrogen utilisation, CCUS deployment, and increased adoption of non-fossil electric arc furnaces.[64] The GX Implementation Council has mobilised an estimated JPY 150 trillion through 2030 to support industrial decarbonisation technologies and associated infrastructure.[65]

Japan’s national GX Emissions Trading System (ETS), set to become fully operational in FY 2026, will introduce mandatory caps for large emitters and allow emissions trading across industrial sectors. The scheme sets a threshold of 100,000 tonnes of CO₂ annually for mandatory participation and is expected to cover 300–400 of Japan’s largest emitting facilities, representing roughly 60 percent of national CO₂ emissions.[66]

Even though sector-specific allocation rules setting process-specific benchmarks (e.g., for blast furnaces, scrap-EAFs, and special steel EAFs) are still being finalised, the ETS is expected to affect all major integrated steel producers, including Nippon Steel, JFE Steel, and Kobe Steel, by requiring verifiable emissions reporting, target-setting, and eventual credit purchases if decarbonisation targets are not met.

Japan is also advancing green public procurement to create predictable demand for low-carbon steel.[67] Japan’s Green Purchasing Act (Act on Promotion of Procurement of Eco-Friendly Goods and Services), introduced in 2001 was one of the world’s first laws mandating that government ministries and agencies prioritise environmentally friendly goods and services. This was amended in January 2025 to extend its scope to steel products, requiring procuring entities to favour low-carbon “green steel.” These measures are intended to stabilise early markets for green steel despite higher production costs, while aligning industry output with emerging global frameworks such as CBAM.

Japan’s steel producers are simultaneously testing technology pathways to reduce emissions from existing assets while preparing for deeper transformation.

- Nippon Steel’s “COURSE50” project (CO₂ Ultimate Reduction System for Cool Earth 50) uses hydrogen injection into blast furnaces to partially replace coke. Commercial trials have achieved ~30 percent emissions reductions while maintaining stable furnace operation.[68]

- The evolving “Super COURSE50” aims to raise hydrogen-injection levels and integrate CCUS, targeting 50 percent or higher reductions, but full decarbonisation remains impossible as long as carbonaceous reductants are used.

- Hydrogen-based direct reduction (H-DRI) is Japan’s long-term pathway. Nippon Steel, JFE Steel, and Kobe Steel are currently exploring pilot-scale H-DRI systems through the Green Innovation in Steelmaking (GREINS) consortium, often in collaboration with global equipment suppliers. Japan’s strategy emphasises ammonia import corridors and large-scale hydrogen carriers as part of its broader energy-security model. [69]

Alongside these technology initiatives, Japan has introduced targeted financial incentives to accelerate industrial decarbonisation. These include a JPY 3 trillion hydrogen contract-for-difference scheme under the Hydrogen Society Promotion Act, 2024, designed to bridge cost gaps between fossil fuels and low-emission hydrogen; capital subsidies covering up to one-third of plant conversion costs in hard-to-abate sectors, and the JPY 2 trillion Green Innovation Fund administered by the New Energy and Industrial Technology Development Organisation to support commercialisation of breakthrough technologies such as hydrogen-based steelmaking and CCUS.[70]

Japan also possesses near-term decarbonisation opportunities through greater utilisation of its existing fleet of scrap-based EAFs, whose operating costs are only about 5 percent higher than BF-BOF production, while delivering emissions reductions of up to 77 percent per unit of output. The country also benefits from a substantial domestic scrap base, with supply totalling nearly 44 million metric tonnes in 2023, around 52 percent of which was used in EAF plants, and 15 percent was exported.[71] This combination of existing EAF capacity, investment plans by Nippon Steel announced in May 2025 to expand EAF capacity, and domestically available scrap suggests considerable potential for expanding scrap-based steelmaking as a complementary and cost-effective pathway to Japan’s longer-term, hydrogen-based transition.

Japan’s decarbonisation trajectory reflects a balance between structural constraints and technological leadership. High electricity prices and ageing assets slow its transition, yet Japan’s cutting-edge research, hydrogen-furnace innovation, abundant domestic scrap base, and CCUS expertise position it as a key architect of Indo-Pacific green-steel standards.

South Korea’s Green Steel Transition

South Korea’s steel sector sits at the centre of its decarbonisation challenge. According to a 2022 Climate Transparency report, the steel sector is the country’s single largest industrial emitter, accounting for approximately 39 percent of industrial emissions and about 13 percent of total national greenhouse gas emissions.[72] This underscores the strategic importance of steel decarbonisation within Korea’s broader industrial and climate-policy framework.

South Korea’s decarbonisation roadmap places a strong emphasis on hard-to-abate industrial transformation, private-sector involvement, and new regulatory pressure. The government has committed to carbon neutrality by 2050, with POSCO and Hyundai Steel designated as national champions to lead the shift toward hydrogen-based steelmaking. Both companies are developing commercial-scale hydrogen direct reduced iron (H2-DRI) plants, with a 300,000-tonne-per-year facility planned for operation by 2030 and supported through public financing instruments.[73]

Under the National Hydrogen Strategy, the government has committed KRW 800 billion (over US$600 million) to develop hydrogen-based steel production, breakthrough technologies, and supporting infrastructure.[74]

Regulatory pressure is rising in parallel. In 2025, the Korean Emissions Trading System (K-ETS) reduced free carbon permit allocations for the steel sector, increasing compliance costs and incentivising deep decarbonisation investments across major steelmakers.[75] These policy signals are reinforced by the ongoing POSCO and Hyundai demonstration projects, which are poised to become major nodes in the Indo-Pacific’s emerging low-carbon steel supply chain.[76]

South Korea is also advancing proprietary technologies aimed at achieving near-zero steelmaking emissions. POSCO’s FINEX process, a hydrogen-rich smelting-reduction technology, demonstrates the potential for up to 95 percent emissions reduction compared to the BF-BOF route.[77] A major advantage of FINEX is its ability to use low-grade iron ore, making it more cost-competitive than conventional DRI systems and highly relevant for resource geographies like India and Japan, which rely heavily on lower-grade ore and seek to reduce import dependence.[78]

Building on this, POSCO’s HyREX technology integrates hydrogen-based DRI production using fluidised-bed reactors with an electric smelting furnace to produce liquid hot metal. This offers a viable pathway to replace carbon-intensive blast furnaces while advancing near-zero emission steelmaking.[79]

South Korea’s approach is highly integrated, export-oriented, and driven by chaebol-scale capital mobilisation, positioning it among the fastest-moving hydrogen-steel players globally.

Emerging Architecture for Green Steel Collaboration in the Region

Regional cooperation on green steel has expanded significantly as Indo-Pacific economies seek to align decarbonisation priorities with industrial competitiveness and supply-chain resilience. Green steelmaking now features prominently in discussions on critical materials, clean-technology deployment, standards harmonisation, and secure procurement; a shift accelerated by CBAM, global net-zero pledges, and rising demand for low-emissions steel from automotive and construction sectors.

Although no formal trilateral India–Japan–South Korea steel platform exists, the three countries increasingly intersect across bilateral and regional dialogues, including India–Japan industrial partnerships, Korea–Japan industry platforms, and broader Indo-Pacific economic and energy cooperation forums, where steel decarbonisation is emerging as a shared priority.

These discussions have led to joint benchmarks for steelmaking R&D and supported smart manufacturing pilot investments in India, such as a Joint Venture (JV) between India’s JSW steel and Japan’s JFE Steel to expand the production capacity of cold-rolled grain-oriented electrical steel across two Indian plants.[80] Furthermore, South Korea’s POSCO Group and India’s JSW Steel have signed a non-binding Heads of Agreement to explore setting up a 6 MTPA integrated steel plant in India.[81] Additionally, POSCO has partnered with Japan’s JERA to develop a low-carbon fuel value chain, an effort that could support future steel decarbonisation pathways by enabling access to cleaner energy inputs.[82]

At the 3rd India–Japan Steel Dialogue, both sides reaffirmed their commitment to deepening cooperation across areas of mutual interest, including advanced steel technologies, supply-chain resilience, and investment facilitation.[83] The Japanese delegation explicitly assured continued support for new-technology deployment and joint investments in India’s steel sector, reinforcing Japan’s long-term role in India’s transition to low-emissions steelmaking.

This cooperation is also unfolding amid shifting trade dynamics. South Korea became India’s largest steel supplier in FY 2024–25, particularly for high-grade products, surpassing China as the leading supplier of finished steel to India between April 2024 and January 2025.[84] This shift elevates the importance of coordinated standards and reliable low-emissions supply networks across the three economies.

Efforts toward harmonising green-steel definitions and certification systems have also begun through informal coordination among standards bodies and industry associations in the region. The World Steel Association’s (WSA) sustainability indicators and International Organisation for Standardization’s (ISO) ongoing work on low-carbon steel guidelines offer a common foundation. While full trilateral mutual-recognition frameworks are not yet formalised, early coordination is visible in public-infrastructure procurement discussions and in bilateral dialogues involving India–Japan and Korea–Japan steel associations.

Cross-border technology and standards advancement is also being catalysed through pilot initiatives. The Japan Iron and Steel Federation’s Product Category Rules (PCRs), approved in 2019 under the EcoLeaf environmental-label programme run by the Japan Environmental Management Association for Industry (JEMAI), provide standardised lifecycle-impact rules for steel products and secondary steel products used in both construction and non-construction applications. This establishes a starting point for comparable emissions accounting across regional markets. [85]

Similarly, South Korea has also formalised its approach. Since 2021, the Korean Green Taxonomy has defined environmental criteria for 69 economic activities, including steelmaking, enabling compliant companies to access preferential financing.[86] Together, these initiatives establish precise emission thresholds and third-party verification protocols to encourage mutual recognition and market access for low-carbon steel.

Beyond the three major economies, wider regional mechanisms are beginning to incorporate green-steel supply-chain integration. The Association of Southeast Asian Nations (ASEAN) and Australia have launched joint industrial eco-parks and are using the Regional Comprehensive Economic Partnership (RCEP) to facilitate clean-technology flows and regional supply-chain integration. Similarly, ASEAN–Japan and ASEAN–Korea energy cooperation frameworks now also include industrial-decarbonisation workstreams centred on hydrogen, CCUS, and industrial clusters.

Japan’s role within this emerging architecture is reinforced by its push to build a regional hydrogen-supply backbone. It is expanding renewable-powered hydrogen-production hubs, advancing liquefied-hydrogen import projects with Australia,[87] and pursuing public–private partnerships that establish early R&D and trade corridors with Indo-Pacific partners, including India.[88] While plans for a US$20 billion green-hydrogen facility are subject to political uncertainty under the new administration, they underscore Japan’s ambition to anchor the region’s future hydrogen economy.[89]

Further bilateral efforts are shaping this space as well. India’s and Japan’s ministerial meeting in 2023 highlighted a country-specific cooperation model that aligns economic growth with industrial decarbonisation. Meanwhile, Japan and South Korea have expressed interest in India’s National Green Hydrogen Mission, positioning hydrogen supply, ammonia co-firing, and electrolyser manufacturing as key areas of future convergence.

Broader cooperation is supported by emerging Asia-wide industrial consortia, including collaborations among POSCO, Nippon Steel, and Indian steelmakers on carbon-reduction technologies. Multilateral institutions including Asian Development Bank (ADB), Japan International Cooperation Agency (JICA), the World Bank, and the Green Climate Fund, now support capacity building, blended-finance platforms that combine public and concessional capital with private investment to de-risk projects, and demonstration pilots for industrial decarbonisation across the region.

Together, these initiatives indicate the emergence of a multi-layered regional architecture for green-steel cooperation linking technology development, standards alignment, and investment mobilisation across the Indo-Pacific.

Policy Recommendations: Accelerating a Trilateral Green Steel Transition

Building on the technology pathways and cooperation landscape outlined in this report, the following recommendations identify priority interventions that can unlock investment, harmonise standards, and accelerate low-carbon steelmaking amongst India, Japan, and Korea as well as across the wider Indo-Pacific region.

Short Term: Governments can establish regular trilateral convenings to exchange expertise on hydrogen-DRI deployment, CCUS retrofits, and supply-chain resilience. Standards bodies could begin technical working groups to move toward aligned emissions thresholds and data-reporting frameworks, building on existing WSA and ISO guidance. Industry and research institutions should collaborate through joint R&D platforms to address bottlenecks in hydrogen storage, ore preparation, scrap sorting, and EAF efficiency.

Medium Term: Countries could jointly support pilot-scale green hydrogen-based DRI plants, cross-border demonstration projects, and testbeds for harmonised green-steel certification. Governments can promote and incentivise green-steel usage in public procurement, to enable early demand, encouraging sectors such as automotives, construction, and renewable-energy manufacturing to adopt procurement targets for near-zero-emission steel.

Alongside demand creation, coordinated industrial partnerships can reduce technology and financing risks. Joint ventures anchored by leading steelmakers such as Nippon Steel, Kobe Steel, Tata Steel, and POSCO can provide technology guarantees and offtake commitments that lower financial risk premiums.

Proprietary low-emissions technologies, including South Korea’s FINEX steelmaking process and HyREX hydrogen reduction process, could be shared through structured technology partnerships to accelerate regional learning curves. In parallel, India, Japan, and South Korea can co-develop hydrogen and ammonia corridors, shared standards for green-steel exports, and financing vehicles for large-scale commercial hydrogen-DRI/EAF deployment. The trilateral target for green steel certification should be to establish a mutual recognition framework that is more aligned with global near-zero definitions.

Long Term: Following the development of hydrogen and ammonia corridors, all governments should ensure incremental progress towards a long-term climate finance target, aiming to leverage ADB, JICA, and K-EXIM coordination. Regional partners should transition from pilots to integrated industrial clusters, including renewable-powered electrolysis, scrap-processing hubs, and dedicated transport and storage for hydrogen and CO₂. Over time, aligned certification systems should evolve into mutual-recognition frameworks, facilitating seamless trade in low-carbon steel.

Cross-Cutting System-Level Recommendations

- Infrastructure for low-emission steelmaking: A foundational step is investment in purpose-built infrastructure, including renewable-powered electrolysis; hydrogen transport and storage systems; expanded grid capacity; and large-scale scrap-processing hubs. Existing supply chains designed around coal and fossil fuels require modernisation to support electrified steelmaking, circular-economy logistics, and low-carbon transport systems.

- Accelerate green hydrogen usage in DRI-EAF steelmaking: Using green hydrogen in DRI-EAF configurations yields greater emissions reductions than hydrogen injection in blast furnaces or CCUS retrofits. Accordingly, industrial policy should favour the transition to H-DRI/EAF routes through R&D support, tax incentives for early adopters, and public procurement mandates that specify low-carbon steel usage in infrastructure contracts. This combination of supply-side incentives and demand-side pull will lower investor risk and accelerate green steel adoption.

- Reduce green hydrogen costs and competitiveness barriers: With green hydrogen costs in India currently estimated at US$3.5–5/kg,[90] recent tenders signal early cost declines, including a record-low bid of INR 279 (US$3.08)/kg to supply 10,000 tonnes annually to Numaligarh Refinery Limited, majority-owned by Oil India Limited.[91] However, globally, green steel still costs around 40 percent more than unabated production today, highlighting the importance of scale, infrastructure, and policy support.[92] To accelerate cost parity and industrial transition, the three countries must prioritise domestic electrolyser manufacturing, renewable expansion, long-term power-purchase mechanisms, and regional hydrogen corridors. These efforts will bring hydrogen closer to parity by 2030, in line with India’s 5 MTPA green-hydrogen target.[93]

- Establish a trilateral green steel investment framework and scale blended finance: Trilaterally, governments should aim to create standardised financial modelling and develop a decision-support tool to compare the economic viability of different low-emissions steelmaking pathways under country-specific conditions. This will reduce information asymmetry between stakeholders, allowing for tracking of technology developments and adjustment of policies over time. With steel recognised by the G20 Sustainable Finance Working Group as one of the world’s top transition-finance priorities, the countries should use this momentum to scale blended-finance vehicles. This can include tapping into concessional credit lines and multilateral transition funds (ADB, JICA, GCF) to unlock capital for low-emission steelmaking infrastructure, and workforce transition programmes aimed at reskilling and capacity-building for effective deployment. Coordinated financing strategies can turn scattered pilot investments into a bankable regional decarbonisation pipeline.

- Harmonising green-steel certification: Regional alignment on emissions thresholds, measurement, reporting and verification (MRV), and certification protocols will reduce transaction costs and enable smoother trade.[94] Reducing the minimum emission intensity threshold of what qualifies as green steel, according to India’s newly released taxonomy, will be key in meeting the ambitions of decarbonising the sector. Presently, three-star green-rated steel must have an emission intensity between 2.0 and 2.2 t-CO2e /tfs, which remains above the current global average of steelmaking of 1.9 t-CO2e /tfs. Further, a trilateral alignment among India, Japan, and South Korea can serve as the foundation for a broader Indo-Pacific mutual-recognition system, strengthening market access and regional supply-chain resilience.

Collectively, these recommendations can enable India, Japan, and South Korea to move from fragmented national initiatives to a coherent, region-wide strategy grounded in shared technology priorities, aligned standards, connected supply chains, and coordinated financing. By acting together, the three economies can shape the Indo-Pacific’s emerging green-steel architecture and position the region as a global leader in industrial decarbonisation.

Conclusion: A Trilateral Imperative for Green Steel Leadership

The transition to green steel in the Indo-Pacific is no longer a distant objective but a strategic necessity. India, Japan, and South Korea sit at the centre of this shift, each contributing distinct strengths to a shared industrial transformation: India’s expanding production base, Japan’s technological leadership, and South Korea’s rapid hydrogen-scaling capabilities. As global markets tighten carbon-based trade measures and demand for low-emissions steel accelerates, coordinated action across these three economies will be crucial to safeguarding competitiveness, maintaining market access, and securing resilient regional supply chains.

The pressures are mounting, from CBAM compliance to volatile commodity markets and intensifying competition in low-carbon manufacturing. Yet these challenges also present a rare window for deeper collaboration across technology pathways, standards harmonisation, infrastructure development, and green-finance mobilisation. A trilateral approach offers the necessary scale and complementary advantages to move beyond fragmented pilots toward an integrated Indo-Pacific ecosystem for near-zero-emission steel.

By aligning policy frameworks and leveraging public-private investment, India, Japan, and South Korea can jointly unlock the deployment of hydrogen-DRI, strengthen and mutually recognise green-steel certification, expand scrap-processing and hydrogen infrastructure, and deploy CCUS where strategically viable. In doing so, the three economies can shape the rules, standards, and supply chains that will govern the next era of industrial competitiveness.

Ultimately, whether the Indo-Pacific emerges as a global leader in industrial decarbonisation or cedes that ground to more coordinated regions will depend on the choices made today. A decisive trilateral partnership will not only accelerate the green-steel transition but also signal the region’s intent to lead, rather than follow, the industrial transformations defining the decades ahead.

Parul Bakshi is Fellow, Energy and Climate, ORF Middle East.

Krishna Vohra is Junior Fellow, Centre for Economy and Growth, ORF.

Acknowledgement

The authors acknowledge the use of Claude Sonnet 4.6 to conduct a preliminary literature survey and for language refinements prior to submission.

All views expressed in this publication are solely those of the authors, and do not represent the Observer Research Foundation, either in its entirety or its officials and personnel.

Endnotes

[a] Green steel is not a new alloy or product, but steel produced through cleaner processes.

[1] World Economic Forum, “Steel Industry Net-Zero Tracker,” in Net-Zero Industry Tracker: 2024 Edition, Geneva, World Economic Forum, December 2024, https://reports.weforum.org/docs/WEF_Net_Zero_Industry_Tracker_2024_Steel.pdf

[2] “Steel Industry Net-Zero Tracker”

[3] Astrid Grigsby-Schulte et al., Pedal to the Metal: Evaluating Progress Toward 2030 Iron and Steel Decarbonization Goals, San Francisco Global Energy Monitor, May 2025, https://globalenergymonitor.org/wp-content/uploads/2025/05/GEM-global-steel-report-May-2025.pdf

[4] Niklas Brundin et al., Paving the Way to Net Zero: The Future of Green Steel, Arthur D. Little, 2025, https://www.adlittle.com/sites/default/files/viewpoints/ADL%20Paving%20the%20way%20to%20net-zero%202025.pdf

[5] Stefan Ellerbeck, “What is Green Steel and How Can It Help Us Reach Net Zero?,” World Economic Forum, July 2022, https://www.weforum.org/stories/2022/07/green-steel-emissions-net-zero/

[6] “DGTR Launches Probe into Cheap Stainless Steel Imports from China, Indonesia, Vietnam,” Economic Times, October 3, 2025, https://economictimes.indiatimes.com/industry/indl-goods/svs/steel/dgtr-launches-probe-into-cheap-stainless-steel-imports-from-china-indonesia-vietnam/articleshow/124297018.cms

[7] OECD, OECD Steel Outlook 2025, Paris, OECD, May 2025,

[8] Joseph Olbrycht-Palmer, “Australia Slaps 10 Per Cent Levy on Chinese Steel Ceiling Frames,” news.com.au, February 8, 2026, https://www.news.com.au/national/politics/australia-slap-10-per-cent-levy-on-chinese-steel-ceiling-frames/news-story/c81d05d9b3d7fc68f1944e6dc360f6d7

[9] “Taiwan Customs Confirms Anti-Dumping Duties on Chinese Beer, Steel,” Taipei Times, September 25, 2025, https://www.taipeitimes.com/News/biz/archives/2025/09/25/2003844369

[10] Anirban Sanyal and Sanjay Singh, “Steel Under Siege: Understanding the Impact of Dumping on India,” RBI Bulletin, October 2025, https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/05ARTICLE20102025C70817FD01F6404B8CC1279F0948B79E.PDF

[11] Directorate General of Foreign Trade, Government of India, https://content.trade.gov.in/TCP-CMS/12766729435441048/3080000217/3.pdf

[12] “South Korea Surpasses China to Become India’s Top Steel Supplier Amid Trade Protectionism,” S&P Global Commodity Insights, February 27, 2025, https://www.spglobal.com/commodity-insights/en/news-research/latest-news/metals/022725-south-korea-surpasses-china-to-become-indias-top-steel-supplier-amid-trade-protectionism

[13] World Steel Association, World Steel in Figures 2025, Brussels, World Steel Association, 2025, https://worldsteel.org/data/world-steel-in-figures/world-steel-in-figures-2025/

[14] Ali Hasanbeigi, Steel Climate Impact 2025: An International Benchmarking of Energy and GHG Intensities, Global Efficiency Intelligence, 2025,

https://static1.squarespace.com/static/5877e86f9de4bb8bce72105c/t/68f30ceebdbccf7dc6b7c877/1760759022538/Steel+benchmarking+-10.10.2025-E.1.pdf

[15] World Steel Association, “Responsible Value Chain,” World Steel Association, https://worldsteel.org/wider-sustainability/responsible-value-chain/

[16] Joint Plant Committee, Indian Steel Industry: April 2025 – A Trend Report, (New Delhi: Ministry of Steel, Government of India, April 2025), https://jpcindiansteel.nic.in/writereaddata/files/TrendReportApril%202025.pdf

[17] Pedal to the Metal, pp. 11.

[18] “World Steel in Figures 2025”

[19] “Steel Climate Impact 2025”

[20] “Steel Climate Impact 2025”

[21] Sabarish Elango et al., Evaluating Net-zero for the Indian Steel Industry: Marginal Abatement Cost Curves of Carbon Mitigation Technologies, Council on Energy, Environment and Water, October 2023, https://www.ceew.in/sites/default/files/How-Can-India-Decarbonise-For-Net-Zero-Sustainable-Steel-Production-Industry.pdf

[22] “The Share of EAF in Global Steel Production in 2024 Increased to 29.1%,” GMK Center, June 12, 2025, https://gmk.center/en/news/the-share-of-eaf-in-global-steel-production-in-2024-increased-to-29-1/

[23] Kapil Bansal et al., Green Steel Production Pathways for India, WWF India and EY Parthenon, October 2024, https://www.ey.com/content/dam/ey-unified-site/ey-com/en-in/insights/mining-metals/ey-green-steel-production-pathways-for-india.pdf

[24] Lauren Huleatt, Kenta Kubokawa, and Akira Kanno, Japanese Electric Arc Furnace Steel: A Market Ready for Low-Carbon Growth, Hong Kong, Transition Asia, March 2025, https://transitionasia.org/wp-content/uploads/2025/03/TA_JP_EAF_032025.pdf

[25] “China Baowu Steel’s Net-Zero Target is Just the Start,” BloombergNEF, February 18, 2021, https://www.bloomberg.com/professional/insights/commodities/china-baowu-steels-net-zero-target-is-just-the-start/

[26] “Steel Climate Impact 2025”

[27] Global Energy Monitor, “Electric Arc Furnaces and the Decarbonization of Steel,” Global Energy Monitor,

,”, https://globalenergymonitor.org/research/electric-arc-furnaces-and-decarbonization-steel

[28] OECD, Hydrogen in Steel: Addressing Emissions and Dealing with Overcapacity, Paris, OECD, March 2025, https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/03/hydrogen-in-steel_f4d15f8d/7e2edc69-en.pdf

[29] Sara Budinis et al., Iron and Steel Technology Roadmap: Towards More Sustainable Steelmaking, Paris, International Energy Agency, October 2020, https://www.iea.org/reports/iron-and-steel-technology-roadmap

[30] HYBRIT Development, “Fossil-Free Steel Production Ready for Industrialisation,” HYBRIT Development, November 14, 2024,

https://www.hybritdevelopment.se/en/fossil-free-steel-production-ready-for-industrialisation/

[31] Douglas Main, “The World’s First Industrial-Scale Plant for Green Steel Promises a New Age of Manufacturing,” MIT Technology Review, December 27, 2024,

[32] World Steel Association, World Steel in Figures 2024, Brussels, World Steel Association, 2024, https://worldsteel.org/data/world-steel-in-figures/world-steel-in-figures-2024/

[33] Nippon Steel Corporation, Green Transformation (GX) Initiatives, Tokyo, Nippon Steel Corporation, March 13, 2025, https://www.nipponsteel.com/en/ir/library/pdf/20250313_100.pdf

[34] Paul Mitchell, “Five Actions to Improve the Sustainability of Steel,” EY Global, July 20, 2021, https://www.ey.com/en_gl/insights/energy-resources/five-actions-to-improve-the-sustainability-of-steel

[35] “Net-Zero Industry Tracker: 2024 Edition”

[36] BloombergNEF, Decarbonization of Japan’s Steel Industry: Economics and Path Forward, BloombergNEF, December 3, 2025, https://assets.bbhub.io/professional/sites/44/2025-12-3_Tokyo-Steel_BNEF_Final_Eng.pdf

[37] “OECD Steel Outlook 2025”

[38] “Decarbonization of Japan’s Steel Industry”

[39] Katinka Waagsaether, Aleksandra Waliszewska, and Johanna Lehne, Country Profile – Japan: 2023 Steel Policy Scorecard E3G, February 2024, https://www.e3g.org/wp-content/uploads/E3G-2023-Steel-Policy-Scorecard-Country-Profile-Japan.pdf

[40] Korea Iron & Steel Association (KOSA), “Steel Production Statistics,” Korea Iron & Steel Association, https://www.kosa.or.kr/sub/eng/statistics/production3.jsp

[41] Ministry of Steel, Government of India, Annual Report 2024–25, (New Delhi: Ministry of Steel, 2025), https://steel.gov.in/sites/default/files/2025-04/Steel_English_AR_2024%20%281%29.pdf

[42] Joojin Kim and Geunha Kim, The South Korean Steel Industry and Carbon Neutrality: Responses, Issues, and Policy Recommendations, Solutions for Our Climate, November 2021, https://content.forourclimate.org/files/research/U8eiFUe.pdf

[43] Akira Kanno, 2025 Integrated Report Updates: Nippon Steel, Transition Asia, October 2025, https://transitionasia.org/wp-content/uploads/2025/10/TA_Sus_Report_NS_2025_251003.pdf

[44] “Steel Climate Impact 2025”

[45] “Pedal to the Metal”

[46] IPE Global, “Budget 2026–27 Sets Aside Rs 20,000 Cr to Accelerate Carbon Capture,” IPE Global, February 2026, https://www.ipeglobal.com/in-budget-2026-27-environment-takes-a-backseat/

[47] Ministry of Steel, Government of India, https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=2083839

[48] Ministry of Steel, Government of India, Green Steel Taxonomy for India (New Delhi: Ministry of Steel, 2024, https://steel.gov.in/sites/default/files/2025-03/Taxonomy%20Brochure.pdf

[49] “AMNS India Has Received a Green Steel Certificate for Its Steel Products,” GMK Center, February 5, 2026,

https://gmk.center/en/news/amns-india-has-received-a-green-steel-certificate-for-its-steel-products/

[50] “Net-Zero Industry Tracker: 2024 Edition”

[51] Ministry of New and Renewable Energy, Government of India, https://mnre.gov.in/en/national-green-hydrogen-mission/

[52] Ministry of New and Renewable Energy, Government of India

[53] Tata Steel, “Tata Steel Initiates Trial for Record-High Hydrogen Gas Injection in Blast Furnace at its Jamshedpur Works,” press release, Tata Steel, April 2023, https://www.tatasteel.com/media/newsroom/press-releases/india/2023/tata-steel-initiates-trial-for-record-high-hydrogen-gas-injection-in-blast-furnace-at-its-jamshedpur-works/

[54] “JSW Energy Commissions India’s Largest Green Hydrogen Plant in Karnataka,” Economic Times, November 11, 2025, https://economictimes.indiatimes.com/industry/renewables/jsw-energy-commissions-indias-largest-green-hydrogen-plant-in-karnataka/articleshow/125242518.cms

[55] ArcelorMittal, “ArcelorMittal Nippon Steel India Targets a Reduction in Emissions Intensity by 20% by 2030,” ArcelorMittal, February 5, 2024, https://corporate.arcelormittal.com/media/news-articles/arcelormittal-nippon-steel-india-targets-a-reduction-in-emissions-intensity-by-20-by-2030

[56] Neha Verma et al., Greening the Steel Sector in India: Roadmap and Action Plan, (New Delhi: Ministry of Steel, Government of India, September 2024),

https://steel.gov.in/sites/default/files/2025-03/GSI%20Report.pdf

[57] “Tata Steel Aims to Achieve Circular Production in the Next 10–15 Years,” GMK Center, June 16, 2025, https://gmk.center/en/news/tata-steel-aims-to-achieve-circular-production-in-the-next-10-15-years/

[58] “Greening the Steel Sector in India”

[59] Will Hall, Sidharth Sinha, and Mayank Aggarwal, Green Steel by 2030: Building the Business Case for the First Green Steel Plant in India, New Delhi, The Energy and Resources Institute, January 22, 2026, https://teriin.org/policy-brief/green-steel-2030-building-business-case-first-green-steel-plant-india

[60] Ministry of New and Renewable Energy, Government of India, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2108170

[61] “Green Steel by 2030”

[62] “Green Steel by 2030”

[63] “Pedal to the Metal”

[64] Cabinet Secretariat, Government of Japan, “The Basic Policy for the Realization of GX,” 2023, https://www.cas.go.jp/jp/seisaku/gx_jikkou_kaigi/pdf/kihon_en.pdf.

[65] InfluenceMap, “Japan Steel Decarbonization Policies,” InfluenceMap, https://japan.influencemap.org/policy/Japan-Steel-Policy-5558

[66] “Japan Mulls Barring International VCM Credits Before GX-ETS Launch; Move to be Bullish for Domestic Credits,” S&P Global Commodity Insights, July 7, 2025, https://www.spglobal.com/commodity-insights/en/news-research/latest-news/energy-transition/070725-japan-mulls-barring-international-vcm-credits-before-gx-ets-launch-move-to-be-bullish-for-domestic-credits

[67] Ali Hasanbeigi and Navdeep Bhadbhade, Green Public Procurement of Steel in India, Japan, and South Korea, Florida, Global Efficiency Intelligence, April 2023, https://static1.squarespace.com/static/5877e86f9de4bb8bce72105c/t/6435249e1d7f8d2d3bc48732/1681204404601/Steel+GPP+report-+24Mar2023.pdf

[68] “Green Transformation (GX) Initiatives”

[69] Green Innovation Fund Project Hydrogen Steelmaking Consortium (GREINS), “Organisation,” https://www.greins.jp/en/research/

[70] “Decarbonization of Japan’s Steel Industry”

[71] “Decarbonization of Japan’s Steel Industry”

[72] Climate Transparency, Climate Transparency Report 2022: South Korea, Climate Transparency, October 2022, https://www.climate-transparency.org/wp-content/uploads/2022/10/CT2022-South-Korea-Web.pdf

[73] Korea Iron & Steel Association (KOSA), “Korean Steel Industry’s Decarbonization Plan” (paper presented at the OECD Knowledge Sharing Workshop on Carbon Capture and Storage and Hydrogen Use for Iron and Steel Production, Paris, June 11, 2025), https://www.oecd.org/content/dam/oecd/en/events/2025/06/knowledge-sharing-workshop-on-iron-and-steel/session-1-presentation-kosa.pdf/_jcr_content/renditions/original./session-1-presentation-kosa.pdf

[74] KOSA, “Korean Steel Industry’s Decarbonization Plan”

[75] Jeong Ji-seong and Han Yubin, “Korean Steel Industry Hit by Carbon Permit Costs, High Tariffs,” Pulse, October 17, 2025, https://pulse.mk.co.kr/news/english/11444056

[76] “The South Korean Steel Industry and Carbon Neutrality”

[77] “South Korea to Develop Hydrogen-Based Steelmaking Technology by 2030,” The Korea Times, June 26, 2025, https://www.koreatimes.co.kr/business/tech-science/20250626/south-korea-to-develop-hydrogen-based-steelmaking-technology-by-2030

[78] “Pedal to the Metal”

[79] “POSCO Advances Hydrogen-Based Steel Production with HyREX Demonstration Plant,” Mesteel Online News, n.d., https://news.mesteel.com/posco-advances-hydrogen-based-steel-production-with-hyrex-demonstration-plant/

[80] “India’s JSW Steel, Japan’s JFE to Invest $669 Million to Boost Electrical Steel Output,” Reuters, August 4, 2025, https://www.reuters.com/world/india/indias-jsw-steel-japans-jfe-invest-669-million-boost-electrical-steel-output-2025-08-04/

[81] POSCO Group Newsroom, “POSCO Group and JSW Steel Sign Heads of Agreement to Explore 6 MTPA Integrated Steel Plant in India,” POSCO, August 18, 2025, https://newsroom.posco.com/en/posco-group-and-jsw-steel-sign-heads-of-agreement-to-explore-6-mtpa-integrated-steel-plant-in-india/

[82] JERA, “JERA Has Concluded a Joint Collaboration Agreement with POSCO International to Realize Low Carbon Fuel Value Chains” JERA, September 26, 2024, https://www.jera.co.jp/en/news/information/20240926_2011

[83] Ministry of Steel, Government of India, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2100091

[84] “South Korea the Top Steel Supplier to India in FY24–25,” Argus Media, April/May 2025, https://www.argusmedia.com/en/news-and-insights/latest-market-news/2680944-south-korea-the-top-steel-supplier-to-india-in-fy24-25

[85] “Green Public Procurement of Steel in India, Japan, and South Korea”

[86] Ihor Vorontsov, “Prospects for South Korean Green Steel,” GMK Center, September 3, 2025, https://gmk.center/en/posts/prospects-for-south-korean-green-steel/

[87] Antara Mascarenhas and Parul Bakshi, “Australia and Japan’s Hydrogen Partnership: Navigating Ambitions and Realities,” The Diplomat, April 24, 2025, https://thediplomat.com/2025/04/australia-and-japans-hydrogen-partnership-navigating-ambitions-and-realities/

[88] “Important Updates in India’s Green Hydrogen Landscape,” GH2 India, July 18, 2025, https://gh2.org.in/important-updates-in-indias-green-hydrogen-landscape/

[89] “Japan May Open $20 Billion Hydrogen Plan Applications in Summer,” Bloomberg, January 30, 2024, https://www.bloomberg.com/news/articles/2024-01-30/japan-may-open-20-billion-hydrogen-plan-applications-in-summer

[90] GreenH, “Green Hydrogen to Become Cost-Competitive by 2030,” GreenH, n.d., https://www.greenh.in/green-hydrogen-cost-by-2030-and-industrial-adoption/

[91] “India Records Lowest-Ever Price for Green Hydrogen in Tender,” Economic Times, February 15, 2026, https://economictimes.indiatimes.com/industry/renewables/india-records-lowest-ever-price-for-green-hydrogen-in-tender/articleshow/128417452.cms

[92] Julia Attwood, “Green Steel Demand Is Rising Faster Than Production Can Ramp Up,” BloombergNEF, June 26, 2023, https://about.bnef.com/insights/finance/green-steel-demand-is-rising-faster-than-production-can-ramp-up/

[93] Ministry of New and Renewable Energy, Government of India, https://mnre.gov.in/en/national-green-hydrogen-mission/

[94] “Green Public Procurement of Steel in India, Japan, and South Korea”