Expert Speak | 11 May, 2026

Impacts of an Impending “Super” El-Niño on Global Supply Chains

Spotlight:

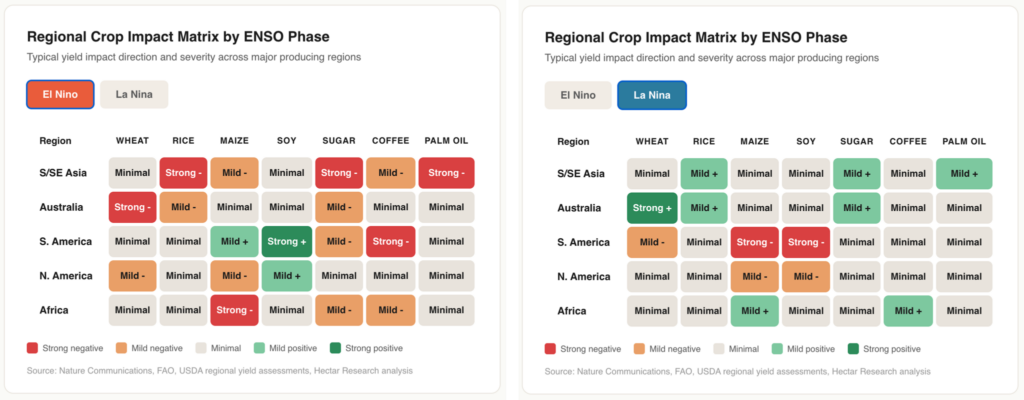

- The projected El Niño is likely to yield asymmetric impacts; with drought-like conditions reducing maize, rice, and wheat production in Asia and Australia and wet conditions boosting global soybean production in the Americas.

- El-Niño conditions hinder the clean energy transition by exacerbating heatwaves, draining hydrodams, and restricting access to mines due to flash floods.

- Parametric insurance, adaptive measures, and infrastructure resilience will be crucial to buffer against shocks from conflict and climate interlinkages.

The El-Niño Southern Oscillation is a climate phenomenon oscillating between two phases: El Niño and La Niña, with each cycle spanning two to seven years. While La Niña induces cooling tendencies, El Niño increases global average surface temperatures. Historically, El Niño events have increased rainfall and flood risk in dry areas such as the Americas, while instigating drought in wet areas like South and Southeast Asia.

As the world forges through geopolitical upheaval, a prospective “Super” El-Niño, albeit a non-standardised classification, threatens to further destabilise global supply chains. The World Meteorological Organisation (WMO) predicts an upward shift in sea-surface temperatures in the Equatorial Pacific as early as May to July 2026, with an estimated 60 percent risk of El Niño development by summer. This trend is particularly alarming, as the looming El Niño will likely coincide with conflict-induced trade restrictions in the Middle East, which have already stranded maritime shipments, driven transpacific container rates 40 percent above pre-crisis levels, and restricted critical urea and phosphorus fertiliser exports.

The stakes are high, as the last dubbed “Super” El Niño invoked billions of dollars of losses, including US$327 million in the agricultural sector alone. Despite these risks, current studies highlight a deficit in forecasting effectiveness and strategic response capacity, often underestimating risk. This article evaluates projected asymmetric impacts of a Super El Niño across regional agricultural commodities, energy, and infrastructure, underscoring the urgent need for localised climate adaptation investments and measures.

Impacts on Agricultural Commodities

Drought Conditions in South Asia, Southeast Asia, and Australia

Akin to previous patterns, El Niño is likely to induce drought-like conditions in Southeast Asia and Australia and a weaker monsoon season in South Asia, negatively impacting rice, grain, sugar, and palm oil production. For South Asia, the monsoon season is referred to as the region’s “real finance minister,” as agriculture largely underpins regional GDP. India, for instance, estimates below-average monsoon rains for the first time in three years. Prolonged trade blockages of nitrogenous-based fertilisers through the Strait of Hormuz and dwindling options for viable fertiliser alternatives may result in potentially weaker yields for rice, cotton, and soybeans. Likewise, weakening rainfall across Thailand and Vietnam, the world’s second and third largest global rice exporters, raises food security concerns for high-importing countries such as the Philippines where rice composes the bulk of caloric intake. Potential food insecurity is further exacerbated by intermittent rice and fertiliser export restrictions, dependencies on energy-intensive irrigation practices, and rising costs of cooking gas. Moreover, El Niño conditions are expected to exacerbate below-average rainfall in Australia, reducing wheat production and exports to Asia, placing pressure on domestic stockpile buffers.

Prolonged trade blockages of nitrogenous-based fertilisers through the Strait of Hormuz and dwindling options for viable fertiliser alternatives may result in potentially weaker yields for rice, cotton, and soybeans.

Diverging Impacts Across the Americas

El Niño induces diverging impacts on North and South America, positively impacting soy production and negatively impacting coffee production. For instance, during El Niño events, average soybean yields improve by 2.1 to 5.4 percent, due to more favourable growing conditions in the United States (US), Argentina, and Brazil. Brazil’s soybean harvests are progressing well due to rain from La Niña conditions, but El Niño could negatively affect 2027 crop production alongside fertiliser restrictions due to aforementioned conflict-induced trade blockages. Despite current strong crop output, Brazil has every incentive to leverage soybeans domestically for biofuels to shield the country from the US-Israel-Iran war fuel import disruptions. The country already seeks to increase its biofuel portion of diesel to 20 percent and high bunker fuel prices inhibit exports from reaching markets. In coffee-growing countries across the equator, El Niño also invokes dry conditions and heat stress, negatively affecting coffee yields and smallholder producer livelihoods. However, given previously record-high Brazilian coffee crop harvests, future coffee production is not expected to be seriously affected. The diverging contrast across geographies necessitates tailored response strategies among policymakers and international agencies.

Mixed Impacts Across the Middle East, South and East Africa

For the Middle East, a lingering El Niño threatens domestic water supply, with the potential for drought-related disputes to emerge in Iraq, Syria, and Lebanon. Compounded by ongoing conflicts, water scarcity, high fertiliser and fuel costs, El Niño conditions may threaten food insecurity and drain declining fiscal buffers. However, an El Niño also increases the risk for extreme heat, heavy precipitation and flash floods, testing the adaptive capacity of urban infrastructure. In Southern Africa, drought conditions may reduce regional maize production, while Kenyan maize crop production in the East may benefit from additional rainfall.

Source: Hectar Global

Impacts on the Energy Transition

Beyond agricultural commodities, severe weather disruptions also compromise energy distribution, creating a feedback loop that temporarily hinders clean energy transition efforts. A Super El Niño may intensify heatwaves, simultaneously straining water supplies and power grid connectivity, prompting increased fossil fuel dependencies. In India, a rise in electricity demand from El Niño conditions is expected to raise coal-fired power generation by 10 percent year over year, and the country is looking to leverage hydropower to fill the gaps. However, hydropower-dependent countries may be forced to reduce output or shut down due to droughts or torrential flooding. In Zambia and Zimbabwe, for instance, El Niño drought conditions previously reduced hydropower generation at Kariba Dam.

A Super El Niño may intensify heatwaves, simultaneously straining water supplies and power grid connectivity, prompting increased fossil fuel dependencies.

Beyond immediate power shortages, climate-driven energy disruptions intersect with Strait of Hormuz blockages, sharp oil price hikes, and infrastructure vulnerabilities, stalling critical minerals output across Global South countries. In Indonesia, where hydropower underpins mining operations, any shortfall in rain risks curtailing the country’s nickel operations, affecting global steel production. These operations are further compounded by a disruption in sulphur feedstock from the Middle East which is crucial for purifying Indonesia’s nickel supply. On the opposing end, El Niño increases heavy rain in Chile, inhibiting access to Chile’s mountainous mining regions which house large copper deposits.

Impacts on Maritime Trade Corridors

Drier El Niño conditions can also restrict maritime traffic. A decline in water levels from the previous El Niño resulted in reduced weight limits and increased vessel surcharges for shipments across the Panama Canal. Shipments were previously able to be rerouted through the Suez Canal, Strait of Magellan, and the Cape of Good Hope. With ongoing trade blockages at the Strait of Hormuz, added climate vulnerabilities may further complicate just-in-time supply chain operations. Likewise, the Suez Canal is already subject to coastal inundation. El-Niño associated rainfall shifts from the land to ocean could further exacerbate rising sea levels, compromising critical maritime infrastructure. Previous simulations highlight how small-island developing states (SIDS) would be the most negatively affected by increased shipping rates from geopolitical and climate disruptions at key maritime chokepoints, due to their heavy economic dependence on maritime shipping and processed food imports. SIDS are projected to experience a 0.9 percent consumer price impact, and a 0.11 percent reduction in real GDP, a figure doubles the global average. SIDS also have differing adaptive capacities to respond to shocks due to their economic structure, debt levels, and institutional capacity, with concentrated economies having lower adaptive capacity compared to diversified economies.

Looming El-Niño Underscores Importance of Climate Resilience Measures

While increasing food and energy stocks and diversifying trade corridors are crucial to safeguarding economic growth amidst El Niño conditions, accelerating investments in climate insurance mechanisms and other resilience measures is equally crucial to protect vulnerable households, small-sector players, and infrastructure across agriculture, energy, and water management sectors.

Climate-related insurance schemes are already expected to rise by 50 percent by 2030, thus prompting the need to recalibrate insurance to incentivise resilience approaches.

First, parametric insurance schemes can help mitigate financial impacts of extreme El Niño conditions on vulnerable populations. Climate-related insurance schemes are already expected to rise by 50 percent by 2030, thus prompting the need to recalibrate insurance to incentivise resilience approaches. Peru piloted an El Niño Index Insurance which determines pay outs through a pre-defined index instead of physical flooding or drought damages. By releasing payouts prior to the heaviest flooding and rainfall, communities or companies are offered funding earlier on to reinforce infrastructure, shift planting schedules, or harvests, allowing them to mitigate potential losses as opposed to reacting to damage. Likewise, Colombia also released a parametric insurance solution which reacts to predefined weather change thresholds to help smallholder coffee households recover from climate shocks. Several limitations of parametric insurance include a lack of compensation to losses just above or below the predetermined threshold and the increasing frequency of insurance payouts associated with intensifying climate risks.

Second, embedding resilience considerations in crop and infrastructure planning is crucial to mitigate risks and lower costs. Often, policies for slow onset climate events such as El Niño are incomprehensive and fragmented. For the agricultural sector, impacts on crop output often depend on timing, intensity, duration, and intersection with growing and harvest seasons. Thus, supporting small-scale farmers to pre-emptively develop alternative crop value chains and monitor changes in water salinity will help them prepare for extreme drought or flooding events. FAO analyses suggest that every US$1 invested in anticipatory action adds US$7 in value of avoided losses and added benefits for families. For urban infrastructure, combining enhanced localised weather monitoring for extreme heat or flash flooding with grey and green infrastructure solutions, stormwater management, and land-use regulation will help reduce cascading repercussions. For the maritime sector, establishing backup trade routes during drier months can help prevent stranded goods, while strengthening investments in maritime infrastructure resilience significantly reduces high transport costs. A UNCTAD analysis found that an investment-to-export ratio in maritime transport infrastructure that improves from the bottom 20th percentile to the 20th-40th percentile group would decrease maritime costs by 4.7 percent.

Embedding resilience considerations in crop and infrastructure planning is crucial to mitigate risks and lower costs.

The forthcoming “Super El-Niño” threatens to exacerbate compounding crises wreaking havoc on global food and energy supply chains. The increasing need for climate-resilient infrastructure to buffer against the incoming volatility of conflict and climate interlinkages is already driving 2026 green bond deployment and cargo war risk insurance. However, ensuring that finance translates to resilient infrastructure development will be crucial to reducing food insecurity, clean energy disruptions, and disproportionate cost burdens.

Leigh Mante is Junior Fellow, Climate and Energy, ORF Middle East.