Expert Speak | 24 April, 2026

Resilient Food Systems Beyond Inorganic Fertiliser Reliance

Spotlight:

- Global inorganic fertiliser supply relies on a narrow group of exporters, rendering it vulnerable to price shocks, trade blockages, and infrastructural disruptions.

- The high concentration of raw material inputs and protectionist domestic policies further compromise global fertiliser supply chain security.

- Bolstering regional fertiliser reserves, open trade and diversification, demand-side monitoring, and gradual transitions towards alternative and organic fertilisers can decouple food security from market volatility.

Fertiliser’s Pivotal Role in Modern-Day Agriculture

Modern agriculture systems depend on inorganic fertilisers to feed the global population of 8 billion people. In the 19th century, rapid population growth increased demand for large-scale food production and agricultural efficiency improvements. To increase land productivity and crop yields, fertilisers emerged as a key solution. However, heightened dependencies on inorganic fertilisers have introduced significant environmental and supply chain risks. Fertilisers contribute to nutrient runoff and carbon emissions. For instance, the use of natural gas in the Haber-Bosch process to produce ammonia, accounts for approximately 84 percent of fertiliser-related emissions, while fertiliser application generates carbon dioxide and nitrous oxide. In the 21st century, a series of compounding conflicts has further exposed new vulnerabilities in global fertiliser trade.

The global food system relies on a limited number of key fertiliser suppliers, many of whom are located near conflict‑prone regions. The Russia-Ukraine war and US-Israel war on Iran have exposed the fragility of dependencies on singular trade routes and unilateral supply chains, prompting a reconstitution of fertiliser resilience. To safeguard global food systems while progressing towards net-zero carbon goals, this article argues for a supply-demand approach involving the immediate-term development of global fertiliser storage reserves, incremental investments in fertiliser alternatives, and enhanced demand-side fertiliser regulation, monitoring, and transparency.

Overview and Constraints of The Global Fertiliser Market

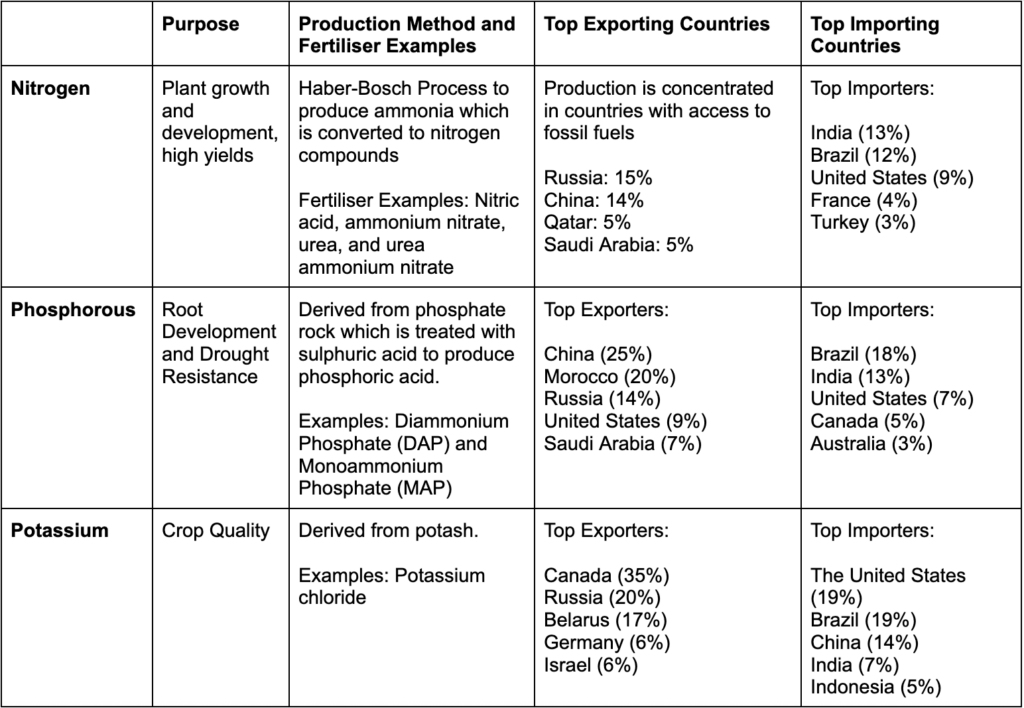

Mineral fertilisers are composed of three key macronutrients: Nitrogen, Phosphorous, and Potassium which cannot easily be substituted. Due to the uneven distribution of natural resources and the reliance on fossil fuels for nitrogenous fertilisers, the global fertiliser market remains highly concentrated among a limited number of exporters, heightening susceptibility to supply disruptions and food security risks. (See Table 1). Among the three macronutrients, Russia is a leading exporter across all categories, China dominates Nitrogen and Phosphorous exports, and Canada holds the largest market share in Potassium exports.

Table 1: Breakdown of Key Fertiliser Macro-Nutrients and Top Exporters and Importers

Source: OECD

Few alternatives to mineral fertilisers are commercially viable and widely available. For instance, burgeoning alternatives such as the transition from natural gas to renewable-based “green” ammonia are still long-term aspirations. Given that the bulk of green ammonia is concentrated in the United Arab Emirates (UAE), Saudi Arabia, and Oman, these markets may replicate the same trade risks as traditional fertiliser exports. Moreover, despite established green ammonia policy objectives in India and Morocco, green ammonia has not yet reached a state of cost-competitiveness to scale beyond pilots towards commercial deployment.

21st Century Crises Reveal Entrenched Dependencies on Concentrated Fertiliser Supply

Russia-Ukraine war exposed fertiliser dependencies, but price spikes and fertiliser shortfalls were largely placated by trade diversification and alternate transhipment corridors

As the leading supplier of nitrogen, second in potassium, and third in phosphorus fertiliser exports, Russia clearly dominates the global fertiliser market. At the onset of its war on Ukraine,

Russia-Ukraine war exposed fertiliser dependencies, but price spikes and fertiliser shortfalls were largely placated by trade diversification and alternate transhipment corridors

fertiliser prices spiked due to economic barriers from global restrictions, building upon price increases from fossil fuel fertiliser feedstocks. However, price spikes were offset by international sanction exemptions, alternate transhipment corridors avoiding Black Sea ports, and trade loopholes. Although international sanctions largely exempted Russian fertiliser exports, EU sanctions still banned potash imports from Belarus, and financial systems leveraged to purchase agricultural products were implicated to dissuade purchases from Russia. Russia overcame these challenges through alternate transhipment corridors through friendly countries and transhipping Belarus potash exports through Russia. Countries either diversified away from or doubled down on Russian fertiliser imports, with Brazil increasing imports from Canada to offset fertiliser decline from Belarus, and India, with a more amenable diplomatic posture to Russia, increasing Russian and Belarus fertiliser imports. Other fertiliser exporting countries such as China reduced diammonium phosphate (DAP) and urea exports to meet domestic demand, with DAP trade falling by 43 percent and urea trade falling by 47 percent between 2021 and 2022. Nevertheless, smallholder farmers, particularly those in Sub-Saharan Africa, continue to bear the brunt of impacts due to limited fiscal space from governments to subsidise high costs.

Hormuz chokepoint blockages during the US-Israel War on Iran exposes limitations in fertiliser diversification pathways

The US-Israel War on Iran immediately led to trade blockages at the Strait of Hormuz, a crucial chokepoint transiting 30 percent of global fertiliser trade. The Gulf Cooperation Council (GCC) countries represent a dual-risk hub, acting as critical exporters of natural gas and fertiliser. First, the Gulf is a critical producer of nitrogenous-based fertilisers such as urea, with India purchasing more than 40 percent of its urea from the region, and Australia depending on Gulf states for more than half of its urea. In addition, the Gulf states represent the single largest sulphur exporter. Sulphur is leveraged to convert phosphate rock into essential DAP and monoammonium phosphate (MAP) fertilisers. Morocco and China represent the world’s largest phosphate producers, relying significantly on sulphur imports from the Gulf. To illustrate, Morocco imports roughly 3.7 million metric tonnes, while China imports 4 million metric tonnes. Without sulphur inputs, phosphate production may become constrained, raising production costs and limiting trade diversification pathways.

Hormuz chokepoint blockages during the US-Israel War on Iran exposes limitations in fertiliser diversification pathways

In addition, coinciding conflicts between the US-Israel-Iran and Russia-Ukraine have damaged infrastructure, hampering immediate export capacity. For example, Iranian drone attacks on the Qatar Fertiliser Company (QAFCO), the world’s largest site for urea exports supplying 14 percent of global urea, halted production. Moreover, Ukrainian drone attacks on Russia’s Dorogobuzh plant which produces approximately 11 percent of Russia’s ammonium nitrate, has resulted in Russian fertiliser restrictions. These logistical and infrastructure challenges are compounded by protectionist policies of countries such as China who, like the onset of the Russia-Ukraine war, restricted urea exports to meet domestic demand. Although export restrictions offer short-term relief, they raise prices and exacerbate global price volatility.

The supply constraints imposed by these crises limits trade diversification pathways for global south countries rapidly approaching critical planting seasons. India is most concerned about urea availability, its most widely-deployed fertiliser. To counter supply constraints, India is leveraging its domestic stockpiles, but continues to engage with Morocco and Russia, while expanding outreach to Indonesia for urea-specific trade substitution. Still, Indonesia intends to prioritise domestic demand, and import quantities will be less than those from the Gulf. Given price hikes, Brazilian farms have switched to less expensive, lower-concentration products such as ammonium sulfate. However, despite being cheaper per tonne, ammonium sulfate requires more volume and logistical handling, raising overall costs. Overall, the burden of high fertiliser prices will likely fall on small-holder farmers in lower-income countries with tight fiscal space. While subsidies protect farmers from immediate price shocks, they also reduce financial resources directed towards rural or infrastructural development. The alternative is reduced fertiliser applications, leading to lower crop yields and constrained global food supply.

Compounding Crises Strengthens the Case for a Renewed Approach to Fertiliser Resilience

Supply-Side: Storage, Organic Fertiliser, and Low-Carbon Fertiliser Alternatives

To mitigate future immediate shocks, countries should collectively strengthen regional and global fertiliser reserves and maintain open trade. Replicating strategies from the hydrocarbon sector’s global reserve system for crude oil, developing shared regional infrastructure, strengthening regional trade to absorb shocks offers a few pathways. For instance, the ASEAN Plus Three Emergency Rice Reserve mechanism can be expanded to include fertiliser stockpiles. However, storing concentrated fertilisers requires logistical and safety considerations due to risks of groundwater chemical contamination, corrosion, and damage from moisture exposure.

Increasing financing, research, and development to scale locally-cultivated biofertilisers will help increase circularity while reducing dependencies on fragile supply chains. Biofertilisers can be derived from agricultural waste and crop residues or novel methods like sargassum. Scaling the biofertiliser market will be especially crucial for tropical and subtropical regions with vulnerable small-holder farmers like those in Latin America and the Caribbean. Unlike chemical fertilisers, biofertilisers absorb nutrients better than chemical fertilisers in high soil acidity environments, promote long-term soil health, and reduce farmer production costs.

Studies also highlight the potential for key macro-nutrients to be extracted from human waste, sewage, and manure. While companies in China, the United States, Canada, and Europe have initiated large-scale implementation of fertiliser extraction from sewage, the practice remains largely nascent and untapped in Southeast Asia. Notably, organic fertilisers may not always be exact substitutes for inorganic fertilisers due to uneven distribution of raw biomass availability and differing concentrations of nutrient content. Thus, this approach is best suited for areas rich in organic waste and compost demand. Nevertheless, significant waste output, insufficient sanitation infrastructure, and fertiliser demand breeds ground for enhanced waste management, nutrient recovery, and circularity co-benefits. At a national level, promoting blended organic and chemical fertiliser use would facilitate a viable intermediate transition.

Moreover, deepening investments in green ammonia in India and Morocco would offer a low-carbon alternative, but requires overcoming regulatory barriers and misalignment between producers, offtakers, infrastructure, and policymakers. Distributed green ammonia production has already proved to be a key competitor to imports, serving local smallholder farmers in Kenya without subsidies.

Demand-Side: Demand-Side Regulation, Monitoring, and Transparency

Long-term, governments can re-design subsidy regimes to incentivise proper fertiliser application methods (right source, time, place, and quantity) while providing transitional subsidies to offset risks of shifting to organic alternatives. In regions like South Asia, where long-term subsidies have historically driven nitrogen-based fertiliser overuse, implementing gradual and tailored policy shifts as opposed to abrupt bans would protect against inadvertent food system destabilisation while also increasing farmer acceptance.

Furthermore, replacing widespread mineral fertiliser messaging with localised guidance on bio-fertiliser production and crop rotation methods will enable farmers to leverage resources more effectively, promoting biodiversity and soil health. Deploying satellite remote sensing can also help monitor actual fertiliser consumption. When paired with support to smallholder farmers to adopt Low External Input Sustainable Agriculture (LEISA), demand for synthetic fertilisers would reduce.

Trade diversification is often positioned as a key strategy to assuring resilience. Given the highly concentrated nature of the global fertiliser market, safeguarding trade flows in anticipation of the next global shock will also require bolstering regional and global fertiliser storage reserves, advancing research and investments in circular and low-carbon bio-fertiliser alternatives, and improved demand-side regulation. Supplementing diversified trade partnerships with stronger domestic capacity will ultimately help improve food system resilience.

Leigh Mante is Junior Fellow, Climate and Energy, ORF Middle East.