Expert Speak | 03 March, 2026

The Gulf’s Regional Opportunities Along the Critical Minerals Value-Chain

Spotlight

- Coordinating to build a critical minerals value-chain can offer Gulf countries leverage in the new currency of global power.

- The Gulf countries can address capacity gaps in the critical minerals sector by synergizing their comparative advantages.

- Cooperating in the sector offers an opportunity for strategic economic coincidence in the Gulf while avoiding wasteful overlaps.

Coordinating to build the region’s leverage globally is a model that Gulf actors have fine-tuned over decades as part of the Organization of Petroleum Exporting Countries (OPEC). It is, crucially, also a model that has enabled the building of a global clout collectively through the leveraging of their natural resources. This article makes the case that similar coordination in the vital Critical Minerals sector known as the new oil today, could enhance particular regional positions along the value-chain, with benefits percolating to each, and the region as a whole.

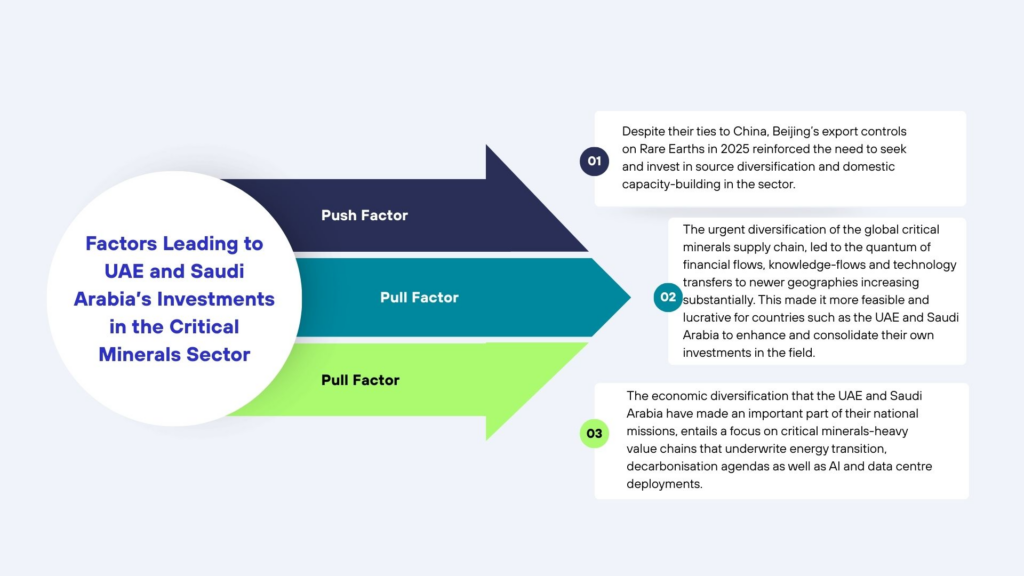

The relevance of Critical Minerals to regions such as the United Arab Emirates (UAE) and Saudi Arabia, and their resultant investments in the sector, may be contextualized through the following push and pull factors-

Table.1 Factors Leading to UAE and Saudi Investments in the Critical Minerals Sector

Transforming their positions along the Critical Minerals value chain will involve regions such as UAE and Saudi Arabia partaking more in the midstream and downstream processes of refining, separation, production of final products and recycling. Their present unique circumstances in the sector may be outlined through the following snapshot-

Table. 2 UAE and Saudi Arabia’s Strengths and Weaknesses in the Sector

Saudi Arabia’ Comparative Advantages

Domestic reserves including heavy Rare Earth Elements (REEs) concentrated in the 600,000 sq.km block of the Arabian Shield offer the region a significant advantage. In addition to the estimated $2.5tn valuation of it, the possession of domestic mineral reserves mitigates a crucial supply chain vulnerability. Once refining and processing capacities are developed domestically, this mineral wealth would prove to be a turning-point for the region’s role along the value-chain.

Coordination in the vital Critical Minerals sector known as the new oil today, could enhance particular regional positions along the value-chain, with benefits percolating to each, and the region as a whole.

Saudi Arabia’s second advantage lies in the scale it can build based sheerly on the size of the local population. The Public Investment Fund’s (PIF) ambitious target of 500,000 Ceer EVs by 2030 is a testament to this potential in absorption capacity.

Its external partnerships offer Riyadh its third point of advantage. Primary among these is the US Department of War supported MP Materials partnership of $110 with Ma’aden. Additionally, through the Future Minerals Forum (FMF), Riyadh has also positioned itself quite effectively at the heart of the Critical Minerals conversations globally. The establishment and proposed coordination of the Hubs of Excellence at FMF 2026 demonstrates Saudi Arabia’s role in influencing global frameworks in the sector.

UAE’s Comparative Advantages

What the UAE lacks in domestic minerals wealth, it makes up with the robust access it has developed through mining partnerships, offtake agreements and the logistics infrastructure it has built across the geographies recently identified as the Critical Minerals Super Regions of Africa, Latin America, Central Asia, and West Asia. It has achieved this by deploying its formidable financial agency strategically through both public and private platforms to meet capacity gaps in many of these geographies.

In Africa, home to nearly 30 per cent of the world’s Critical Mineral reserves, for instance, the UAE’s investment already stood at more than $110bn between 2019-2023. It is a segment in which the UAE’s ADQ and Orion Resource Partners have also developed a substantive footprint, through partnerships with the US Development Finance Corporation (DFC).

Seeking to match the high subsidisation that first-movers like China managed in the domain decades ago, can impose prohibitive costs on relatively newer players in the Critical Minerals sector.

Notably, the UAE has a relative head-start in refining, both through external partnerships, as well as the country’s ongoing work with American and Italian public and private entities. The Khalifa Economic Zones Abu Dhabi’s Lithium processing plant is a case in point. The country has extended these international partnerships also to working on the relatively small but crucial EV battery recycling segment such as the partnership it has developed with India.

Capacity gaps vis a vis first movers

Delineating the comparative advantages of each actor effectively highlights the differentiated capacity gaps of the other. The shortfalls are further compounded by the following considerations that are inherent to the sector as a whole:

First, the lead-times in greenfield mining projects coming online (17.9 years), in the development of refining and processing capacity (4-8 years), and in the development of a skilled workforce (4-8 years) are considerably high.

Second, there are also implications of innovations in battery chemistries that today’s investors have to factor in. In answer to Chinese restrictions on REE exports to the country post 2010, for instance, Japanese companies such as Honda and Daido Steel re-engineered their battery chemistries to create more heat-resistant neodymium magnets that reduced the amount of REEs in their composition. Such re-engineering will eventually alter the demand matrix of critical minerals and change the final net value of the investments made in the sector today by those producing or refining. Also pertinent is China’s ability to undercut competition by flooding the market through significant price reductions of its own output.

Third, the ability to remain competitive given these considerations while seeking to match the high subsidisation that first-movers like China managed in the domain decades ago, can impose prohibitive costs on relatively newer players in the Critical Minerals sector. The monopoly China has already established in the field is substantial, and cannot realistically be challenged in the short to medium term. Although, challenging legacy actors such as China is a daunting task for any country in the Critical Minerals space, it is not always avoidable. UAE’s IRH’s bid for Zambia’s Mopani Copper mines is the first known instance of how the Gulf actors are beginning to directly compete with China for a major Critical Minerals asset. It is unlikely to be the last.

Building on Strengths

The substantial reservoir of patient capital available in the UAE and Saudi which is relatively less risk-averse, together with process engineering expertise derived from legacy hydrocarbon sectors, can be synergised with the following pathways to mitigate these complexities:

The substantial reservoir of patient capital available in the UAE and Saudi which is relatively less risk-averse, together with process engineering expertise derived from legacy hydrocarbon sectors, can be synergised.

There is potential for a Critical Minerals Trading Hub in the region. The region has for decades now been a commodity trading hub. Given their current stakes in the sector, it is reasonable to expect a successful iteration for Critical Minerals to develop in the region as well. In October 2024, UAE’s International Resource Holding (IRH) declared that they would work towards setting up a trading hub for copper trading. Saudi’s Public Investment Fund (PIF) has made a similar declaration. In the recently concluded Future Minerals Forum, 2026, Saudi’s Minister of Mining and Minerals Alkhorayef alluded to a similar role through the creation of a specialized platform to balance supply and demand of minerals. The objectives of both, could fructify and benefit from a pooling of resources and expertise.

Notably, the fact that neither country is a full member of the Extractive Industries Initiative (EII) is a matter of concern, and must be addressed if credibility is to be gained as a trading or arbitration hub.

A second initiative worth exploring could be the creation of an energy transition equipment hub. Critical minerals are a vital feedstock in energy transition manufacturing and thus central to the economic diversification and decarbonization objectives of both countries. The UAE has begun working with countries like Australia to establish itself as a viable manufacturing base for renewable energy equipment. Relatedly, the UAE and Saudi Arabia could coordinate effective industrial sequencing efforts to integrate both waste-recovery and recycling of critical minerals from transition infrastructure into their manufacturing models. For example, Emirati partnerships with Japanese firms have focused on re-engineering industrial processes to reduce the quantity of critical minerals in manufactured products. Again, with their access to Critical Minerals, the two countries could work towards developing a niche in battery storage, widely regarded as the next frontier in the energy transition.

With their access to Critical Minerals, the two countries could work towards developing a niche in battery storage, widely regarded as the next frontier in the energy transition.

The development and integration of AI in mining could serve as the third pathway to value-creation in the sector. The Sovereign Wealth Funds (SWF) of both countries have made substantial investment in the Artificial Intelligence domain. The use and integration of AI processes can significantly improve discovery efficiency in mining processes. This would translate into shorter project timelines, especially for greenfield projects, and would enhance discovery efficiency. Additionally, robust supply chains of Critical Minerals such as silver, gold, copper, tin, tantalum, palladium, barite, boron, gallium, germanium, silicon and other REEs are a pre-requisite for the structural integrity, energy intensity, and performance enhancement of the Data Centres that both countries are increasingly prioritizing.

In their seminal work outlining the theory of Complex Interdependence, Robert Keohane and Joseph Nye contend that in an interconnected world, states are necessarily interlinked across a much wider matrix of considerations including, but not limited to, economic ties, social connections, and environmental issues. This explains the Gulf’s pragmatism underpinning the ability to work together where possible despite differences. The resultant stability is integral to the economic diversification and developmental ambitions of both the UAE and Saudi Arabia. How countries manage their resources, strengths, weaknesses, and differences in the sector together will largely determine whether they can identify and consolidate their niche along the Critical Minerals value chain. Coordinating can forge strategic coincidence and catalyse a coherent trajectory of leverage for the region in the emerging currency of resource wealth. Choosing to not do so would, conversely, result in a lost opportunity.

Cauvery Ganapathy, Fellow, ORF Middle East.