Expert Speak | 15 April, 2026

How Middle East Turmoil Reverberates Through Japan’s Energy System

Spotlight

- Japan’s Middle East dependency is structural, not just strategic, creating a web of dependencies that no single policy lever can quickly unravel.

- Japan’s post-Fukushima shift to fossil fuels, a gap filled almost entirely by Middle Eastern imports, compounded a pre-existing structural vulnerability that is still reverberating through its energy system today.

- Tokyo’s diversification toolkit is real but moves slower than geopolitics. US crude imports, North American LNG investments, nuclear restarts and renewables buildout are all underway, but are constrained by time, cost and configuration.

Japan has long been described as a country with deep “energy angst”, an understandable sentiment for an industrialised island nation with almost no domestic energy resources. That anxiety has returned to the foreground with force amid the ongoing Middle East crisis, which has once again exposed the structural fault lines in Japan’s energy supply. Analysts and governments alike have highlighted Japan as one of the developed economies most acutely vulnerable to disruptions in the Gulf. What follows examines the roots of that dependence, the real costs of disruption, and the limited options Tokyo possesses to gradually reduce its exposure over time.

A Dependency Decades in the Making

Despite being the world’s fourth-largest economy, Japan produces only around 15 percent of the energy it consumes domestically, leaving it structurally dependent on imports across all fuel types. Of all the vulnerabilities this creates, its reliance on the Middle Eastern oil and gas, is most consequential.

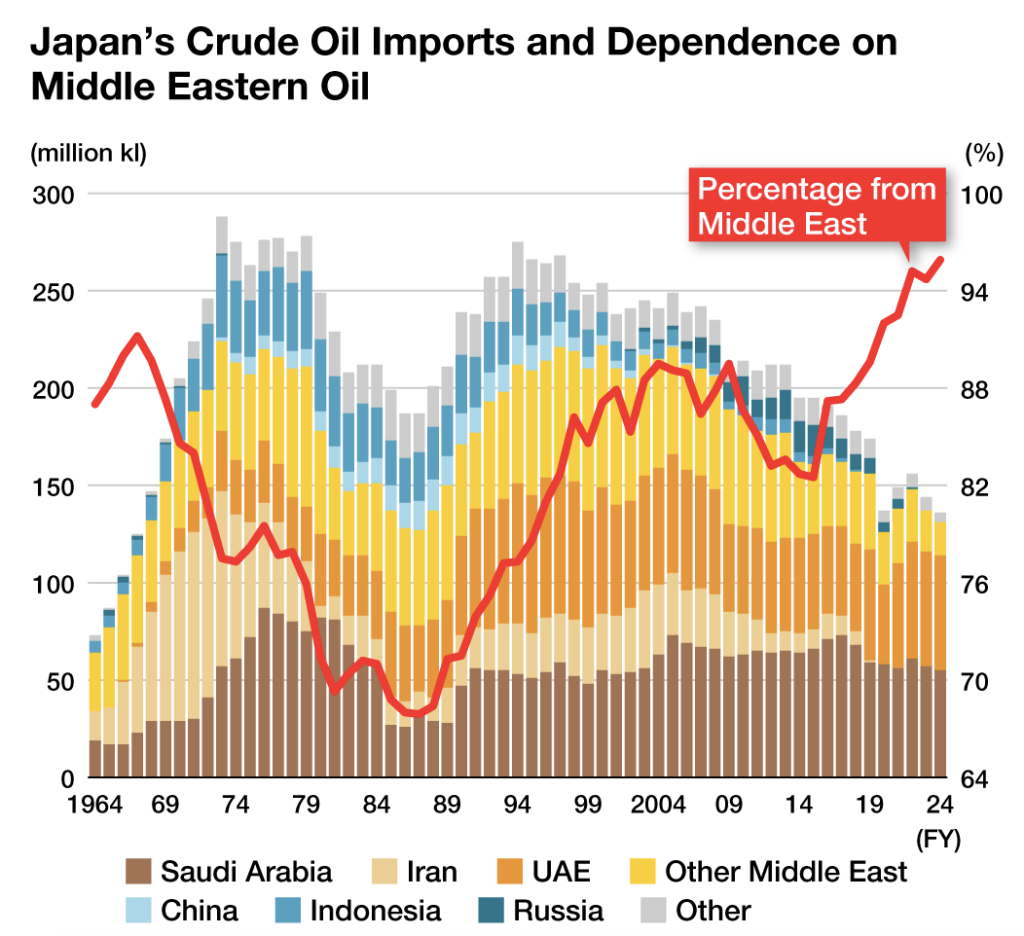

As of the first half of 2025, Japan sourced more than 95 percent of its crude oil feedstock from Middle Eastern suppliers. Moreover, Japanese refineries were built to process medium and heavy sour crude, the grades that define Persian Gulf exports. That configuration has made the Middle East not merely a convenient supplier but a structural cornerstone of Japan’s energy system.

Source: nippon.com

Supply patterns remain highly concentrated. The United Arab Emirates (UAE) alone accounts for roughly 44percent of Japan’s crude imports, followed by Saudi Arabia (40 percent), Kuwait (7 percent) and Qatar (4 percent). The complementarity between refinery configuration and Gulf crude grades has locked in this dependence across decades of long-term contracts.

For liquefied natural gas (LNG), the picture is somewhat more diversified. Japan remains the world’s second-largest LNG importer, and Australia is its largest supplier, accounting for roughly 38 percent of imports in recent years. Other major suppliers include Malaysia (16 percent), the United States (10 percent) and Russia (9 percent), with the Middle East, primarily Oman, Qatar and the UAE, accounting for about 11percent of LNG imports directly.

Yet roughly 83 percent of LNG leaving the Persian Gulf transits through the Strait of Hormuz. Any disruption to that chokepoint therefore ripples across global gas markets, raising spot prices for Asian buyers regardless of where their contracted volumes originate.

Japan’s fossil fuel dependence was also deepened by a domestic policy choice. Prior to the March 2011 Fukushima disaster, nuclear power supplied close to 30 percent of Japan’s electricity. The subsequent closure of the entire reactor fleet forced utilities to replace that generation with imported fossil fuels. Fossil fuels’ share of electricity generation surged to 84 percent in 2015, up from 64 percent in 2010, before gradually retreating to around 69 percent by 2024 as solar expanded and some reactors restarted.

These structural factors have reinforced Japan’s enduring dependence on imported fuels and deepened its exposure to geopolitical developments in the Middle East.

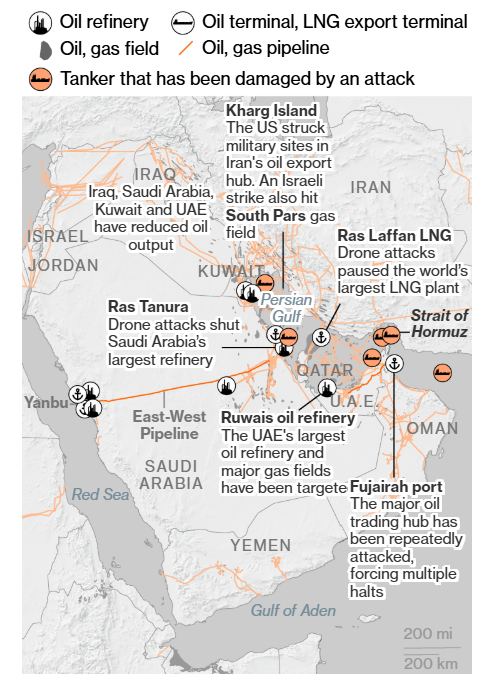

The Hormuz Calculus

The Strait of Hormuz is the world’s single most consequential energy chokepoint and Japan’s most critical supply artery. At the time of writing this article, a two-week ceasefire has been announced, but the events of the past several weeks have demonstrated how quickly theoretical risk can become operational reality.

Energy Disruptions in the Middle East

Source: Bloomberg

Brent crude, trading at around US$72 per barrel before the conflict intensified, surged past US$110 by end-March 2026. The Japan Korea Marker (JKM), Asia’s benchmark LNG spot price approximately doubled, as tighter supply intensified competition between Asian and European buyers for available cargoes.

The macroeconomic transmission channels to Japan’s economy are direct and severe. A US$10 increase in crude prices is estimated to raise Japan’s inflation by around 0.3 percentage points. At sustained prices above US$120 per barrel, it is estimated that Japan could slip into stagflation, with GDP roughly 0.6 percent below baseline in 2026. The situation is compounded by Japan’s fiscal position: the country already carries the largest public debt burden among developed economies, at roughly 260 percent of GDP, leaving limited room for large-scale energy subsidy programmes.

Higher fuel prices feed directly into Japan’s trade balance and household energy costs. The trade deficit ballooned to over JPY 20 trillion in 2022 following the Russia–Ukraine energy spike, and the current crisis risks a repeat. Utilities including TEPCO and Chubu Electric have signalled plans to pass rising procurement costs through to retail tariffs from April 2026, with annual household electricity bills projected to increase by around JPY 15,000.

Japan maintains significant emergency petroleum stockpiles, approximately 254 days of crude oil reserves as of end-2025, combining government and industry holdings. This reserve, among the largest in the OECD, provides meaningful insulation against short-term physical supply disruptions. But stockpiles address volume shortfalls, not price shocks; as long as global markets clear at elevated prices, Japanese buyers will face higher costs regardless of reserve levels.

The LNG dimension introduces an additional layer of complexity that stockpiles cannot address. Unlike crude oil, LNG cannot be held in long-term strategic reserves once regasified, and Japan has no comparable buffer mechanism, though the government has introduced a Strategic Buffer LNG (SBL) framework under the Economic Security Promotion Act. The Oxford Institute for Energy Studies estimates that a one-year Hormuz closure would reduce global LNG supply by roughly 15 percent as compared to 2024 levels, a shortfall that new volumes from Australia, the US and Canada could only partially offset. With LNG accounting for approximately 33 percent of Japan’s electricity generation in 2024, a prolonged Gulf gas disruption would translate rapidly into tighter power markets and higher electricity prices.

The damage to Qatar’s Ras Laffan Industrial City, the world’s largest LNG export facility, also underscores how deeply embedded Japan is in Qatar’s gas sector. Japanese engineering firm Chiyoda Corporation was among the contractors involved in the massive North Field expansion before the conflict forced construction to halt. Within hours of the ceasefire announcement, Chiyoda signalled it was considering a return to on-site work at Ras Laffan, a cautious sign of recovery, but also a reminder that Japan’s stake in Gulf energy infrastructure is not merely financial but also industrial and the product of decades-long cooperation.

Options on the Table: Diversification, Nuclear, and the Long Game

Japan is not without options, but none of them are quick or costless. The country’s energy establishment has been grappling with diversification for decades, with efforts accelerating after the Russia–Ukraine conflict demonstrated the risks of concentrated supplier dependence. Three broad pillars define Tokyo’s response: continued diversification, potential momentum in restarting of nuclear capacity, and reshaping the power mix through renewables and grid modernisation.

On the crude oil front, Japanese refiners have begun sourcing non-Middle Eastern feedstocks, though refinery configuration constraints remain significant. In 2025, Japan imported a record volume of US crude, almost double than 2024. Combined with sourcing from Africa, Latin America and Oceania, this effort helped reduce the Middle East’s share of crude feedstock from 95.4 percent in 2024 to 93.5 percent in 2025, incremental progress given that refineries designed for heavy sour grades cannot rapidly or cheaply switch to lighter alternatives.

For LNG, diversification is more advanced but also more complex. Japan’s import portfolio already spans Australia, Malaysia, Russia’s Sakhalin-2 project and the United States (US). Since mid-2025, Japanese energy companies have deepened their upstream exposure in North American gas. Mitsubishi’s US$ 5.2 billion acquisition of Haynesville Basin producer Aethon Energy, JERA’s USD 1.5 billion Haynesville investment, Tokyo Gas’s pledge to direct over half its overseas budget to the US, and JAPEX’s US$ 1.3 billion Colorado and Wyoming acquisitions collectively reflect a strategic pivot toward equity participation in North American supply chains. Yet as the current crisis has demonstrated, portfolio diversification cannot insulate Japan from global price shocks when supply tightens simultaneously across multiple nodes.

Nuclear restarts have long been touted as the most structurally significant lever available and one that has gained renewed political momentum. Japan’s 7th Strategic Energy Plan, committed to maximising existing reactor use, targeting around 20 percent of electricity from nuclear by 2040. In February 2026, TEPCO restarted Unit 6 of the Kashiwazaki-Kariwa Nuclear Power Station, bringing the active fleet to 15 reactors with 33 GW of combined capacity. According to the US Energy Information Administration, a single unit of this plant could displace approximately 1.3 million tonnes of LNG imports annually, equivalent to roughly 10 percent of Japan’s Gulf LNG imports from 2025.

However, ambition exceeds near-term delivery capacity. Analysts estimate that nuclear may reach only around 12 percent of electricity generation by 2030 under optimistic assumptions and could decline further by 2040 as ageing reactors are decommissioned. Local opposition, safety reviews and regulatory timelines continue to slow restarts. METI’s own modelling acknowledges that if nuclear and renewables both underperform, fossil fuels could supply around 45 percent of Japan’s electricity as late as 2040.

Renewables form the third pillar, driven primarily by solar, offshore wind and geothermal expansion. Japan’s Organisation for Cross-regional Coordination of Transmission Operators has identified inter-regional transmission reinforcement as a priority investment, and the government’s GX (Green Transformation) programme allocates funding for grid modernisation alongside clean power deployment. The Climate Bonds Initiative estimates that a decisive clean power transition could require around JPY 38 trillion in investment by 2035, roughly a quarter of the broader GX programme. The price shocks of 2022 and again in 2026 have sharpened the fiscal logic: avoided fossil fuel import costs could offset much of that expenditure over time.

Thus, crude diversification, LNG upstream investment, nuclear restarts and renewable expansion are complementary rather than competing strategies. None offers a rapid solution in isolation. Collectively, they form the foundation of Japan’s long-term attempt to reduce the structural vulnerability that ties its energy security to geopolitical events thousands of kilometres away.

Structural Vulnerability, Incremental Escape

Japan’s energy relationship with the Middle East is not a policy choice that can be reversed by decree. The current disruption has underscored that the costs of this dependence increase with each successive crisis. Each price spike expands the trade deficit, exerts pressure on the yen, raises household energy bills, and complicates monetary policymaking for the Bank of Japan. Even after a ceasefire, the supply consequences are likely to persist.

With sustained policy commitment, the goal should not be seen as independence from Middle Eastern energy reliance but as resilience, ensuring that any future disruptions find Japan less exposed than previous ones.

Parul Bakshi is Fellow, Energy and Climate, ORF Middle East.