Expert Speak | 15 April, 2026

Oman’s Personal Income Tax: A Case of Fiscal Signalling

Spotlight

- Oman’s planned personal income tax is a shift beyond the rentier model

- The tax is set to target the top one percent and that is less about redistribution and more about macroeconomic signalling and creditor confidence

- Oman is positioning itself as a regional outlier in fiscal reform

Introduction

The oil price collapse of 2014, when crude fell from about US$100 to US$50 per barrel, marked a turning point for fiscal policy in the Gulf Cooperation Council (GCC) states. Governments began steering their economic strategies toward diversification, stronger budgetary discipline, foreign investment, and the introduction of new tax instruments, including indirect taxes, corporate taxes, and direct taxes.

The reform marks a deliberate recalibration of the rentier social contract, prioritising credibility and sustainability over redistribution.

As part of Oman’s broader effort to move beyond hydrocarbons and diversify its fiscal base, the small open economy (SOE) plans to introduce a five percent personal income tax on individuals earning more than RON 42,000 annually (approximately US$109,000) with a roll-out from January 2028. This threshold applies to roughly one percent of the population, signalling a progressive approach that initially targets top earners. Oman’s personal income tax can be best understood not as a revenue tool, but as a calibrated signal of fiscal discipline aimed at reinforcing creditor confidence and macroeconomic stability. It marks a deliberate recalibration of the rentier social contract, prioritising credibility and sustainability over redistribution.

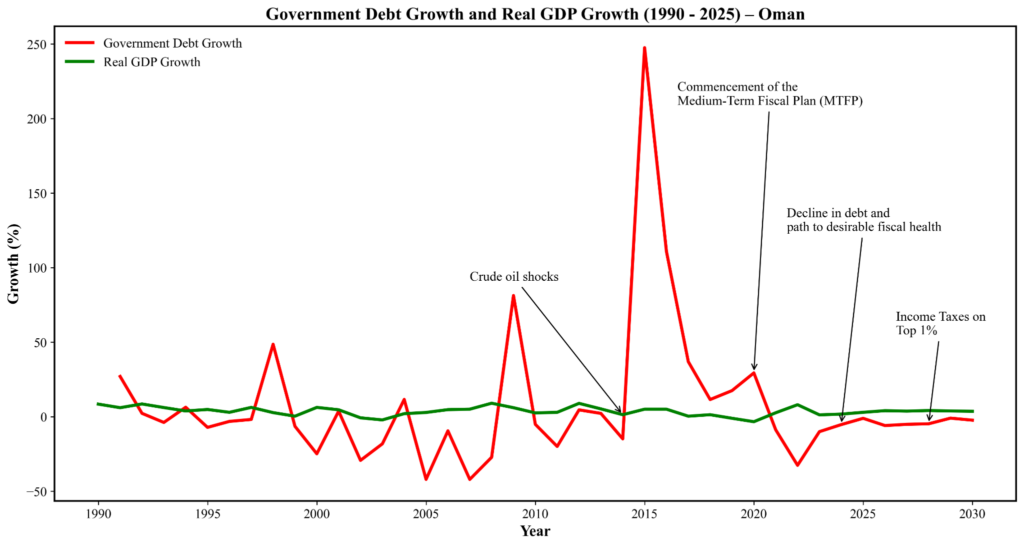

Figure 1: Government Debt and Real GDP for Oman from 1990-2025 (Growth Series)

Source: Authors’ Own. Data from the IMF. Prepared using Matplotlib.

Oman’s Early-Mover Advantage

The six GCC economies have historically functioned as rentier states, where a substantial share of national income is derived from rents, defined as income generated from natural resources, particularly oil. However, the long-term sustainability of the rentier model has increasingly come under scrutiny. Volatility in global oil prices, rapid population growth that strains the traditional social contract, and rising pressures on public sector employment have intensified calls for economic diversification across the region. One important dimension of this transition is fiscal or revenue diversification, which involves reducing dependence on hydrocarbon revenues by developing alternative sources of government income.

Compared to its GCC peers, Oman possesses significantly lower natural resource rents than major hydrocarbon producers such as Kuwait and Saudi Arabia. This relative resource constraint, combined with higher fiscal pressures and a more limited sovereign wealth buffer, has compelled Oman to adopt a more pragmatic and fiscally realistic policy approach. These structural factors, together with decisive political leadership, have positioned Oman as a first mover within the GCC in pursuing reforms such as the introduction of new personal income taxation frameworks.

Broadly, the Sultanate’s policy response to the oil shocks and the resulting fiscal pressures has rested on three pillars: (a) spending more efficiently, (b) broadening existing revenue bases, and (c) prioritising debt reduction. Taken together, these measures strengthened Oman’s fiscal position and helped drive a significant decline in public debt by 2024 (Figure 1). These decisions reflect the Sultanate’s fiscal health considerations and its long-term goal of achieving balanced and sustainable economic growth.

Notable achievements in recent years include the decree of the Public Debt Law, which set a decision to establish a Public Debt Management Committee (DMC). The committee is responsible for developing a framework for public debt management strategies and policies by reviewing the annual borrowing plan to ensure the sustainability of public debt and its growth rate. On top of this, Oman’s sovereign wealth fund (the Oman Investment Authority) reduced its companies’ debt by 24 percent and increased its contribution to the State’s General Budget, exceeding RON 6bn (US$15.6bn) from 2016 to 2023.

While the income tax may not be the saviour for government revenues, it boasts an important signal for creditors that the Sultanate is serious about charting a fiscal path that is unique in the Gulf region.

By edging towards a stable and diversified revenue base, the personal income tax introduction marks a credible inflection point in Oman’s fiscal transformation, sending a clear signal to creditors that diversification is no longer aspirational but underway. Notably, as part of the 11th Five-Year Development Plan (2026–2030), the share of non-oil revenues is expected to increase to around 37.4 percent of total revenues by the end of 2030. Still, Oman forecasts it will have an estimated average yearly deficit of RON 666mn (US$1.7bn) during these coming years, mainly because it aims to spend significantly on development, economic transformation projects, and its social protection system. A personal income tax would anchor Oman’s fiscal consolidation, reinforcing the hard-won credit rating upgrades that are now unlocking more favourable borrowing conditions — and the capital needed to sustain its broader economic ambitions. Crucially, while the income tax may not be the saviour for government revenues, it boasts an important signal for creditors that the Sultanate is serious about charting a fiscal path that is unique in the Gulf region.

Oman’s move toward personal income taxation signals a deeper shift in revenue diversification and represents a structural attempt to offset the limitations of the traditional rentier model.

While other GCC states continue to pursue diversification primarily through economic and sectoral strategies, open economy initiatives such as attracting foreign direct investment, and the deployment of sovereign wealth funds, their revenue models still rely largely on indirect taxes, fees, levies, and corporate taxation, and other forms of diversification (economic, export, financial, labour market). In contrast, Oman’s move toward personal income taxation signals a deeper shift in revenue diversification and represents a structural attempt to offset the limitations of the traditional rentier model. In this respect, Oman maintains a clear first mover position within the GCC in advancing fiscal diversification.

Why the Top One Percent? Fiscal Discipline over Redistribution

The current income tax targeting the top one percent improves vertical equity, wherein people with higher income incur a greater tax burden and introduce a limited degree of tax progressivity in an economy characterised by volatile oil rents. Over the past two decades, Oman’s average national income has declined by nearly 37 percent, driven largely by external developments and successive economic shocks, beginning with the downturn following the global financial crisis in 2008 and oil shocks in 2014. The primary purpose of this tax is not redistribution in a developmental sense, but rather the re-marking of post-oil fiscal realism. It carries limited implications for income inequality reduction or large-scale redistribution and instead centres on improving state financing, building fiscal credibility, political-economy signalling and building macroeconomic resilience.

The top one percent of income earners in Oman account for roughly 20 percent of total national income in recent years, approximately making up to US$22 billion in aggregate. This one percent primarily comprises high- and upper-income capital owners, concentrated across sectors such as real estate, industrial conglomerates, oil and gas, and other commercial activities.

The reform speaks to an external audience: fellow GCC states as well as institutions such as the IMF and the World Bank.

The reform’s impact can be understood across four distinct groups. First, for the state, it introduces a credibility-enhancing revenue instrument, signalling a gradual shift toward a more sustainable and rules-based fiscal framework. Second for the remaining 99 percent of earners below the threshold, the reform carries no direct burden, thereby preserving the existing social contract for most households. Third, for the targeted top one percent, outright capital flight remains unlikely given the low statutory rate of five percent and the inherently location-bound nature of their wealth and business interests. Instead, among those with access to sophisticated financial and legal arrangements, the more probable response is marginal income reclassification or quiet financial restructuring to reduce effective tax liabilities below the headline rate, rather than any wholesale relocation of capital. Fourth, and perhaps most consequentially, the reform speaks to an external audience: fellow GCC states as well as institutions such as the IMF and the World Bank. In this regard, Oman positions itself as the first Gulf state to cautiously recalibrate its social contract, doing so in a measured and deliberate manner, by design.

Oman in the International Tax Regime

Another key consideration surrounding the income tax relates to the issue of double taxation, which has implications like FDI and ease of doing business, harming Oman’s economy. As Oman seeks to continue its economic growth, and attract investment, it is important for it to proliferate its international tax agreements. Particularly, Double Taxation Agreements are important to keep the Sultanate globally competitive. Oman has been diligent in recent years to ratify at least ten double taxation agreements since 2014. An additional two with Bahrain and Kazakhstan are due to be ratified, amongst other discussions closing in the number of such agreements on 40.

The latest ten agreements have converged more on the OECD principle of taxing individuals in their primary residence rather than sources of income. This aligns Oman with international standards and though some taxation will be lost in the short run, it will have a longer-term success of attracting economic activities despite the increased reliance on taxation for revenues.

Conclusion

If successful and unamended, any expansion of the tax base or increase in rates remains a second-order question. The first-order priorities are clear: a more dynamic labour market, reduced reliance on state support, a financially resilient middle class, and deeper capital markets. The current reform is therefore best understood as a deliberate first step, not the endpoint.

Nonetheless, Oman has taken the risk of being a first mover amongst the Gulf countries. The risk is that, with crises such as the ongoing war, such initiatives and their core objectives may be undermined. Oman may be anticipating a scenario where creditor confidence is not sustained to the extent it hopes once the tax is rolled out. Consequently, Oman could still postpone or cancel the tax’s roll‑out while continuing to pursue its long‑term economic vision.

Manish Vaidya is Research Assistant, at ORF.

Mahdi Ghuloom is Junior Fellow, Geopolitics, at ORF Middle East.