Special Reports | 23 February, 2026 Download Report (PDF)

Mapping Gulf Sovereign Wealth Funds in the Global Energy Transition: Capital, Technology, and Diplomacy

Attribution: Parul Bakshi, Mapping Gulf Sovereign Wealth Funds in the Global Energy Transition: Capital, Technology, and Diplomacy, Observer Research Foundation Middle East, February 2026.

Introduction

Over the past decade, the Gulf’s political capitals have become increasingly important to understanding the geography of global state capital. The region’s sovereign wealth funds (SWFs) illustrate how financial power is now central to industrial strategy, technology acquisition, and clean-energy diplomacy. Together, Gulf SWFs account for about 40 percent of global SWF assets, and six of the ten largest funds worldwide, underscoring their systemic weight.1

Gulf SWFs are, however, no longer passive financial actors but system-shaping institutions. By absorbing first-mover risks in commercially immature sectors, they de-risk the transition for private investors, accelerate project pipelines, and create investable ecosystems aligned with national diversification and global climate objectives.

Their patient, long-horizon capital enables the transfer of technology, operational know-how, and manufacturing capability across borders, helping local markets scale complex industries more rapidly. In parallel, their outward investments have become a form of economic statecraft, projecting capital to forge industrial alliances, reshaping supply chains, and extending diplomatic influence across multiple regions.

Once synonymous with oil rents and fiscal stabilisation, Gulf SWFs have evolved into active engines of diversification, diplomacy, and technological leadership. Investment activity reflects this dominance, according to Deloitte, Gulf SWFs invested USD 82 billion in 2023 and USD 55 billion in the first nine months of 2024, accounting for nearly two-thirds of all sovereign wealth deployment globally.1 Their strategies now extend beyond asset management to shaping the direction of energy systems and strategic industries.

As the global energy transition accelerates, Gulf SWFs are emerging as central actors in new clean-energy supply chains. They are deploying patient, long- horizon capital into renewable energy, hydrogen, critical minerals, green industrial manufacturing, and smart-grid infrastructure; sectors that simultaneously support domestic economic diversification and extend Gulf strategic influence across the Global South and Global North.

Their expanding role also reflects a shift away from traditional passive wealth management toward more interventionist climate and industrial mandates, raising new questions about the robustness of emerging green investment frameworks.

The scale of their impact is significant given how Gulf Cooperation Council (GCC) SWFs are projected to control no less than USD 18 trillion in assets by 2030, a roughly 50-percent increase from today.2 Currently, the Gulf controls USD 4.9 trillion, representing 38 percent of all global SWF assets, concentrated primarily in the Abu Dhabi Investment Authority (ADIA), the Public Investment Fund (PIF), and the Kuwait Investment Authority (KIA).3

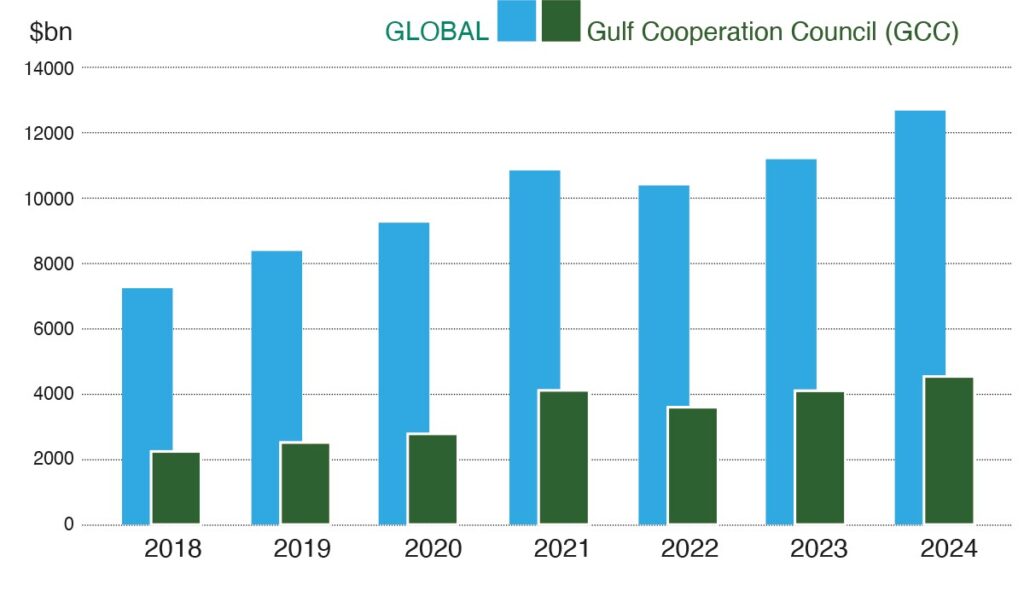

Figure 1: Total SWF Assets Under Management (AUM), in $bn

Source: Deloitte, 2025

Against this backdrop, this report undertakes a structured mapping of major Gulf sovereign and quasi-sovereign wealth funds (SWFs) in energy and clean-technology sectors. Its objective is to provide a concise, evidence- based landscape highlighting flagship transactions and partnerships, planned commitments, geographic footprints (Domestic/Global South/Global North), and the diplomatic linkages that enable or follow investment flows.

Scope and Coverage

This mapping focuses strictly on fund-level investments and commitments, where SWFs act as direct equity investors or formally announced co-investors. Domestic project developers and operating arms (e.g., QatarEnergy Renewable Solutions, national utilities, and IPP SPVs) are treated separately unless the SWF explicitly appears in the project’s equity or funding structure.

Many project details are based on public announcements, MoUs, and financial/ industry media reporting. These often indicate strategic intent rather than completed deployment. SWFs often use subsidiaries, affiliates, or third-party funds (LP positions) that can obscure direct ownership. Equity participation is recorded only when explicitly disclosed by the fund, project sponsor, or credible financial media.

It should be noted that this is not an exhaustive record of all SWF-funded energy or technology projects. Rather, it synthesises publicly available information to assess directional flows of capital and strategic intent across the Gulf’s leading funds.

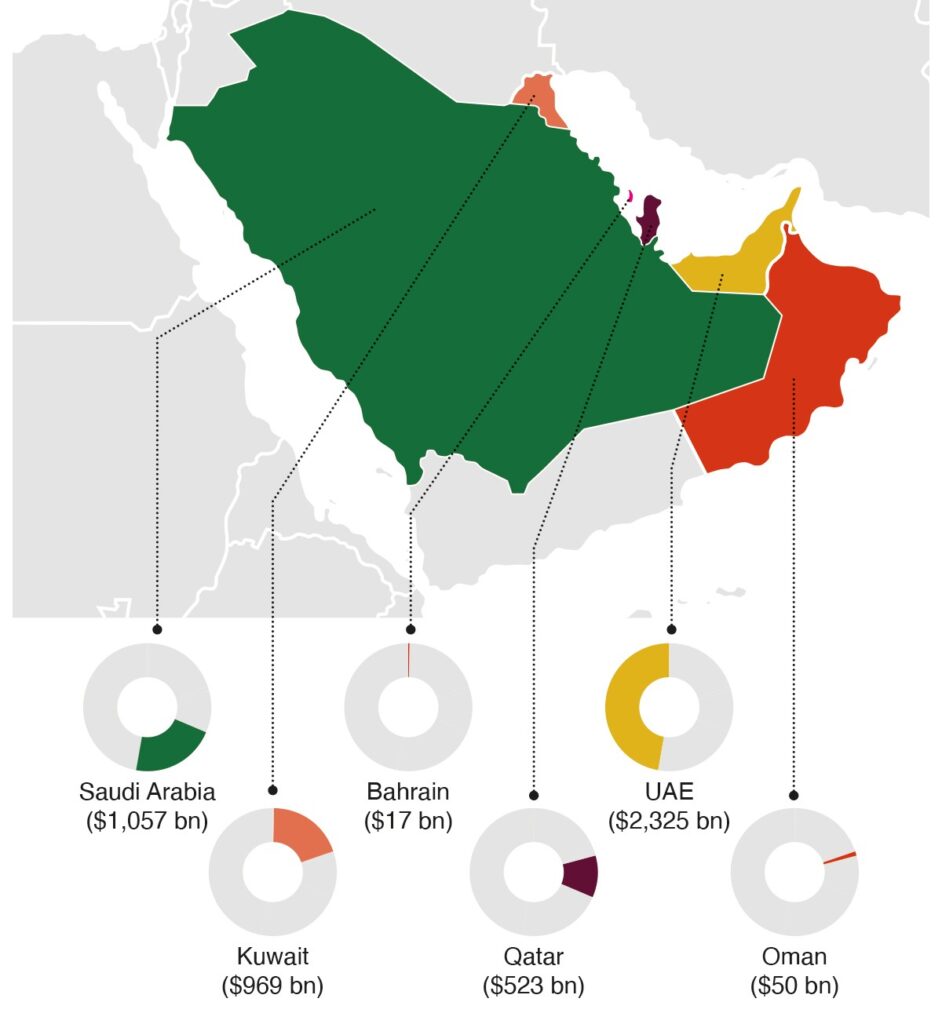

As the figure below indicates, a small number of Gulf SWFs hold a disproportionately large share of regional assets. To reflect the political geography of these systems, this report follows the four principal Gulf capitals—Abu Dhabi, Doha, Kuwait City, and Riyadh—each anchoring a distinct architecture of state capital and investment strategy.

Figure 2: Estimated Total GCC SWFs, by Country’s Assets Under Management

Source: Alhajaraf, 2025

The major Gulf SWFs included in this report are:

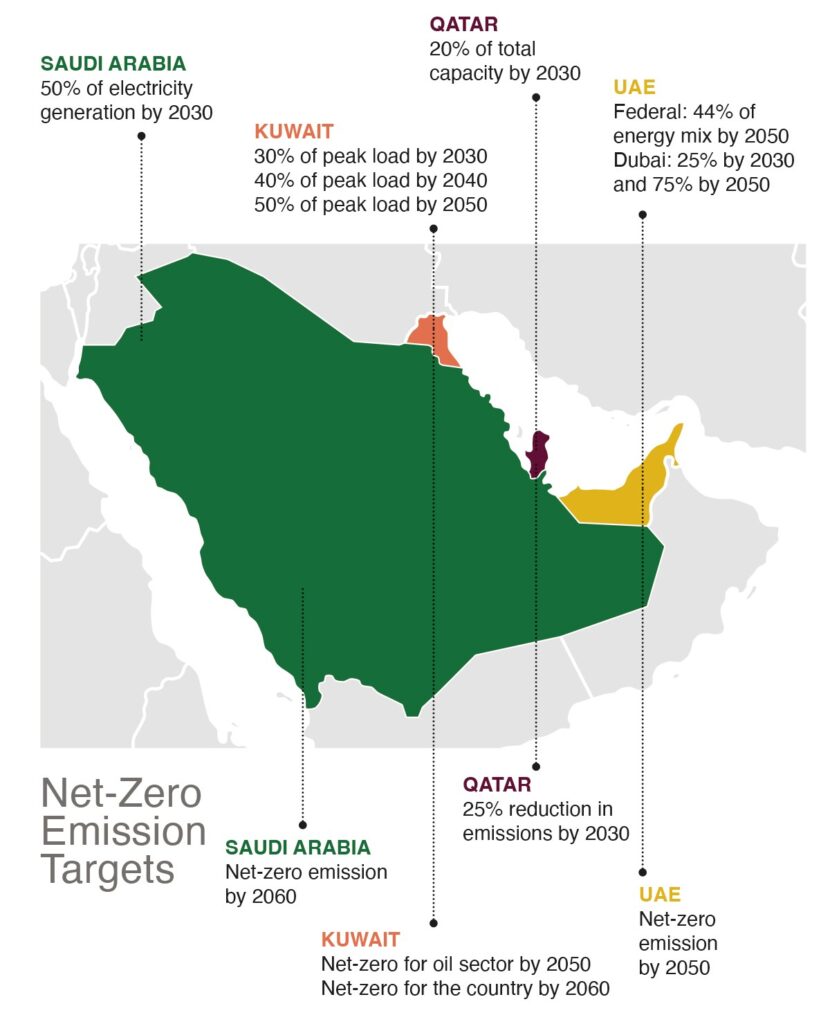

Across these four capitals, national decarbonisation strategies have been articulated alongside broader climate and competitiveness commitments. Their domestic energy targets and overseas investment patterns form part of a shared Gulf effort to reshape global energy systems while advancing long-term economic diversification.

Figure 3: Renewable Energy Targets

Sectors covered: Utility-scale renewables (solar, wind), green hydrogen and derivatives, grid and storage systems, green industrialisation (local manufacturing and supply-chain localisation), critical-minerals and mining tied to the energy transition, climate tech, and relevant finance instruments (green bonds, transition funds).

Together, these funds demonstrate how Gulf capital is shifting from passive wealth preservation to active global influence, reshaping domestic economies, enabling technology acquisition, and redefining the geography of the energy transition.

Read the report here.

Parul Bakshi, Fellow, Energy and Climate, ORF Middle East.

All views expressed in this publication are solely those of the author, and do not represent the Observer Research Foundation, either in its entirety or its officials and personnel.