Expert Speak | 26 May, 2026

The U.S.-Iran Ceasefire Illusion: Energy Shortages Far from Over

The following excerpt is from Chapter 3 — Shifting Sands: A Middle East in Conflict and Transition.

The Strait of Hormuz crisis has sent ripples across global energy and commodity markets. Political posturing, primarily United States (US) President Donald Trump’s grand proclamations, have driven sharp swings in oil prices—pushing Futures Brent crude to as high as US$126[1] down to US$95 following the ceasefire announcement on 7 April 2026.[2] Brent crude futures surged by more than 60 percent between late February and mid-March.[3] The tanker traffic through the Strait of Hormuz reduced by as much as 95 percent compared to pre-crisis levels,[4] becoming almost negligible at the time of writing and operating on an ad-hoc basis. Conflicting announcements from Washington and Tehran regarding the peace deal continue to leave the passageway dangerously contested and the markets increasingly wary.

Though global markets are desperately trying to decouple from the developments in the Middle East, their efforts are unlikely to hold. The structural consequences of the disruptions will far outlast the conflict itself. While diplomatic posturing can temporarily calm markets, it will not be able to repair damaged infrastructure, restore lost capacity, or eliminate the irreversible capital stock destruction and the endogenous risk premium in shipping insurance. The question is no longer whether the supply will return, but rather how economies will adapt to a period of constrained and uncertain availability.

Most Significant Energy Shock in History

The International Energy Agency has described the Hormuz conflict as the most significant oil shock in history, with damage to almost 80 energy facilities in the Middle East[5] amounting to at least US$25 billion,[6] and loss of more than 13 million barrels per day of exports.[7] Almost 35 percent of global crude oil and products, and 20 percent of natural gas supplies[8] pass through the Strait of Hormuz. Unlike the previous crises—the oil shocks of 1973 and 1979, or the loss of Russian gas following Moscow’s invasion of Ukraine in 2022—this episode extends beyond oil and gas. It represents multi-commodity shocks—on fertilisers, petrochemicals, and refined products— in turn triggering cascading effects across global supply chains.

Yet, despite the severity of the crisis, the price shocks have not been as pronounced as anticipated. This is due to an oversupply of pre-existing inventory at sea, strategic reserve release, overseas Gulf storage, external alternative pipelines available to Saudi Arabia and the United Arab Emirates, and anticipatory stockpiling by energy importing Asian countries. However, as reserves deplete and logistical constraints tighten, markets will be compelled to account for the true scale of the disruptions. The current short-term cushioning will therefore prove to be temporary, exposing the underlying long-term constraints yet to entirely unfold.

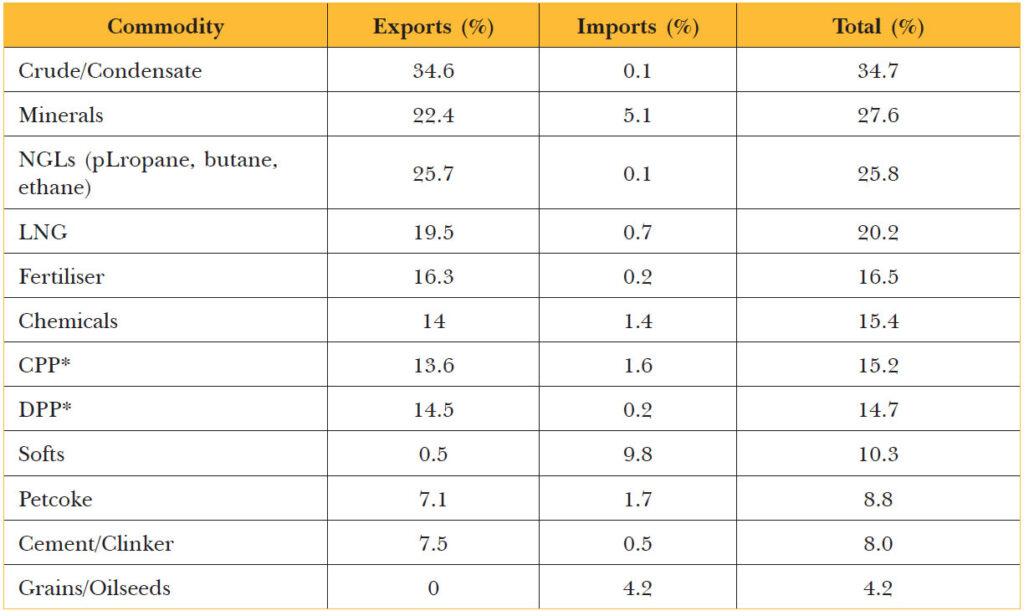

Table 1: Share of Global Seaborne Commodity Flows Transiting the Strait of Hormuz in 2024 (Imports + Exports)

Source: Kpler[9]

Note: CPP (clean petroleum products such as naphtha, gasoline, jet fuel (A1), kerosene, and gas oil); DPP (dirty petroleum products such as crude oil, fuel oil, heavy fuel oil, and dirty condensate)

Triple Whammy: Logistical Disruptions, Storage Constraints, and Infrastructure Damage

Before the crisis, approximately 20 million barrels per day (mbpd) of crude oil and product exports would pass through the Hormuz Strait—primarily from Saudi Arabia, the UAE, Kuwait, Iraq, and Iran. The alternative routes bypassing the Hormuz have managed to offset some of the supplies but cannot compensate for complete loss of maritime flows. Saudi Arabia’s 1,200 km long East–West Crude pipeline from Abqaiq to Yanbu in the Red Sea has an export capacity of around 5 mbpd,[10] with a parallel Petroline for natural gas liquids (NGLs). Even though overall Saudi crude exports fell 25 percent in March 2026 from the same time last year, the higher prices caused the value of those exports to balloon by roughly US$558 million,[11] partially substituting for lost Iraqi and Gulf supplies. This divergence reflects a classic terms of-trade gain for Riyadh but a welfare loss for the global economy. Essentially it is a transfer of wealth from consumers to producers that acts as a deadweight drag on global gross domestic product (GDP).

The UAE has also witnessed a decline of almost 30 percent in exports from last year. However, the 380-km Abu Dhabi Crude Oil Pipeline (ADCOP), running from Habshan to the Fujairah port and bypassing the Strait of Hormuz, offers a relatively secure alternative to move between 1.5–1.8 mbpd (roughly half of UAE’s total daily oil export capacity) to the Indian Ocean[12], which has helped keep revenues around the same range.

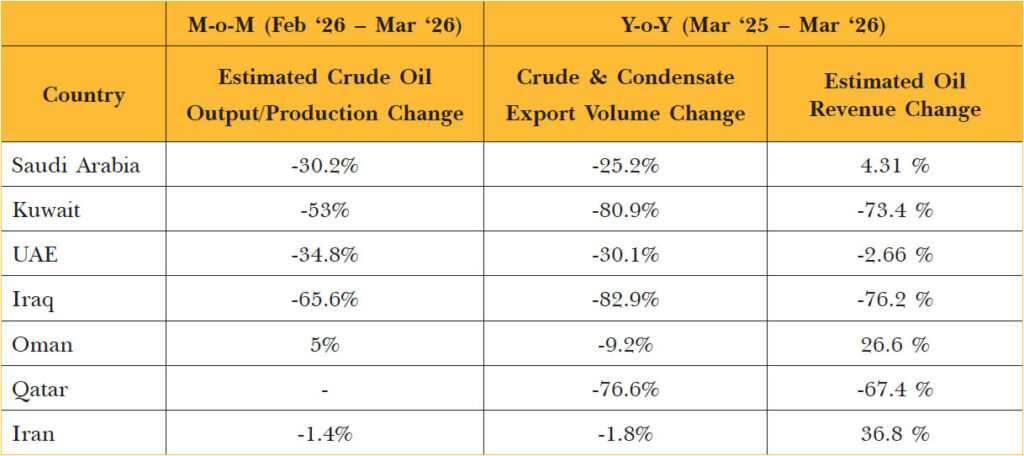

Table 2: Crude Oil Production, Export Volume, and Revenue Change for the Arabian Gulf Countries

Sources: Reuters[13] & IEA[14]

In contrast, Iraq has recorded the steepest supply declines, suffering significant losses in export volumes and revenues. Pre-crisis production of 4.25 mbpd has plummeted to 875,000 barrels per day (bpd), while exports have declined by 83 percent in March 2026 compared to the same period last year, with limited diversion options and a constrained pipeline capacity of 200,000 bpd via the Kirkuk–Ceyhan northern pipeline between Iraq and Turkey.[15] Kuwait has also faced a similarly devastating outcome with no viable alternative route and mounting storage constraints. Without continuous shipments, production must halt once storage is exhausted forcing facility shut downs. Producers can, in theory, utilise floating storage, but in practice credit constraints and warrisk insurance costs prove onerous, reinforcing the financial dimension of supply disruptions.

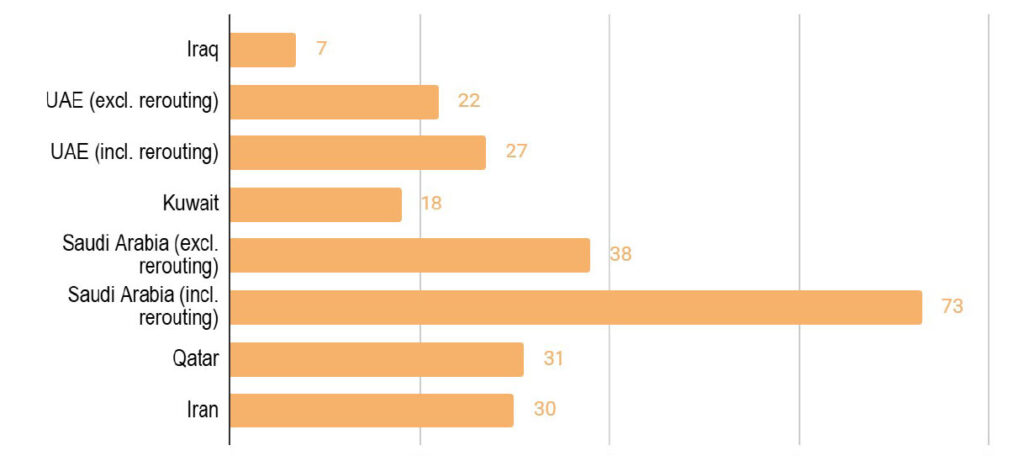

Figure 1: Estimated Days Until Storage Tanks in the Gulf Countries Fill Up, Forcing Oil Field Shut-Ins

Note: Measured from Day 1 of conflict (28 February 2026)

Source: Reuters[16]

Natural gas supplies from the region, primarily from Qatar (as much as 93 percent) and the UAE (7 percent),[17] have been significantly curtailed. Following sustained kinetic attacks, the Ras Laffan facility in Qatar with normal capacity of 77 million tonnes per annum (mtpa)[18] declared force majeure (emergency halt) on some liquified natural gas (LNG) contracts for up to five years.[19] This has eliminated 17 percent of Qatar’s LNG export capacity, with losses of 12.8 mtpa of LNG for three to five years until repairs are actualised.[20] Beyond LNG, Qatar’s exports of condensate will drop by around 24 percent, while liquefied petroleum gas (LPG) will fall 13 percent, helium output will fall 14 percent, and naphtha and sulphur will both drop by 6 percent.[21] For the UAE, disruptions to shipping through the Strait of Hormuz has led to significant declines[22] in output at the country’s sole LNG plant on Das Island, effectively halting most of its 5.8 mtpa of production capacity.[23] In parallel, damage to the UAE’s gas infrastructure, particularly the Habshan facility, poses significant risk to the country’s domestic gas supply[24].

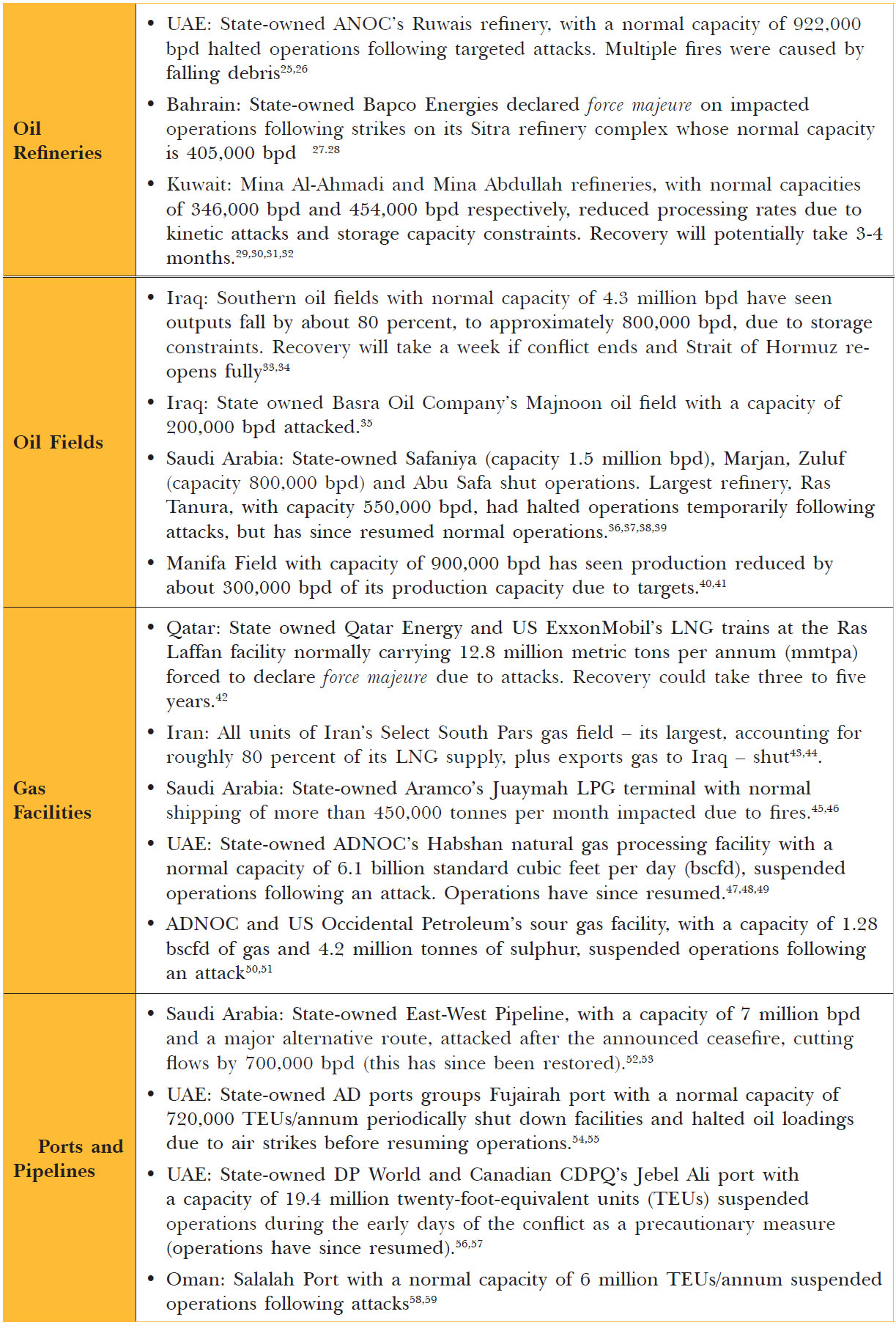

Besides the logistical disruption and storage constraints, damage to oil fields and refineries, ports and pipelines, and gas facilities, will take many months – if not years in some cases – to repair, reopen and resume, further disrupting and prolonging supply disruptions in global markets.

Table 3: Key Disruptions to Arabian Gulf Oil and Gas Infrastructure (28 Feb – 15 Apr 2026)

Source: Authors’ own, using various open sources.

Energy Shortages Far from Over

Energy shortages are unlikely to ease, even in the aftermath of a ceasefire or any semblance of normalisation. Alternative routes from Saudi, the UAE and Oman offer limited relief—these pipelines were designed to complement and not substitute maritime flows through the Strait. Their capacity falls way short of the scope of the disruption. At the same time, repairing damaged infrastructure, rebuilding strategic petroleum reserves, and regular stockpiling by importing countries, will keep prices elevated and unlikely to swiftly retreat to the pre-war USD 60-70 range.

Compounding this challenge are shipping and insurance constraints. Maritime insurers are repricing or suspending war risk coverage— currently 329 vessels are stranded in the Arabian Gulf requiring roughly US$352 billion in insurance coverage that private markets are no longer providing.[60] Traders price risk and not just physical supply, and insurance premiums will continue to factor in geopolitical stressors long after the hostilities are over. To illustrate, although the Red Sea Houthi attacks declined in 2025 relative to 2023-24 levels, transit volumes through the Bab-al-Mandab Strait remained 65-percent below pre-conflict baselines as of June 2025.[61] Even if physical risk subsides, the perceived risk of potential future disruptions may continue to affect pricing and shipping volumes through the Strait of Hormuz. Investments will remain highly sensitive and contingent on long term maritime stability. The role of expectations, speculative behaviour, and futures markets in shaping price trajectories is central to risk pricing. The inability of private markets to clear this risk is a classic market failure which will potentially need state intervention in the form of government-backed war-risk insurance mechanisms to restore both trust and trade flows.

Energy markets are inherently adaptive and nonlinear. Market adjustments are not purely supply driven—the marginal cost of storage and demand destruction in price-sensitive developing economies will act as a market clearing mechanism. At the same time, substitution effects and accelerated supply responses outside the Gulf will gather pace. Renewed oil and gas exploration in new geographies such as the North Sea, Africa, the Eastern Mediterranean, and the Arctic, could become economically feasible in the wake of recent geopolitical realities. These dynamics will act as important countervailing forces in restoring equilibrium at relatively lower volumes. Highers prices with slower growth will heighten stagflationary pressures in importing countries.

The crisis is also accelerating a broader structural transition. In the coming years, countries will increasingly prioritise diversification—both in terms of supply partnerships and transport routes. At the same time, higher fossil fuel prices are improving the viability of alternative technologies, including nuclear energy, hydrogen and solar plus storage. These shifts, however, involve significant fiscal, geopolitical and climate trade-offs, and their pace and direction will vary considerably across countries. The UAE’s recent departure from the Organization of the Petroleum Exporting Countries Plus (OPEC+) alliance is also notable, as it could introduce greater supply flexibility while simultaneously contributing to heightened price volatility and weaker coordination among major producers.

It is clear that the energy security calculus for both energy exporting and importing countries is fundamentally shifting, emphasising resilience, system redundancy, and the endogenous role of risk in price formation. Whether this evolves into a permanent structural transformation or remains a cyclical adjustment will depend on the duration of the conflict, the extent of future disruptions, and persistence of current risk perceptions and policy responses.

Mannat Jaspal is Director and Fellow, Climate and Energy, ORF Middle East.

Reem Sagahyroon is Research Assistant, Climate and Energy, ORF Middle East.

[1] Nicole Jao, “Oil Retreats After Hitting Four-year High on Concern of US-Iran War Escalation,” Reuters, April 30, 2026, https://www.reuters.com/business/energy/oilretreats- after-hitting-four-year-high-concern-us-iranwar- escalation-2026-04-30/.

[2] “ICE Brent Crude Energy Future c1,” Reuters, May 6, 2026, https://www.reuters.com/markets/quote/LCOc1/.

[3] IEA, “Key Facts on the Strait of Hormuz, Oil and Gas Markets, and the IEA’s Response,” https://www.iea.org/ topics/the-middle-east-and-global-energy-markets.

[4] Matt Strahan and Daniel Murphy, “How War in the Middle East is Turning Governments Into Insurers of Last Resort,” World Economic Forum, April, 2026, https://www.weforum.org/stories/2026/04/how-middleeast- war-turning-governments-into-insurers-last-resort/.

[5] “How the War in the Middle East is Impacting Global Energy Systems,” MIT Energy Initiative, April 30, 2026, https://energy.mit.edu/news/how-the-war-in-the-middleeast- is-impacting-global-energy-systems/.

[6] Anushree Ashish Mukherjee, Vallari Srivastava and Pranav Mathur, “Services Firms Feel the Squeeze as Oil Rally from Iran War Fails to Spur Drilling,” Reuters, March 27, 2026, https://www.reuters.com/business/ energy/services-firms-feel-squeeze-oil-rally-iran-war-failsspur- drilling-2026-03-27/.

[7] IEA, Oil Market Report, April 2026, https://iea.blob. core.windows.net/assets/515f3128-df1a-4d6c-beb4- fd91d2434bef/-14APR2026_OilMarketReport_Free_ version1.pdf.

[8] IEA, “Strait of Hormuz Factsheet,” https://www.iea.org/ about/oil-security-and-emergency-response/strait-ofhormuz.

[9] Florian Grünberger, “Strait of Hormuz – What’s At Stake?,” Kpler, June 2025, https://www.kpler.com/blog/ strait-of-hormuz—whats-at-stake

[10] IEA, “Strait of Hormuz Factsheet”.

[11] Ahmad Ghaddar and Yousef Saba, “Hormuz Closure Divides the Fortunes of Middle Eastern Oil States,” Reuters, April 6, 2026, https://www.reuters.com/business/ energy/hormuz-closure-divides-fortunes-middle-easternoil- states-2026-04-06/.

[12] Somshankar Bandyopadhyay, “Iran-Israel War: UAE Oil Pipeline Offers Safe Alternative in Case of Hormuz Closure,” Khaleej Times, June 23, 2025, https://www. khaleejtimes.com/business/iran-israel-war-uae-oilpipeline- offers-safe-alternative-in-case-of-hormuzclosure.

[13] Ghaddar and Saba, “Hormuz Closure Divides the Fortunes of Middle Eastern Oil States”.

[14] International Energy Agency, Oil Market Report, 2026, https://iea.blob.core.windows.net/assets/515f3128- df1a-4d6c-beb4-fd91d2434bef/-14APR2026_ OilMarketReport_Free_version1.pdf.

[15] Victoria Grabenwöger, “Resumption of Iraqi flows via Strait of Hormuz?,” Kpler, April 2026, https://www.kpler. com/blog/resumption-of-iraqi-flows-via-strait-of-hormuz.

[16] Ahmad Ghaddar, Yousef Saba, and Alex Lawler, “After Iraq, Kuwait and UAE May be Next to Cut Oil Output on Iran Crisis, Analysts Say,” Reuters, March 5, 2026, https:// www.reuters.com/business/energy/after-iraq-kuwaituae- may-be-next-cut-oil-output-iran-crisis-analystssay- 2026-03-05/.

[17] Grünberger, “Strait of Hormuz – What’s at Stake?”.

[18] Marwa Rashad, “Qatar’s Role in the Global Gas Market,” Reuters, March 2, 2026, https://www.reuters.com/business/ energy/qatars-role-global-gas-market-2026-03-19/.

[19] Emese Fabian, “QatarEnergy Declares Force Majeure For Up to Five Years,” Ceenergy News, March 25, 2026, https://ceenergynews.com/oil-gas/qatarenergyforce- majeure/#:~:text=HomeOil%20&%20 GasQatarEnergy%20declares,long%2Dterm%20 LNG%20contracts.%E2%80%9D.

[20] Maha El Dahan, Andrew Mills and Yousef Saba, “Exclusive: Iran Attacks Wipe Out 17% of Qatar’s LNG Capacity for Up to Five Years, QatarEnergy CEO Says,” Reuters, March 19, 2026, https://www.reuters.com/ business/energy/iran-attack-damage-wipes-out-17-qatarslng- capacity-three-five-years-qatarenergy-2026-03-19/.

[21] Dahan, Mills and Saba, “Exclusive: Iran Attacks Wipe Out 17% of Qatar’s LNG Capacity for Up to Five Years, QatarEnergy CEO Says”.

[22] Anthony Di Paola, “UAE Restarts Main Gas Supply Plant While Idling Most LNG Output,” Bloomberg, March 23, 2026, https://www.bloomberg.com/news/ articles/2026-03-23/uae-restarts-main-gas-supply-plantwhile- idling-most-lng-output.

[23] Laura Page, “Middle East Conflict – Gas Market Implications: A Continuing Assessment,” Kpler, March 2026, https://www.kpler.com/blog/middle-east-conflict— gas-market-implications-a-continuing-assessment.

[24] Wood Mackenzie, “Middle East Oil and Gas Recovery Faces Months-Long Process Despite Ceasefire,” April 2026, https://www.woodmac.com/press-releases/middleeast- oil-and-gas-recovery-faces-months-long-processdespite- ceasefire/.

[25] Salma El Wardany and Anthony Di Paola, “Biggest UAE Refinery Halts as Precaution After Drone Attack,” Bloomberg, March 10, 2026, https://www.bloomberg.com/ news/articles/2026-03-10/uae-says-drone-attack-causesfire- in-zone-that-houses-refinery.

[26] Yousef Saba and Ahmad Ghaddar, “UAE oil giant ADNOC Shuts Ruwais Refinery After Drone strike, source says,” Reuters, March 10, 2026, https://www.reuters.com/world/ middle-east/fire-hits-site-housing-abu-dhabi-national-oilcompany- operations-after-drone-2026-03-10/.

[27] Dylan Griffiths and Carlos Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War,” Bloomberg, April 11, 2026, https://www.bloomberg.com/ news/articles/2026-03-25/here-s-a-list-of-gulf-energyinfrastructure- damaged-in-iran-war.

[28] Rithika Krishna and Bachar Halabi, “Bahrain’s Bapco Issues Force Majeure After Refinery Hit,” Argus, March 9, 2026, https://www.argusmedia.com/en/news-and-insights/ latest-market-news/2798255-bahrain-s-bapco-issuesforce- majeure-after-refinery-hit.

[29] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[30] Kuwait National Petroleum Company, “Overview,” https://www.knpc.com/en/about-us/who-we-are.

[31] “Around 1.9 Million bpd of Gulf Oil Refining Capacity Shut Due to Iran War, IIR Says,” Reuters, March 10, 2026, https://www.reuters.com/business/energy/around-19- million-bpd-oil-refining-capacity-shut-due-iran-war-gulfiir- says-2026-03-10/.

[32] “How the US-Israeli War with Iran is Disrupting Oil and Gas,” Reuters, April 7, 2026, https://www.reuters.com/ business/energy/us-israeli-war-iran-causes-major-oil-gasdisruptions- 2026-04-07/.

[33] “Exclusive: Iraq Oil Output Further Plunges as Storage Fills, Hormuz Exports Blocked by Conflict,” Reuters, March 25, 2026, https://www.reuters.com/business/ energy/iraq-oil-output-further-plunges-storage-fillshormuz- exports-blocked-by-conflict-2026-03-25/.

[34] Aref Mohammed, “Exclusive: Iraq Could Restore Oil Exports to Pre-war Level Within a Week If Hormuz Reopens, Basra Oil Chief Says,” Reuters, April 7, 2026, https://www.reuters.com/business/energy/iraq-couldrestore- oil-exports-pre-war-level-within-week-if-hormuzreopens- basra-2026-04-06/.

[35] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[36] Bachar Halabi, Nader Itayim and Aydin Calik, “Hormuz Halt Forces Opec+ Producers to Curb Crude Output,” Argus, March 9, 2026, https://www.argusmedia.com/en/ news-and-insights/latest-market-news/2798472-hormuzhalt- forces-opec-producers-to-curb-crude-output.

[37] “Safaniya Oil Field,” Saudipedia, October 10, 2025, https://saudipedia.com/en/safaniya-oil-field.

[38] “Aramco’s Giant Zuluf Oilfield Expansion: 5 Facts you Need to Know,” Oil&Gas Middle East, November 14, 2022, https://www.oilandgasmiddleeast.com/explorationproduction/ aramcos-giant-zuluf-oilfield-expansion-5- facts-you-need-to-know.

[39] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[40] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[41] “Saudi Aramco’s Manifa Oilfield Production Hit by Technical Issue: Report,” Reuters, July 11, 2017, https:// www.reuters.com/article/world/saudi-aramcos-manifaoilfield- production-hit-by-technical-issue-reportidUSKBN19W1R3/.

[42] Dahan, Mills and Saba, “Exclusive: Iran Attacks Wipe Out 17% of Qatar’s LNG Capacity for Up to Five Years, QatarEnergy CEO Says”.

[43] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[44] Sarah Shamim, “Why are Iran’s South Pars Gasfield, Qatar’s Ras Laffan, So Significant?,” Al Jazeera, March 19, 2026, https://www.aljazeera.com/economy/2026/3/19/ why-are-irans-south-pars-gasfield-qatars-ras-laffan-sosignificant.

[45] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[46] Shariq Khan and Dmitry Zhdannikov, “Aramco Cancels Juaymah LPG Deliveries through March for Repairs, Traders Say,” Reuters, February 26, 2026, https:// www.reuters.com/business/energy/aramco-cancelsjuaymah- lpg-deliveries-through-march-repairs-traderssay- 2026-02-26/.

[47] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[48] ADNOC Gas, “Gas Processing,” https://adnocgas.ae/en/ our-operations/gas-processing.

[49] Fareed Rahman, “Adnoc Gas Operations Continuing Safely After Debris Falls Near Facilities,” The National, March 23, 2026, https://www.thenationalnews.com/ business/energy/2026/03/23/adnoc-gas-operationscontinuing- safely-after-debris-falls-near-facilities/.

[50] Anthony Di Paola, “UAE Gas Plant, Kuwait Oil Refinery Hit in Latest Iran Attacks,” Bloomberg, April 3, 2026, https://www.bloomberg.com/news/articles/2026-04-03/ abu-dhabi-halts-operations-at-main-gas-facility-afterattack.

[51] ADNOC, “ADNOC Sour Gas,” https://www.adnoc.ae/en/ adnoc-sour-gas.

[52] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[53] Lekshmy Pavithran and Christian Borbon, “Lekshmy Pavithran, Assistant Online Editor and Christian Borbon,” Gulf News, April 12, 2026, https://gulfnews.com/ business/energy/saudi-arabia-restores-key-oil-facilitiesafter- attacks-stabilises-global-supply-1.500504143.

[54] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[55] Port of Fujairah, “Our Story,” https://fujairahport.ae/ about-us/port-of-fujairah-overview/.

[56] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[57] “Dubai’s DP World Says Operations at UAE’s Jebel Ali Port Resumed, Notice Shows,” Reuters, March 2, 2026, https://www.reuters.com/world/middle-east/dubais-dpworld- says-operations-uaes-jebel-ali-port-resumednotice- shows-2026-03-02/.

[58] Griffiths and Caminada, “Here’s a List of Gulf Energy Infrastructure Damaged in Iran War”.

[59] Ministry of Transport, Communications and Information Technology, “Ports,” https://mtcit.gov.om/sectors/ports/ ports-harbour.

[60] Myles McCormick, Jamie Smyth, and Lee Harris in London, “Industry Doubts Trump Plan to Insure Gulf Oil Tankers as Iran War Halts Transit,” Financial Times, March 5, 2026, https://www.ft.com/content/6ddeb488- 0d6f-4b6a-b419-2a2ba7437a25?syn-25a6b1a6=1.

[61] Luca Nevola and Jalale Getachew Birru, Regional Power Struggles Fuel Simmering Tensions Across the Red Sea, Armed Conflict Location and Event Dataset, 2025, https:// acleddata.com/report/regional-power-struggles-fuelsimmering- tensions-across-red-sea.