Expert Speak | 29 May, 2026

Canada Strong Fund: A Platform for Gulf Strategic Investment

Spotlight:

- Canada’s proposed sovereign wealth fund departs from traditional models and will require steady market returns, political independence, and clear value creation to ensure long-term success.

- Canada and its GCC counterparts share strong bilateral ties that are expected to deepen further through new and ongoing engagements.

- Clear avenues exist for Canada-GCC collaborations via co-investments with the CSF, particularly as Gulf States pursue overlapping priorities in sectors including critical minerals, conventional and clean energy, and food security.

Canada’s recently announced sovereign wealth fund (SWF) – Canada Strong Fund (CSF) – comes at a time of growing economic uncertainty and reflects a broader push to build what Prime Minister Mark Carney described as a ‘stronger, more resilient, and more independent Canadian economy.’ Rising trade tensions and tariff threats from its long-standing partner, the United States (US), have intensified concerns around economic resilience and strategic autonomy. At the same time, Canada has long faced a challenge of ‘infrastructure in waiting,’ driven by factors including insufficient private-sector capital deployment, supply chain disruptions, and regulatory bottlenecks – including ESG reporting.

Against this backdrop, the CSF has been mandated to generate market-rate returns for Canadians by co-investing alongside partner investors in domestic projects across priority sectors. Despite initial controversy surrounding the development, if successful it could create a new pathway for Canada to deepen partnerships with the Gulf countries. This comes at a time when both Canada and Gulf states are seeking greater economic resilience and diversification pathways.

A Different Model of Sovereign Capital

Traditionally, SWFs follow two broad characteristics: first, they are financed through domestic capital surpluses from balance of payments or commodity exports; and second, they invest through diversified portfolios spanning both domestic and foreign markets. The CSF diverges from both patterns. It will initially be financed through a government allocation of CAD 25 billion over three years, raised through ‘borrowing’, an approach that has stirred very mixed reactions among Canadian financial and political experts. This concern stems largely from Canada’s persistent fiscal deficits since 2015 – at approximately CAD 67 billion in FY25-26. Additionally, the CSF is exclusively focused on domestic investments. However, this approach is not entirely unprecedented. Academic literature identifies varying SWF objectives, one of which includes supporting domestic economies by serving as government-backed venture capital funds – where the CSF seems to fall – or as a stabilisation fund to compensate for shortfalls in the government budget.

At the same time, the CSF must present value addition beyond existing federal investment vehicles such as the Canada Infrastructure Bank (CIB) and Canada Growth Fund (CGF).

Given that the CSF is expected to operate domestically, its mandate will have to avoid creating tensions between commercially driven investment strategies and broader government policy priorities to prevent inefficiencies and politically driven capital allocation. At the same time, the CSF must present value addition beyond existing federal investment vehicles such as the Canada Infrastructure Bank (CIB) and Canada Growth Fund (CGF). This could include, unlocking capital flows beyond the capacity of current institutions or strengthening economic resilience in ways that would otherwise be difficult to achieve. If unable to, it risks increasing institutional complexities rather than achieving the desired result of building Canada’s wealth and advancing priority sector projects.

Canada-GCC Growing Relations

Canada already maintains deep economic relationships with the Gulf countries and is only continuing to expand, reflected in at least nine visits by Prime Minister Mark Carney’s ministers and officials to Gulf nations since October 2025. This growing GCC-Canada relationship creates potential avenues for collaboration between the CSF and Gulf financial entities – including SWFs – in sectors where Canada maintains competitive advantages. Such collaborations align well with trends in the Gulf, where SWFs are increasingly partnering with private financial institutions and other state-backed investors through joint ventures and sovereign-private partnerships (SPPs). These models support multiple objectives, including costs saving, facilitating knowledge sharing, and diversifying investment portfolios.

This growing GCC-Canada relationship creates potential avenues for collaboration between the CSF and Gulf financial entities – including SWFs – in sectors where Canada maintains competitive advantages.

Reciprocally, Canada should continue to expand investment flows into the GCC states. Established Canadian pension-backed funds, private capital managers, and venture capital firms have expertise in several sectors that are increasingly prioritised in the Gulf. These include industrial decarbonisation, digital infrastructure, and climate technology. These entities can cooperate with Gulf financial institutions through joint ventures, equity investments, and co-investment funds. The United Arab Emirates (UAE) also offers a highly incentivised and flexible regulatory environment through its financial free zones – the Dubai International Financial Centre and the Abu Dhabi Global Market – providing Canadian firms with access to Gulf capital and opportunities to form strategic partnerships with regional actors.

Table 1: Examples of Ongoing Canada-GCC Bilateral Engagements

| Canada-UAE | ● Canada-UAE Foreign Investment Promotion and Protection Agreement (FIPA) signed in November 2025

● UAE has committed to invest approximately US$50 billion in Canada ● Canadian direct investment in the UAE reached US$242 million in 2024 |

| Canada-Saudi Arabia | ● Both countries have agreed to begin negotiations toward a bilateral FIPA

● Agreed to reactivate the Joint Economic Commission (JEC), a ‘treaty-based mechanism to promote trade and investment initiatives of mutual benefit’ |

| Canada-Qatar | ● Prime Minister of Canada and the Amir of Qatar issued a joint statement committing Qatar to strategic investments in large-scale Canadian infrastructure projects

● Canada and Qatar plan to finalise a Foreign Investment Promotion and Protection Agreement (FIPA) by this year ● Agreed to expand cooperation on trade and investment through a Joint Canada-Qatar Commission on Economic, Commercial, and Technical Cooperation |

| Canada-Kuwait | ● Signed an MoU in 2022 committing both countries to deeper cooperation across areas of mutual interest |

| Canada-Oman | ● Agreed to advance bilateral engagement in trade, energy, critical minerals, higher education, tourism and people-to-people ties

● Canadian investments maintain a solid presence in the Omani market, with approximately 280 Canadian companies operating with an estimated total capital of around OMR37 million ● Bilateral trade reached CAD $222 million (OMR 62m, USD 160m) in 2025 and highlighted the strong potential for further economic growth |

Source – Author’s Own

Strategic Sectors for CSF-GCC Investment Cooperation

Although the CSF will target a range of sectors considered strategically important to Canada, several areas also align closely with Gulf priorities, creating opportunities for mutual benefit.

Critical Minerals

Gulf investors are more actively prioritising long-term access to critical minerals as part of broader efforts to strengthen supply-chain resilience and secure inputs necessary for the global energy transition. These minerals include lithium, nickel, cobalt, graphite, and potash, all of which are essential for batteries, renewable energy technologies, and electrification. To illustrate this, in line with Saudi Arabia’s Vision 2030 strategy, a joint venture – Manara Minerals -was established between Public Investment Fund (PIF), the country’s SWF, and Ma’aden specifically to pursue international critical mineral investments.

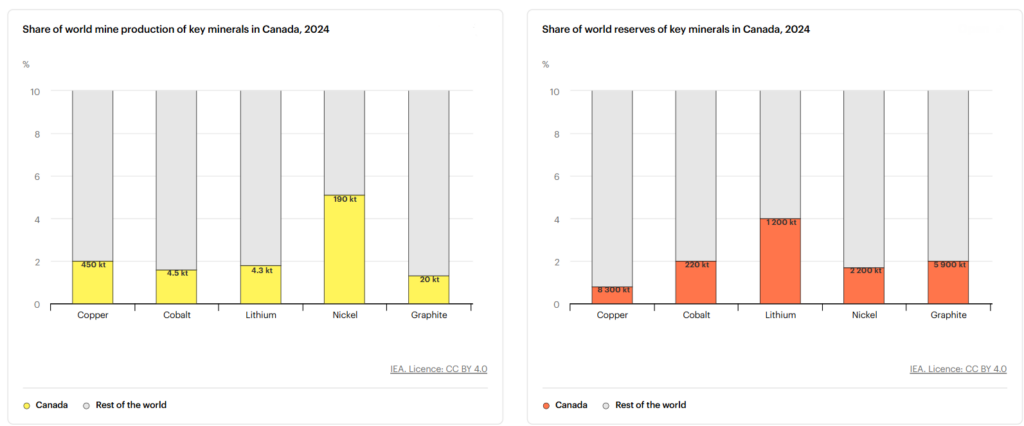

Canada is particularly well positioned in this space. According to the International Energy Agency, the country is expected to emerge as a major global supplier of key CMs such as nickel and lithium, while also possessing significant capacity to expand production further. The nation additionally maintains strengths across midstream and downstream components of the critical minerals value chain, creating a broad set of avenues for Gulf investors seeking both resource access and processing capabilities.

Source – IEA

Earlier in 2026, Canada and Saudi Arabia signed a Memorandum of Understanding (MoU) focused on cooperation in mineral resources, aimed at promoting trade and investment across critical mineral value chains. More substantially, the UAE and Canada are reportedly finalising an agreement exceeding CAD 1 billion to expand domestic critical mineral processing capacity within Canada.

Conventional and Clean Energy

With Carney in office, Canada’s oil and gas sector has seen renewed support and a government pledge to support industry growth. Implemented industrial carbon pricing has shown limited evidence of undermining the sector’s competitiveness. Oil production grew by 20 percent between 2024 and 2025. In parallel, Canada stands as the world’s fifth-largest natural gas producer, with expanding LNG export capacity expected to boost domestic production. Coupled with the ongoing tensions in the Middle East, Canada’s oil and gas sector is becoming an increasingly attractive site for investments. This aligns well with Gulf states’ continued investments in international hydrocarbon assets. Companies such as Saudi’s Aramco and UAE’s ADNOC have increased investments in US LNG projects in recent years, while QatarEnergy has acquired stakes in Egypt, Namibia, and South Africa.

Coupled with the ongoing tensions in the Middle East, Canada’s oil and gas sector is becoming an increasingly attractive site for investments.

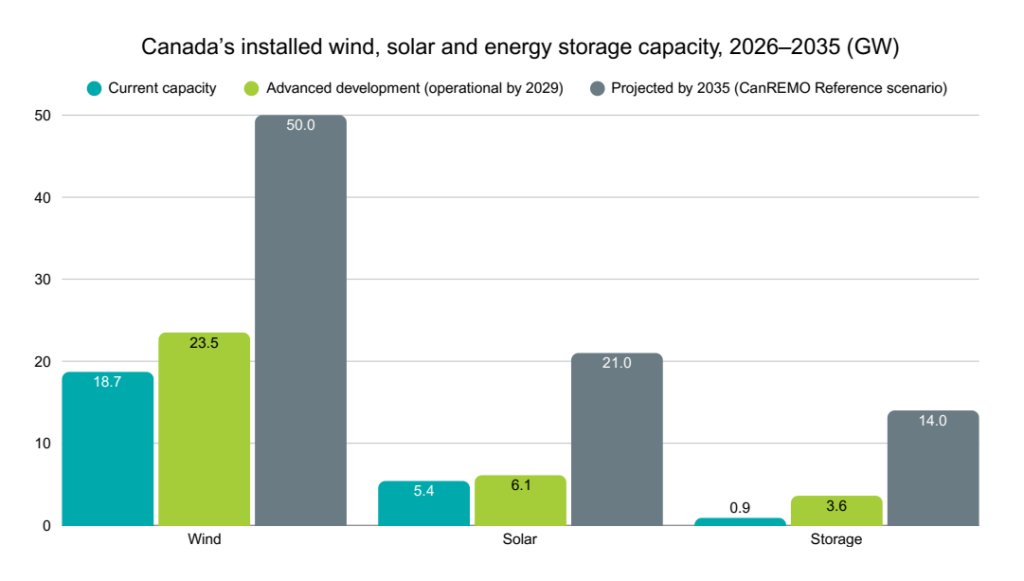

Beyond conventional energy, there has been a growing push for SWFs to play a more active role in financing the global energy transition. In 2023, nearly half of global SWF allocations toward green assets originated from GCC-based SWF, where renewable energy was the most attractive investment segment. The Gulf countries have made their pursuit of economic and energy diversification clear through national strategies such as the Oman Vision 2040. On this note, a report by the Canadian Renewable Energy Association identifies Canada as a highly attractive destination for renewable energy investment over the next decade, driven by its vast resource base, relatively stable policy environment, and rising electricity demand.

Source – Canadian Renewable Association

Although Gulf investments in Canada’s renewable energy sector remains relatively limited to date, the scale of projected growth in Canada’s clean energy sector presents considerable prospects for Gulf SWFs and financial institutions to invest alongside the CSF and other Canadian institutions such as the CIB – whose main role is to accelerate low carbon transitions by de-risking and attracting private capital into large-scale renewable energy projects.

In addition, Canada is emerging as a leader in nuclear energy, with 17 nuclear power reactors in operation and strong ambitions to advance small modular reactor (SMR) development. This aligns closely with the UAE’s position as the Gulf region’s sole nuclear power operator with a potential interest in SMR-powered data centres, creating opportunities for the CSF and Gulf financial entities to collaborate on bilateral investments within the nuclear energy sector.

Agri-Food

Gulf countries – which rely on imports for nearly 90 percent of their food needs – are increasingly prioritising more diversified and resilient food supply chains, particularly following disruptions such as COVID-19 pandemic and the current US-Iran conflict. Consequently, overseas agricultural investments remain central to Gulf food security strategies. For example, Saudi Arabia and UAE companies have expanded their agricultural footprint through acquisitions of farmland and agribusiness across countries such as Ethiopia and Chile.

Although geographic distance increases transportation costs, growing concerns over supply chain resilience and redundancy could support the case for co-investments in this sector.

Canada hosts extensive arable land, a reputation for high-quality agri-food products, and relatively sustainable agricultural production systems. However, agriculture accounts for only 2 percent of Canada’s government-backed growth, venture, and infrastructure funding, indicating meaningful room for expansion. The Canadian government has therefore listed agricultural projects as one of the sectors of interest for the developing CSF, creating openings for co-investment with Gulf SWFs and financial entities.

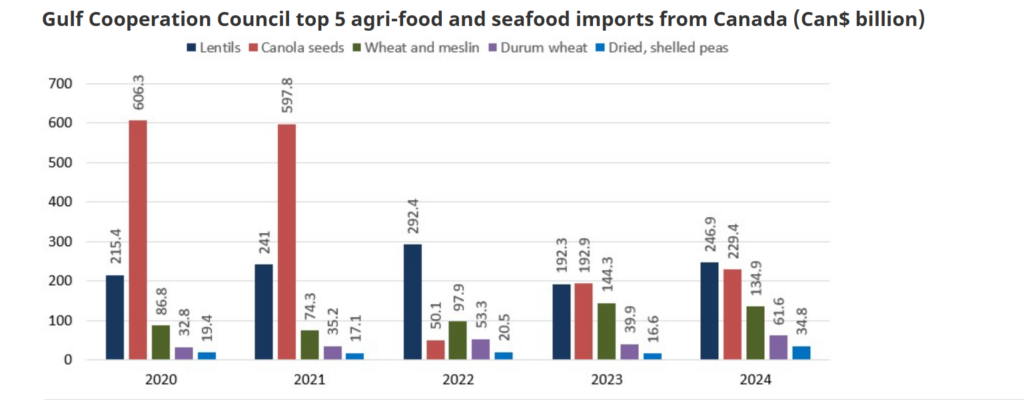

As Canada looks to widen its trade and investment partnerships beyond the US, GCC countries could play a larger role in expanding investments across Canada’s agri-food sector. Gulf states currently maintain strong food trade ties with Canada (graph), and the Canada-UAE Business Council includes a dedicated working group focused on agriculture and food security. Although geographic distance increases transportation costs, growing concerns over supply chain resilience and redundancy could support the case for co-investments in this sector.

Source – Government of Canada

There are select risks that co-investors need to be mindful of navigating when operating alongside the CSF. Given the fund is initially operating off borrowings, generating significant returns on its investments is critical to reduce the risk of political or financial pressures driving shifts in investment strategies or asset liquidation over time, potentially creating misalignments with Gulf investors that prioritise long-term stability. To hedge risks beyond co-investment structures, the CSF could diversify into foreign assets – including opportunities in the Gulf – while still maintaining a primarily domestic investment focus. Given the current geopolitical environment, the Gulf SWFs may choose to reroute some investments domestically. Nevertheless, Canada’s expanding regional engagement and diplomatic support for partners in the GCC during recent crises could encourage institutional partnerships that position the nation favorably for long-term investment diversification.

Reem Sagahyroon is a Research Assistant, Climate and Energy, ORF Middle East.