Occasional Paper | 17 July, 2026 Download Report (PDF)

ASEAN’s Energy Vulnerability and the Impact of the Hormuz Crisis

The closure of the Strait of Hormuz exposed Southeast Asia’s structural energy vulnerabilities. This paper assesses the impact of the ongoing disruption across all 11 Association of Southeast Asian Nations (ASEAN) member states, examining oil supply exposure and refinery substitution capacity, gas and liquefied natural gas (LNG) dependence, and the state of renewable energy transition. It organises the member states into four clusters defined by production capacity, refining sophistication, and import structure, to map a wide spectrum of vulnerability. The fragility of the current ceasefire and the partial nature of the Strait’s reopening mean that the structural vulnerabilities remain live rather than resolved. The paper concludes that while the crisis has generated institutional momentum towards collective energy security mechanisms, the distance between political commitment and structural change remains long. The broader question is whether ASEAN will use the window to build the necessary grid architecture, strategic reserve depth, and transition financing.

Attribution: Parul Bakshi, “ASEAN’s Energy Vulnerability and the Impact of the Hormuz Crisis,” ORF Occasional Paper No. 563, Observer Research Foundation, July 2026.

Introduction

On 28 February 2026, the United States (US) and Israel launched a joint military offensive against Iran, triggering the rapid closure of the Strait of Hormuz, a critical chokepoint through which roughly 20 percent of global petroleum supply and up to 30 percent of global liquefied natural gas (LNG) normally flows.[1] The International Energy Agency (IEA) characterised the disruption as “the largest supply shock in the history of the global oil market.”[2]

As of early July 2026, commercial traffic through the Strait stands at approximately 27 transits per day against a pre-war baseline of 84. That figure represents roughly 32 percent of normal volume, following a fragile US–Iran Memorandum of Understanding (MoU) signed on 17 June that reopened the waterway in principle but did not restore it in practice. War-risk insurance premiums remain at eight times the pre-crisis levels, vessel strikes continued throughout late June, and Iran has declared that it will charge transit fees with differential pricing for friendly nations, internationalising the governance dispute.[3]

For Southeast Asia, the closure led not just to an external price shock but a stress test of the region’s structural energy dependency. Most of the Association of Southeast Asian Nations (ASEAN) economies operate with lower refining sophistication, smaller strategic reserves, and a higher dependence on imported finished petroleum products rather than crude oil alone. The region is also internally uneven, spanning net exporters, mid-sized crude importers with some refining capacity, and entirely import-dependent economies with no meaningful buffer.

In 2025, crude oil imports from the Middle East accounted for 56 percent of ASEAN’s total.[4] The region’s dependence on the Gulf’s supply of LNG, particularly from Qatar, adds a second layer of vulnerability beyond oil.[5] Higher energy prices feed directly into food inflation, which accounts for 25–35 percent of ASEAN Consumer Price Index baskets, compressing household purchasing power and creating a classic stagflationary bind for central banks, leading to weakening growth.[6]

This paper assesses vulnerability across oil supply exposure, gas dependence, and the state of the renewable energy transition; examines the national and ASEAN-wide measures taken in response to the crisis; and maps these across all 11 ASEAN member states.

The picture that emerges is a spectrum. Brunei and Malaysia have experienced the shock primarily in terms of revenue; Indonesia, despite being the region’s largest oil producer, faces mounting fiscal strain as fuel subsidies overshoot budget assumptions; Singapore has managed through reserve depth and trading sophistication unavailable to its neighbours; Thailand and Vietnam face acute supply and fiscal pressure; and the Philippines, the only ASEAN member to declare a national energy emergency, sits at the sharpest end of the energy exposure spectrum. Cambodia, Laos, Myanmar, and Timor-Leste—countries with no refining capacity and the thinnest fiscal buffers in the region—are absorbing the crisis, with direct humanitarian consequences.

The crisis arrived in a global energy market already characterised by volatility on multiple fronts. Conflict in Ukraine, instability across the Middle East, and the potential for renewed disruptions in Venezuela had collectively raised operational and insurance costs, disrupted logistics and trade routes, and heightened investment risks, even in a market where supply was projected to exceed demand by up to four million barrels per day (bpd) in 2026.[7]

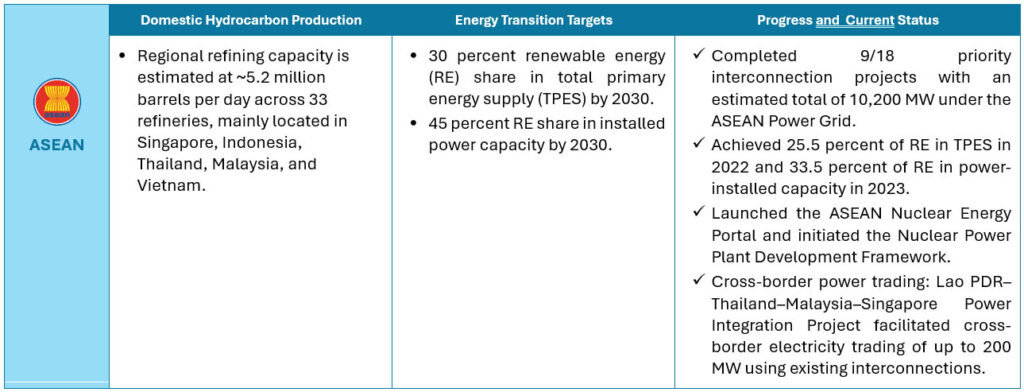

For ASEAN, this matters because the global market is not short of oil or gas in aggregate terms, but it is lacking in the right grades, delivered via the right routes, at a pace that matches the region’s immediate needs. The supply crisis has accelerated political attention to diversification and energy resilience. In April 2026, ASEAN energy ministers reaffirmed the bloc’s commitment to reduce energy intensity by 40 percent and achieve a 30 percent renewable share in total primary energy supply and 45 percent in installed power capacity by 2030.[8] Whether these ambitions and diversification strategies translate into structural change is the defining question.

ASEAN’s Energy Import Dependency

ASEAN’s energy profile is defined by a deepening structural reliance on imported hydrocarbons. Oil remains the largest energy source, accounting for around 42 percent of total final energy consumption. This demand is driven primarily by the transport sector where oil meets roughly 90 percent of consumption needs, and then the electricity sector, where it accounts for around 31 percent of generation fuel.[9] Oil import dependency reached 66 percent in 2024, with over 90 percent of crude sourced from outside the region, and ASEAN is projected to shift to a net natural gas importer by 2027.[10]

Table 1: ASEAN Energy Overview

Source: Author’s compilation using multiple sources.[11]

The ASEAN region requires approximately five million bpd but produces only around two million domestically, from Indonesia (840,000 bpd), Malaysia (570,000 bpd), Thailand (418,000 bpd), Vietnam (197,000 bpd), and Brunei (103,000 bpd), leaving a structural import gap of roughly three million barrels every day.[12] With the Strait of Hormuz closure, up to 28 percent of ASEAN’s final energy consumption was directly disrupted, and importing oil and gas at current crisis prices increased the region’s import costs by US$3.36 billion per month above 2026 expectations.[13]

Countries particularly vulnerable due to high oil import dependence include Vietnam (85 percent), Singapore (77 percent), Thailand (69 percent) and the Philippines (52 percent). [14] Strategic reserves across the region range between 20 and 65 days for most members, with Singapore as the outlier at over 200 days.[15] Malaysia, which relies on imports for only 25 percent of its oil consumption, has, for the first time, considered establishing a formal strategic petroleum reserve, revealing the scale and impact of the disruption.[16]

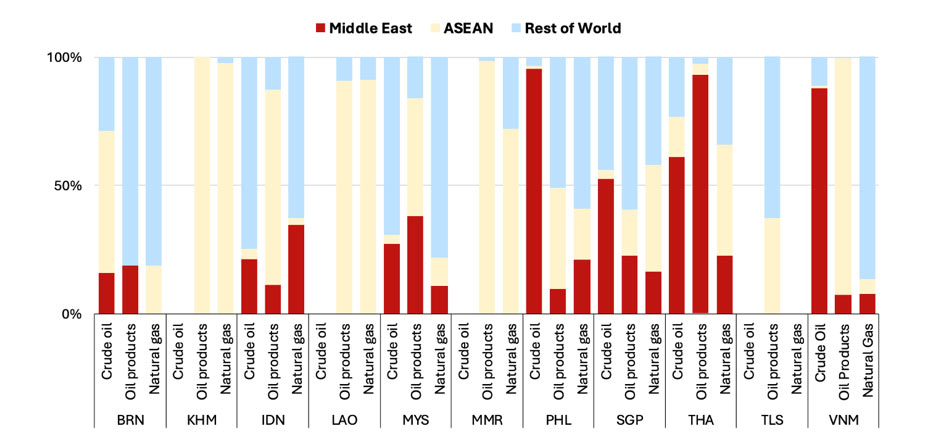

Figure 1: Share of Crude Oil and Natural Gas Imports from Different Parts of the World

Source: ASEAN Centre for Energy.[17]

Regional refining capacity across ASEAN is estimated at around 5.2 million bpd across 33 refineries, concentrated in Singapore, Indonesia, Thailand, Malaysia, and Vietnam, but many of these are configured for Middle Eastern crude, making feedstock substitution technically challenging and costly.[18] This structural constraint runs across all members to varying degrees.

Not all ASEAN economies are exposed to the Hormuz shock in the same way. Countries such as Singapore, Thailand, and Vietnam import crude oil and process it domestically, leading to their vulnerability being partly mediated by refining capacity and feedstock substitution options. In contrast, the Philippines, Cambodia, Myanmar, and Laos import refined petroleum products rather than crude, so the crisis hits them as a direct price and availability shock, with no refinery buffer. This distinction—crude importer versus product importer—combined with the presence or absence of domestic production, is why the impact of the same external disruption varies so dramatically across the 11 member states.

The gas dimension of this dependency is equally striking. Around 17 percent of ASEAN’s natural gas supply comes from the Middle East, translating to a 3 percent disruption in total consumption under current conditions.[19] For some economies, such as Singapore, this is more acute than the oil shock: over 95 percent of Singapore’s electricity is generated from LNG—of which nearly 60 percent is imported from Qatar.

Vietnam sources 49 percent, Indonesia 37 percent, Thailand 28 percent, and Singapore 17 percent of its respective LNG or liquid petroleum gas (LPG) from Gulf countries.[20] LNG as an energy security solution was already gaining momentum before the crisis, with US$20.4 billion in planned investment across proposed and under-construction import projects that would give the region a total import capacity of 121.3 million tons per annum (mtpa). However, whether expanding LNG infrastructure deepens dependency on Gulf countries or diversifies from it depends on sourcing decisions.[21]

Together, these structural conditions, including import dependence, restricted reserves, Gulf-calibrated refineries, and a gas transition tied to the same chokepoint, mean that the Strait of Hormuz’s closure not only disrupted ASEAN’s energy supply but also exposed the architecture of its vulnerability. The following section maps ASEAN’s spectrum of energy vulnerability across four clusters.

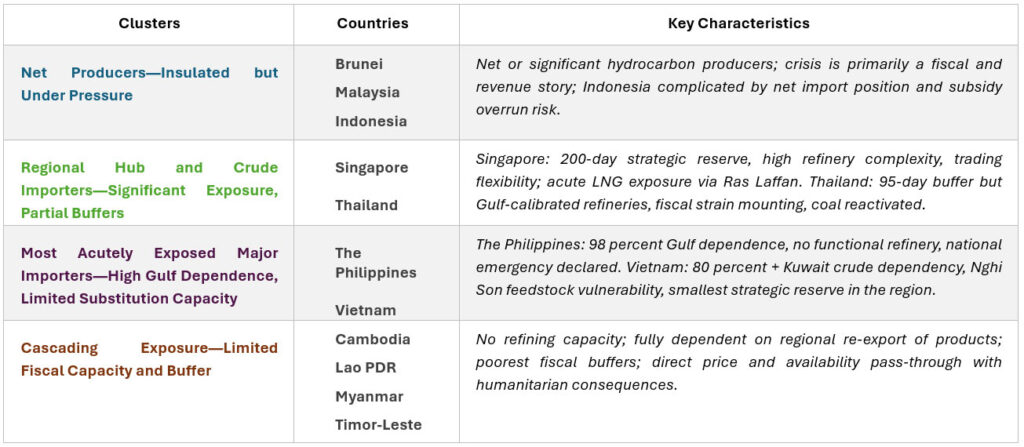

Country Clusters: A Spectrum of Vulnerability

The exposure of ASEAN’s member states to the crisis is shaped by an interplay of four factors that determine both the severity of the immediate shock and the structural options available to manage it. These are: whether a country is a domestic hydrocarbon producer, if it has the refining capacity to process crude or depends on imported finished products, how deeply its crude and gas supply chains are tied to the Gulf, and how far its renewable energy transition has progressed.

This section organises the 11 member states into four clusters for more clarity. Rather than a rigid taxonomy, this grouping is an analytical device to highlight the primary structural differences across the region.

- Cluster 1 (Brunei, Malaysia, and Indonesia) covers the net producers that have domestic output buffers, even if they are not fully insulated.

- Cluster 2 (Singapore and Thailand) covers the regional hub and crude importers that have refining infrastructure providing some degree of feedstock flexibility.

- Cluster 3 (The Philippines and Vietnam) covers the most acutely exposed major importers where high Gulf dependence is combined with limited substitution capacity.

- Cluster 4 (Cambodia, Laos, Myanmar, and Timor-Leste) covers the least-developed and most price-exposed economies, which have no domestic refining capacity and absorb the crisis as a direct product supply and price shock.

Table 2: Clusters and Their Key Characteristics

Source: Author’s own.

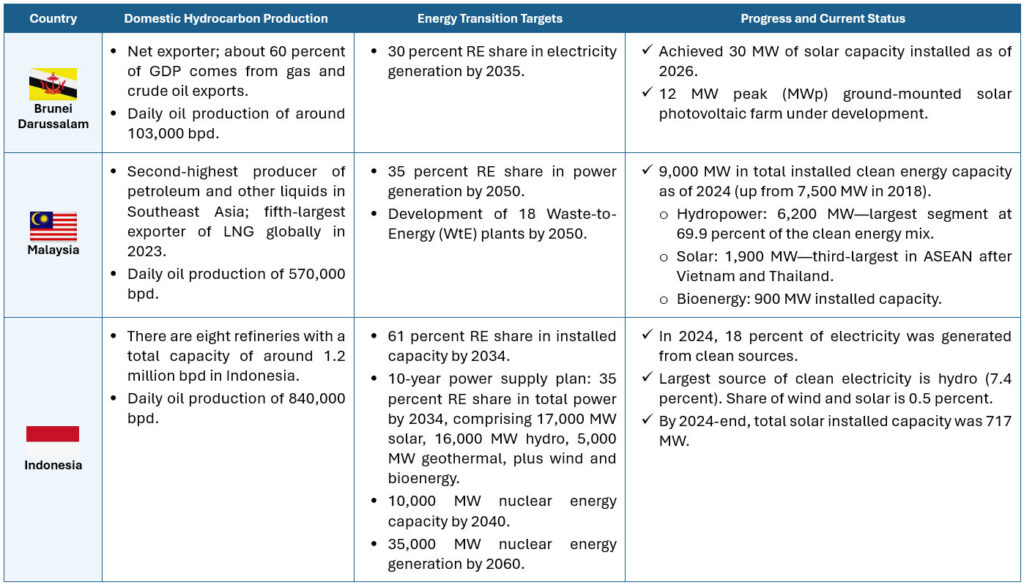

Cluster 1: Net Producers—Insulated but Under Pressure

Brunei, Malaysia, and Indonesia are the only ASEAN members with meaningful domestic hydrocarbon production, which distinguishes their degree of exposure from the rest of the region. For them, the Hormuz crisis is primarily a fiscal and downstream story rather than a supply security emergency, though the degree of insulation varies a lot across the three.

Table 3: The Net Producers

Source: Author’s compilation using multiple sources.[22]

Brunei is a net oil and LNG exporter that stands to benefit from elevated global prices. In April 2026, it exported 105,000 bpd of crude oil, highest in the past five years, of which 70 percent was shipped to Thailand.[23] It has not experienced the fuel price surges seen elsewhere in the region.[24] Its government reinforced energy security partnerships and implemented measures to manage domestic fuel consumption. Notably, Brunei introduced regulations requiring foreign-registered vehicles to enter the country with at least a three-quarters-full tank of fuel, showing cautious reserve management even from a position of relative strength.[25] Despite being a net exporter, it still incurs crude import costs of approximately US$505 million from the United Arab Emirates (UAE), showing that even producing states manage complex import–export balances across crude grades and refined products.[26]

Malaysia is a prominent crude oil and LNG producer and exporter through its state-owned Petronas. It has, however, been a net crude oil importer since 2022, as its domestic production has declined against rising consumption. In 2025, Malaysia remained a net crude oil importer, net LNG exporter, and small net petroleum products exporter.[27] It is largely insulated from supply disruption, and its oil import dependence sits at around 25 percent of consumption, the lowest among the major ASEAN importers.[28] However, fertiliser makers suspended new orders as Middle East supply chain disruptions drove up raw material prices. Malaysia’s monthly fuel subsidy bill saw a fourfold increase to approximately US$990 million in March 2026.[29] The government temporarily reduced the monthly subsidised fuel quota from 300 to 200 litres per consumer, and like several regional peers, is in discussions with Russia for crude supply. The Malaysian king’s Moscow visit in May 2026 is being widely interpreted as smoothening the path for an energy deal.[30] Malaysia’s transition is primarily through the managed redirection of its own LNG exports to meet domestic demand as coal capacity is reduced, with Petronas signing a non-binding agreement with Australia’s Woodside Energy in June 2025 for 1 mtpa of LNG supply from 2028.[31]

Indonesia is a net exporter of LNG and Southeast Asia’s largest oil producer, but remains a net oil importer because its domestic consumption outstrips production. Around 25 percent of its crude imports travel through Hormuz.[32] In May 2026, Indonesia’s oil and gas imports surged by 70.78 percent year on year.[33] Its in-country strategic reserve covers only around 23 days of consumption.[34] The government maintains generous fuel subsidies absorbing 30–40 percent of petrol and diesel prices, with 381.3 trillion rupiah (US$22.5 billion) allocated for fuel subsidies in the 2026 budget, based on oil at US$70 per barrel.[35] That assumption has been eroded by current price levels, and Indonesia now risks breaching its 3 percent deficit ceiling.[36] In response, the government has agreed to import approximately 150 million barrels of Russian crude in 2026, accelerated its biodiesel blending programme (B50 blend), and ordered flexible work arrangements to reduce fuel consumption.[37] Petrochemical firm PT Chandra Asri Pacific declared force majeure[a] on contractual obligations.[38]

On the transition front, Indonesia holds the largest Just Energy Transition Partnership (JETP) commitment in ASEAN at US$20 billion and has introduced programmes to foster renewable energy.[39] The government is also pushing ahead with a programme to switch power plants from diesel to LNG, though this could push Indonesia towards becoming a net LNG importer by the 2040s.[40]

Cluster 2: Regional Hub and Crude Importers—Significant Exposure, Partial Buffers

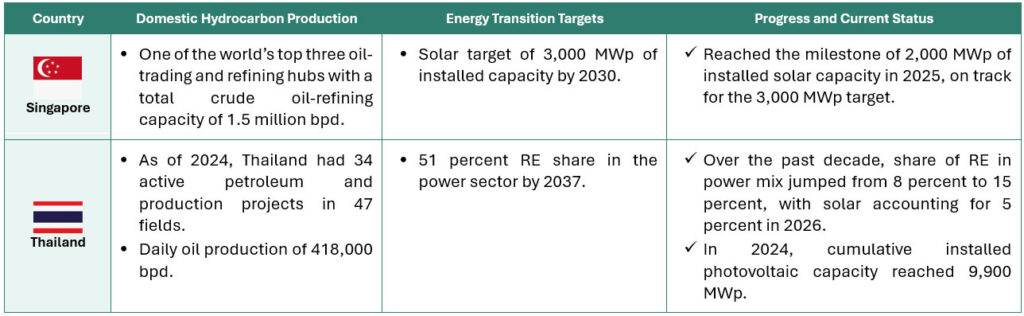

Both Singapore and Thailand have refining infrastructure that provides a degree of feedstock-processing capacity absent in the more exposed clusters, and both occupy strategically important roles in the region’s energy supply chain. The critical distinction within this cluster is that Singapore’s exposure is mediated by extraordinary reserve depth and trading sophistication, while Thailand’s is amplified by fiscal strain and a consumption economy directly feeling the price shock.

Table 4: Cluster 2—Regional Hub and Crude Importers

Source: Author’s compilation using multiple sources.[41]

Singapore is simultaneously the region’s most energy-import-dependent economy and its most operationally resilient. It has no domestic hydrocarbon production and imports virtually all of its energy, with over two-thirds of crude coming from the UAE, Qatar, Saudi Arabia, and Kuwait.[42] Its dependence on LNG is acute and specific: over 95 percent of its electricity is generated from LNG, and nearly 60 percent of that LNG was sourced from Qatar. The Iranian attacks on Qatar’s Ras Laffan complex, which forced a 17 percent production cut with repairs estimated to take several years, directly affected Singapore’s electricity tariffs.[43]

Singapore’s oil-refining facilities are among the most complex in the region. It can handle a wider range of crude grades than most ASEAN peers, giving it more substitution options, even as its Gulf feedstock concentration has grown.[44] However, its Gulf crude dependence rose to over 70 percent in 2025, up from around 50 percent in 2024, after ExxonMobil completed a refinery expansion specifically requiring additional heavy Gulf supply, a commercial investment decision made before the crisis that has since narrowed its feedstock options.[45] Recently, two of Singapore’s three refineries cut output due to constrained crude availability.[46]

What distinguishes Singapore from the rest of ASEAN is the depth of its buffers and the sophistication of its response mechanisms. Its strategic oil reserve, maintained in underground caverns at Jurong Island and other commercial storage facilities, is capable of supporting domestic demand for more than 200 days, far exceeding any other ASEAN member.[47] Singaporean Energy and Technology Minister Tan See Leng confirmed that the nation holds months of LNG and diesel stockpiles, though the precise figure has not been disclosed.[48]

Singapore has also leveraged its financial reserves to absorb price shocks rather than relying heavily on subsidies, a contrast to the fiscal strain visible across most of its neighbours.[49] Its role as a refining and trading hub has given it access to spot market flexibility and pricing mechanisms unavailable to smaller ASEAN economies. This trading sophistication has also enabled Singapore to secure bilateral energy arrangements, such as with Australia, where both have agreed to maintain mutual flows of Australian LNG into Singapore and Singaporean refined fuel into Australia, formalised through a legally binding protocol to their existing free trade agreement (FTA).[50]

On renewables, Singapore’s transition is constrained by geography, limited land area caps, and domestic solar deployment, but the city-state is pursuing regional grid interconnection through the ASEAN Power Grid initiative and has approved cross-border renewable energy imports from Cambodia and Indonesia as part of its longer-term decarbonisation strategy.[51]

Thailand is the region’s biggest crude importer after Singapore in terms of Gulf exposure, with 59 percent of crude oil and 28 percent of LNG imports vulnerable to the Hormuz blockade.[52] It has domestic refining capacity, including Thai Oil’s Sri Racha complex and Integrated Refinery and Petrochemical Complex, configured predominantly for medium-sour Gulf grades, which creates the same substitution challenge described in the broader Asian context.[53] After Singapore, it has the longest fuel buffer in the region at approximately 95 days, which has provided meaningful short-term insulation, but fiscal pressure is mounting rapidly.[54] Thailand’s Oil Fuel Fund, which caps diesel prices at 29.94 baht per litre, is seeking a loan due to a 1.5-billion-baht daily subsidy burden.[55] The government also banned exports of processed fuels except to Myanmar and Laos, reactivated the retired Mae Moh coal-fired power plant, and introduced work-from-home arrangements for civil servants to reduce consumption.[56] The government topped up state welfare cards with an additional 100 baht (approximately US$3.07) for fuel purchases, and is considering targeted electricity tariff relief limited to households consuming 200–300 kilowatt-hour (kWh) per month.[57] Thailand’s fisheries and tourism sectors, both strong GDP contributors, have also been hit hard.

Thailand is pivoting toward Russian crude and US supply as alternatives, following a pre-crisis agreement by the state-owned PTT Public Company Limited to import two million tonnes of LNG annually from the Alaska LNG project for 20 years.[58] As part of pre-crisis tariff negotiations with the US in April 2025, Thailand had already committed to importing an additional one million metric tonnes of US LNG in 2026 and another million over the following five years.[59] On renewables, Thailand had made meaningful progress in solar deployment before the crisis and has introduced programmes to accelerate renewable energy.

Cluster 3: Most Acutely Exposed Major Importers—High Gulf Dependence, Limited Substitution Capacity

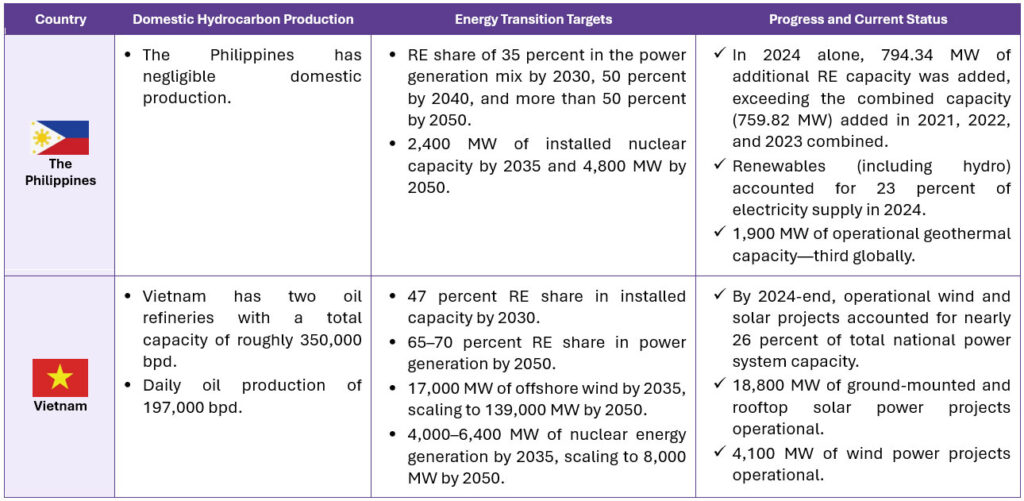

The Philippines and Vietnam combine high Gulf crude dependence with limited ability to rapidly substitute supplies, but for structurally different reasons. Vietnam has domestic refining capacity and was, until 2018, a crude exporter, giving it some operational levers. The Philippines has virtually none of these buffers and responded to the crisis with the most dramatic policy intervention out of all ASEAN members.

Table 5: Cluster 3—Most Acutely Exposed Major Importers

Source: Author’s compilation using multiple sources.[60]

The Philippines is the most acutely exposed major economy in ASEAN and the only country globally to declare a national energy emergency in response to the Hormuz closure. Philippine President Ferdinand Marcos Jr. signed an Executive Order on 25 March 2026, citing the “imminent danger posed upon the availability and stability of the country’s energy supply.”[61] The structural basis for this emergency is that the Philippines imports 98 percent of its oil from the Middle East and lacks a strategic petroleum reserve, relying entirely on commercial stocks.[62]

As of 20 March 2026, its Department of Energy reported average fuel stocks of 45 days, down from 55–57 days at the start of the conflict.[63] Diesel and petrol prices more than doubled, with diesel surging to nearly 150 pesos per litre.[64] LNG prices tripled and coal rose by up to 30 percent.[65] The government released a 20-billion-pesos emergency fund from the Malampaya gas fund, imposed a four-day government work week, and implemented 10–20 percent mandatory power and fuel cuts across all government agencies.[66] On 25 March, it also suspended fuel excise taxes, cutting diesel prices by over 20 pesos per litre and temporarily defusing planned transport strikes.[67] Nevertheless, according to the Philippine Institute for Development Studies, the energy crisis could push between 1.3 million and 3.1 million Filipinos into poverty.[68]

The Philippines has no operationally consequential domestic refinery. Petron’s Bataan facility functions primarily as a storage and blending terminal, not a full conversion refinery—it imports refined petroleum products rather than crude, and has no feedstock substitution option. In response to the Hormuz crisis, Manila received its first shipment of Russian crude in five years in March, approximately 750,000 barrels delivered to the Bataan facility. Petron Corporation confirmed purchasing around 2.48 million barrels of Russian crude to bolster supplies.[69] The government is also procuring two million barrels of oil as a state-owned buffer stock and is considering joint oil exploration with China.[70]

On renewables, the crisis has functioned as a direct accelerant: the Department of Energy fast-tracked 22 approved renewable projects to deliver an additional 1,471 megawatts (MW) by April 2026.[71] The Philippines had set a target of 35 percent renewable share in power generation by 2030 and 50 percent by 2040. In January 2026, it also discovered a new offshore gas field estimated to generate nearly 14 billion kWh of electricity annually. However, at approximately 4 percent of the Malampaya field’s reserves, it offers longer-term promise rather than immediate relief.[72]

Vietnam shares the acute import exposure of the Philippines but has a meaningfully different structural profile. It imports over 80 percent of its crude from Kuwait. In April 2026, for the first time since the 1991 Gulf War, Kuwait exported zero barrels of crude oil, leaving Vietnam directly affected by the Hormuz disruption.[73]

Vietnam sources approximately 85 percent of its oil import needs from outside the country, giving it one of the highest oil import dependence ratios in the region.[74] Its strategic petroleum reserve covers only 30–45 days of domestic demand.[75] Unlike the Philippines, however, it has two domestic refineries, Dung Quat and Nghi Son, giving it some crude processing capacity. Nghi Son was specifically designed around Kuwaiti crude under a long-term supply agreement, which creates a direct and acute feedstock vulnerability. In response, the Vietnamese government cut fuel import tariffs, tapped its price stabilisation fund, secured four million barrels of crude from non-Gulf sources, suspended crude exports, and accelerated its E10 ethanol-blending programme.[76] Jet fuel shortages have become acute as China and Thailand, Vietnam’s main jet fuel suppliers, have cut back on exports to serve their own markets, forcing Vietnam Airlines to cancel dozens of domestic flights.[77]

Vietnam began importing LNG only in 2023, and in January 2026, Petrovietnam Gas awarded its first-ever LNG term contract to Shell for approximately 400,000 tonnes per year from 2027 to 2031.[78] It has also expressed interest in Russian and Japanese crude imports as Gulf supply falters.[79]

On renewables, Vietnam stands out as an advanced transition story in ASEAN and has made rapid progress in solar and wind deployment—its JETP mechanism provides a structured financing pathway to accelerate the transition.[80] Vietnam’s Vingroup recently announced that it would halt construction of the country’s largest LNG-fired power plant, opting for a renewable energy project instead.[81] However, grid instability and curtailment remain constraints on how fast installed renewable capacity translates into reliable power.

Cluster 4: Cascading Exposure—Limited Fiscal Capacity and Buffer

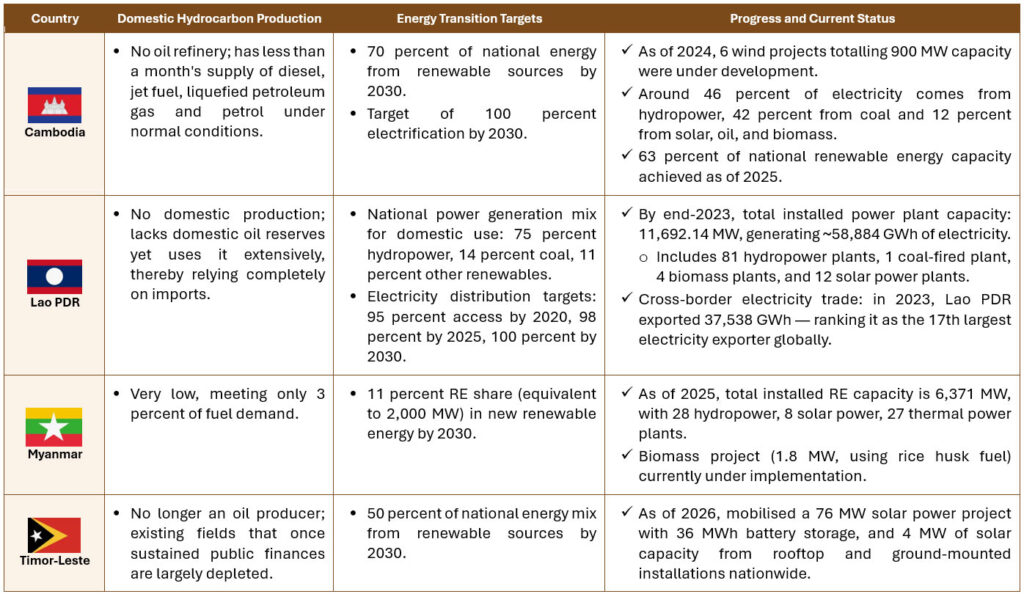

Cambodia, Laos, Myanmar, and Timor-Leste share a defining structural characteristic: none of them has meaningful domestic refining capacity, nor do they produce sufficient crude to buffer against external supply shocks. All import refined petroleum products rather than crude, meaning that the Hormuz disruption affects their markets in terms of product availability and price shock, with no intermediate filter. As the Economic Research Institute for ASEAN and East Asia (ERIA) notes, “[T]he small countries with small refining capacity are the countries that will suffer the most.”[82] Their fiscal capacity to absorb these shocks is also the weakest, and poverty rates remain at around 20 percent or more across the four countries, meaning that price pass-through has deeper socioeconomic repercussions.[83]

Table 6: Cluster 4—Cascading Exposure

Source: Author’s compilation using multiple sources.[84]

Cambodia does not produce crude domestically and has no refining capacity, importing all petroleum products primarily through Thailand, Vietnam, and Singapore. Approximately 2,000 of its 6,300 fuel stations were forced to close in the early weeks of the crisis, with around 400 still shut in mid-March 2026. Its strategic reserves cover less than 30 days of consumption.[85] When Thailand banned fuel exports and China restricted outbound shipments, Cambodia lost its primary supply channels and was forced to pivot to Singapore and Malaysia for relief.[86] The government eliminated import duties and value-added tax (VAT) on fuel and strengthened surveillance against hoarding and smuggling.[87] The crisis has also created renewed urgency for Cambodia to resolve a festering maritime dispute with Thailand and unlock undersea energy resources estimated to hold around 11 trillion cubic feet of natural gas, alongside large quantities of oil worth US$300 billion.[88]

Cambodia has announced plans for its own refinery and stockpile facility by 2029, a signal that the crisis has accelerated thinking about structural energy infrastructure, though the timeline and financing remain uncertain. Tourism, a critical economic pillar, is also under pressure from higher jet fuel costs and reduced regional flight connectivity. Data from the Cambodian government reveals that it imported mineral fuels, mineral oils, and related products worth over US$2 billion in the first five months of 2026, marking an over 27 percent year-on-year increase.[89]

Lao People’s Democratic Republic (PDR) has developed notable hydropower capacity and is a net electricity exporter to Thailand, Vietnam, and China through the regional Mekong grid, making it an energy exporter in one dimension while remaining wholly dependent on imported liquid fuels in another. But this provided no buffer against the liquid fuel shortage triggered by the Strait of Hormuz closure. In March 2026, Laos announced that fuel prices would be reviewed and could be adjusted every two to three days, instead of the previous seven-day schedule.[90] Hundreds of filling stations closed due to lack of fuel, and the school week was reduced from five days to three.[91] The country receives oil exports from Thailand under a bilateral energy cooperation arrangement and has procured additional supplies from Vietnam, while cutting fuel taxes and implementing consumption controls.[92] Laos illustrates a broader lesson the crisis highlighted across ASEAN: progress in one part of the energy system, even genuine, export-scale renewable capacity, does not confer resilience against disruption in another.

Myanmar has some legacy domestic oil and gas production, including the Yadana and Yetagun gas fields, but these have been disrupted by the political crisis following the 2021 military coup, with investment and maintenance severely curtailed. It has no noteworthy domestic refining capacity and relies on refined product imports from Singapore and Malaysia, whose refineries depend on Gulf supply.[93] The military junta introduced an odd–even fuel-rationing system in the early days of the crisis and imposed work-from-home requirements on Wednesdays.[94] Fuel shortages have raised concerns about the junta’s ability to sustain military operations, adding a security dimension to the energy crisis that is absent in other ASEAN nations.[95] Myanmar’s fiscal capacity to absorb price shocks is severely limited, and the combination of political instability, sanctions exposure, and energy vulnerability makes it difficult to assess, with low data reliability and opaque policy responses.

Timor-Leste is technically a hydrocarbon producer, but the Bayu-Undan gas field shut down in June 2025, eliminating the country’s primary production revenue. However, the Greater Sunrise gas field represents a potential resource. Timor-Leste imports all petroleum products and its strategic reserves sit at the lower end of the regional range.[96] The fuel situation was reportedly stable as of mid-March 2026, with the state-owned importer Esperança Timor Oan confirming sufficient reserves for approximately four months.[97] However, the International Monetary Fund (IMF) has warned that the petroleum fund, the country’s primary fiscal buffer, could be exhausted by the late 2030s if drawdown rates continue at current levels.[98] The crisis has added pressure to an already fragile fiscal position, and Timor-Leste’s longer-term energy security depends heavily on whether the Greater Sunrise gas field can be developed.

The humanitarian dimension of this cluster deserves explicit acknowledgement. Rising energy costs affect the price of almost all goods, directly or indirectly; therefore, fuel price inflation has immediate food security consequences. The World Food Programme had warned that if the conflict continues through mid-2026, an additional 45 million people globally could face acute hunger and Southeast Asia’s least-developed economies will not be immune.[99]

Vulnerability, Opportunity, and What Comes Next

The Hormuz closure did not create ASEAN’s energy vulnerability but exposed it. The structural dependencies exposed by the 2026 crisis were decades in the making: an energy profile dominated by imported hydrocarbons, refining infrastructure calibrated for Gulf feedstock, strategic reserves too thin to absorb a prolonged disruption, and a renewable transition that has consistently fallen short of its own targets.

ASEAN countries were aiming for renewables to make up 23 percent of primary energy supply by 2025 but reached only 13.5 percent as of October 2025, a gap that required an annual investment of US$27 billion against the US$8 billion the region actually received between 2016 and 2021.[100] In the near term, limited alternatives to fossil fuels mean that industrial energy use remains heavily reliant on coal and gas, and several governments have responded to the immediate shock by reactivating coal capacity and expanding fossil fuel subsidies.

ASEAN has never had a single energy economy, and that divergence in endowments, consumption structures, and transition capacities has defined the region’s crisis response as much as any external factor. Collaboration across ASEAN has remained limited, with countries largely focused on individual energy security needs and a notable absence of coordinated multilateral response in the weeks following the crisis. Where collective arrangements have been slow to materialise, individual governments have acted on national interest, such as turning to a sanctioned supplier like Russia while navigating complex geopolitical terrain with Washington.

The ASEAN Petroleum Security Agreement (APSA), signed in 2009 but not enforced, is now being pushed to enable coordinated emergency fuel sharing. Its structural weaknesses, including reliance on voluntary commercial assistance and lack of clear implementation guidelines, are apparent.[101] More concretely, there are signs that the crisis is generating institutional momentum beyond rhetorical commitment. On 11 May 2026, Indonesia proposed hosting a joint ASEAN strategic oil reserve hub in Sumatra, working with Malaysia, Brunei, and the Philippines to advance the initiative, while simultaneously preparing a separate national oil storage facility in a Sumatran Special Economic Zone to bolster its own reserves.[102] The proposal, if realised, would mark the biggest step towards collective ASEAN energy security infrastructure since the APSA was signed.

The ASEAN Power Grid, long running but now with renewed political urgency, has similarly been pushed towards operationalisation, endorsed by officials as one of the most consequential cooperative projects the bloc could deliver for its populations. Yet, the gap between ASEAN’s grid ambitions and actual integration remains stark, as it is still working through basic requirements such as harmonising technical standards, setting rules for power transmission and payments, and establishing dispute resolution mechanisms.[103] The current crisis may be the forcing function that accelerates both the political will and the regulatory harmonisation that years of incremental progress have not delivered.

The longer-term signals are more constructive, though the distance between commitment and delivery remains large. Under coordinated policy action, ASEAN could reduce its total primary energy supply by 5.5 percent through displacing imported oil and coal with domestic renewables, thus enhancing energy self-sufficiency while maintaining security.[104] The ASEAN Renewable Electricity Coupling pathway projects utility-scale solar capacity rising to triple its current value, wind sevenfold, and battery storage fourfold by 2030, but achieving this requires an average annual investment of around US$77 billion, grid reinforcement, enhanced flexibility and large-scale storage deployment.[105] The JETP commitments in Indonesia (US$3.1 billion deployed) and Vietnam (24 projects worth over US$7 billion identified) represent genuine institutional progress. So do the Lao–Thailand–Malaysia–Singapore and Brunei–Indonesia–Malaysia–Philippines Power Integration Projects that advance cross-border electricity trading and are essential for the region’s long-term transition.[106] The gap between political commitment and operational reality, though, remains the defining challenge.

Conclusion

The long-term implications of the crisis extend well beyond the current supply disruption. For ASEAN specifically, the geopolitical and economic implications may last for decades. Even a partial or sustained intermittent closure would push several governments past the point where subsidy expansion and fiscal tools can absorb the shock, raising the prospects of fuel rationing, power outages, and social instability at a much higher scale than what the current crisis has so far projected. The food security implications for hundreds of millions of people across the region also make the economic case for de-escalation overwhelming.

The 2026 crisis is perceived as a litmus test for ASEAN’s energy security and the adaptability of its foreign policy. Governments have responded with speed and pragmatism, but the structural conditions that made the shock severe remain intact. It is now up to the ASEAN countries to treat the shock as a mandate for structural change, and accelerate reserve-building, grid investment, and diversification.

Parul Bakshi is Fellow, Energy and Climate, ORF Middle East.

The author acknowledges the use of Claude Sonnet 4.6 as an editorial support tool during the preparation of this paper. The originality, intellectual contribution, analysis, and conclusions of the paper remain the author’s own.

All views expressed in this publication are solely those of the author, and do not represent the Observer Research Foundation, either in its entirety or its officials and personnel.

Endnotes

[a] A contractual clause that relieves parties from liability or obligation when an extraordinary, unforeseeable, and unavoidable event beyond their control occurs.

[1] Jay Hilotin, “What the Hormuz Shutdown Means for Asean: Explainer,” Gulf News, April 15, 2026, https://gulfnews.com/world/asia/what-the-hormuz-shutdown-means-for-aseans-energy-security-renewables-10-things-to-know-1.500507341.

[2] “IEA Warns Iran War Oil Shock Will Cut Supply, Cause Demand to Shrink,” Reuters, April 14, 2026, https://www.reuters.com/business/energy/iran-war-upends-ieas-global-oil-market-outlook-2026-04-14/.

[3] Straits, “Hormuz Live Monitor,” https://straits.live/ https://global-energy-flow.com/hormuz/.

[4] Elbinsar Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses,” Fulcrum, 2026, https://fulcrum.sg/the-war-against-iran-and-the-fragility-of-southeast-asias-energy-responses/.

[5] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses.”

[6] J.P. Morgan, “How does the Middle East conflict affect Asia,” 2026, https://privatebank.jpmorgan.com/apac/en/insights/markets-and-investing/asf/how-does-the-middle-east-conflict-affect-asia.

[7] ASEAN Centre for Energy, ASEAN Energy in 2026, February 2026, https://aebf.aseanenergy.org/publications/asean-energy-in-2026.

[8] ASEAN, “Joint Statement of the Special ASEAN Ministers on Energy Meeting (AMEM) on the Latest Situation in the Middle East,” ASEAN Main Portal, 2026, https://asean.org/joint-statement-of-the-special-asean-ministers-on-energy-meeting-amem-on-the-latest-situation-in-the-middle-east/.

[9] ASEAN Energy in 2026; ASEAN Centre for Energy, ASEAN Energy Security Insights: Implications of the Middle East Situation, April 2026, https://storage.googleapis.com/aceweb-bucket-261225/pdf/publication/ASEAN%20Energy%20Security%20Insights_UHZRdTbAOcoGgHJqvGt4mp84UwDHtU9abdA6DART.pdf

[10] ASEAN Energy in 2026.

[11] “From Shock to Strategy: Strengthening ASEAN Energy Security and Economic Resilience after the Strait of Hormuz Disruption,” Economic Research Institute for ASEAN and East Asia, Issue Paper 2026-1; ASEAN Centre for Energy, ASEAN Energy in 2026, February 2026, https://aebf.aseanenergy.org/publications/asean-energy-in-2026.

[12] Gita Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis,” Carnegie Endowment for International Peace, 2026, https://carnegieendowment.org/posts/2026/04/southeast-asias-agency-amid-the-new-oil-crisis.

[13] “ASEAN Energy Security Insights: Implications of the Middle East Situation, April 2026”

[14] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[15] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[16] “Malaysia Considers Establishing Strategic Petroleum Reserve,” Vietnam+ (VietnamPlus), April 21, 2026, https://en.vietnamplus.vn/malaysia-considers-establishing-strategic-petroleum-reserve-post341427.vnp.

[17] ASEAN Energy Security Insights: Implications of the Middle East Situation.”

[18] “From Shock to Strategy: Strengthening ASEAN Energy Security and Economic Resilience after the Strait of Hormuz Disruption,” Economic Research Institute for ASEAN and East Asia (ERIA), April 2026, https://www.eria.org/publications/from-shock-to-strategy–strengthening-asean-energy-security-and-economic-resilience-after-the-strait-of-hormuz-disruption.

[19] ASEAN Energy Security Insights: Implications of the Middle East Situation.

[20] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[21] “It Is Unclear if LNG Imports can Guarantee Southeast Asia’s Energy Security,” Zero Carbon Analytics, February 2026, https://zerocarbon-analytics.org/insights/briefings/it-is-unclear-if-lng-imports-can-guarantee-southeast-asias-energy-security/.

[22] ASEAN Centre for Energy, ASEAN Energy in 2026, February 2026, https://aebf.aseanenergy.org/publications/asean-energy-in-2026; “Brunei and fossil gas,” Global Energy Monitor, https://www.gem.wiki/Brunei_and_fossil_gas#cite_note-:1-3; Hibiscus Petroleum, https://www.hibiscuspetroleum.com/wp-content/uploads/2026/02/HPB-Press-Release-Brunei-Solar-Ground-Breaking-Final.pdf, 2026; EIA, “Malaysia Energy Profile: Second-Highest Producer Of Petroleum And Other Liquids In Southeast Asia – Analysis,” Eurasia Review, 2024, https://www.eurasiareview.com/14112024-malaysia-energy-profile-second-highest-producer-of-petroleum-and-other-liquids-in-southeast-asia-analysis/; Gita Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis,” Carnegie Endowment for International Peace, 2026, https://carnegieendowment.org/posts/2026/04/southeast-asias-agency-amid-the-new-oil-crisis; “Indonesia Overview,” Energy Information Administration, 2025, https://www.eia.gov/international/analysis/countri/IDN; Indira Pradnyaswari, Rhea Oktaqiara, Edelweis Agatha Zaneta Devi and Zahrah Zafira, et al., 2025 Recap – Renewable Energy Insights, ASEAN Centre for Energy, 2026, https://aseanenergy.org/publications/2025-recap-renewable-energy-insights; Silvira Ayu Rosalia, Fadel Maulana and Marcel Nicky Arianto, 2025 Recap – Electricity Insights, ASEAN Centre for Energy, 2026; “Indonesia,” Ember, 2026, https://ember-energy.org/countries-and-regions/indonesia/; IRENA, Renewable capacity statistics 2025, International Renewable Energy Agency, https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2025/Mar/IRENA_DAT_RE_Capacity_Statistics_2025.pdf; Viktor Tachev, “Malaysia Nears Its 40% Renewable Energy Target by 2035,” Energy Tracker Asia, August 2024, https://energytracker.asia/malaysia-nears-its-renewable-energy-target-by-2035/.

[23] Sribala Subramanian, “Brunei Pumps More Oil,” The Diplomat, June 18, 2026, https://thediplomat.com/2026/06/brunei-pumps-more-oil/.

[24] “IEA Warns Iran War Oil Shock will Cut Supply, Cause Demand to Shrink.”

[25] “Brunei to Bar Foreign Vehicles with Tanks Less than Three-Quarters Full from April,” Reuters, March 31, 2026, https://www.reuters.com/business/energy/brunei-bar-foreign-vehicles-with-tanks-less-than-three-quarters-full-april-2026-03-31/.

[26]“Brunei Imports from United Arab Emirates of Crude Oil – 2026 Data 2027 Forecast 1994-2024 Historical,” Trading Economics, https://tradingeconomics.com/brunei/imports/united-arab-emirates/crude-oil-petroleum-bituminous-minerals.

[27] Lee Heng Guie, “Oil Shocks in the Malaysian Perspective,” The Star, March 19, 2026, https://www.thestar.com.my/business/insight/2026/03/19/oil-shocks-in-the-malaysian-perspective.

[28] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[29] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses.”

[30] Ian Storey, “Southeast Asia and the Third Gulf War: Impact, Responses and Implications,” ISEAS – Yusof Ishak Institute, No. 25 (2026), https://www.iseas.edu.sg/wp-content/uploads/2026/03/ISEAS-Perspective_2026_25.pdf.

[31] “It Is Unclear if LNG Imports can Guarantee Southeast Asia’s Energy Security.”

[32] Maythiwan Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis,” CASE for Southeast Asia, 2026, https://caseforsea.org/energy-security-in-the-shadow-of-war-how-case-countries-are-navigating-the-2026-fuel-crisis/.

[33] Xinhua, “Indonesia’s Oil, Gas Imports Jump 70.78 pct in May,” English News, July 1, 2026, https://english.news.cn/asiapacific/20260701/1071f06477d94949b3154b7523e2df3a/c.html.

[34] “ASEAN Countries Exposed by Middle East oil Dependence,” Vietnam Investment Review, March 23, 2026, https://vir.com.vn/asean-countries-exposed-by-middle-east-oil-dependence-149076.html.

[35] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[36] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses.”

[37] Hilman Palaon, “Indonesia Believes in Cheap Fuel,” Lowy Institute, 2026, https://www.lowyinstitute.org/the-interpreter/indonesia-believes-cheap-fuel ; Jay Hilotin, “More Asean States Turn to Russian Fuel as Hormus Strait Disruptions Batter Global Energy Supply,” Gulf News, April 28, 2026, https://gulfnews.com/world/asia/more-asean-states-turn-to-russian-fuel-as-hormus-strait-disruptions-batter-global-energy-supply-1.500521348.

[38] Sreeparna Banerjee and Abhishek Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability,” Observer Research Foundation, 2026, https://www.orfonline.org/expert-speak/the-middle-east-crisis-and-southeast-asia-s-energy-vulnerability.

[39] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses;” “The Race to Invest in Southeast Asia’s Green Economy,” Zero Carbon Analytics, 2025, https://zerocarbon-analytics.org/insights/briefings/the-race-to-invest-in-southeast-asias-green-economy/.

[40] “It Is Unclear if LNG Imports can Guarantee Southeast Asia’s Energy Security.”

[41] Gita Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis”; International Trade Administration, “Singapore – Oil & Gas,” Energy Resource Guide, 2021, https://www.trade.gov/energy-resource-guide-singapore-oil-and-gas; Tim Daiss, “Gulf of Thailand oil and gas exploration faces stubborn hurdles,” Gas Outlook, March 2024, https://gasoutlook.com/analysis/gulf-of-thailand-oil-and-gas-exploration-faces-stubborn-hurdles/; Singapore Energy Market Authority, https://www.ema.gov.sg/news-events/news/media-releases/2026/Singapore-to-Accelerate-Solar-Deployment-to-Meet-3-GWp-Solar-Target-by-2030, 2026; Viktor Tachev, “Renewable Energy in Thailand: An Alternative to LNG,” Energy Asia Tracker, 2026, https://energytracker.asia/renewable-energy-in-thailand-an-alternative-to-lng/.

[42] US Energy Information Administration, “Singapore,” 2021, https://www.eia.gov/international/analysis/country/SGP.

[43] Storey, “Southeast Asia and the Third Gulf War: Impact, Responses and Implications.”

[44] “The Reasons Behind Asia’s Reliance on Middle East Oil Supplies,” Baird Maritime / Work Boat World, March 4, 2026, https://www.bairdmaritime.com/shipping/tankers/the-reasons-behind-asias-reliance-on-middle-east-oil-supplies.

[45] “ExxonMobil’s Singapore Refinery Starts Up a New Unit, Expanding High-Sulphur Crude Intake,” Baird Maritime / Work Boat World, September 23, 2025, https://www.bairdmaritime.com/shipping/ports/exxonmobils-singapore-refinery-starts-up-a-new-unit-expanding-high-sulphur-crude-intake.

[46] Doug Dingwall, “Singapore’s Major Oil Source Is Blocked and Experts Warn Australians Will Pay,” ABC News, April 2, 2026, https://www.abc.net.au/news/2026-04-02/singapore-oil-refineries-energy-shock-response/106504438.

[47] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[48] “ASEAN Countries Exposed by Middle East Oil Dependence.”

[49] Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability.”

[50] “Australia, Singapore Leaders Pledge Closer Energy Ties to Tackle Global Supply Shock,” Hydrocarbon Processing, April 10, 2026, https://www.hydrocarbonprocessing.com/news/2026/04/australia-singapore-leaders-pledge-closer-energy-ties-to-tackle-global-supply-shock/.

[51] Dinita Setyawati et al., “Regional Grids Key to Singapore’s Energy Future,” Ember, 2024, https://ember-energy.org/latest-insights/regional-grids-key-to-singapores-energy-future.

[52] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis.”

[53] Tita Sanglee, “Thailand’s Brittle Defense Against Oil Shocks,” The Diplomat, April 1, 2026, https://thediplomat.com/2026/04/thailands-brittle-defense-against-oil-shocks/.

[54] ” ASEAN Countries Exposed by Middle East Oil Dependence.”

[55] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses;” “Energy Minister Caps Diesel at 29.94 Baht for 15 Days Using Oil Fuel Fund,” The Nation, March 4, 2026, https://www.nationthailand.com/news/policy/40063274.

[56] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses;” Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability.”

[57] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis.”

[58] “It Is Unclear if LNG Imports can Guarantee Southeast Asia’s Energy Security.”

[59] “It Is Unclear if LNG Imports can Guarantee Southeast Asia’s Energy Security.”

[60] ASEAN Centre for Energy, ASEAN Energy in 2026, February 2026, https://aebf.aseanenergy.org/publications/asean-energy-in-2026; Gita Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis”; “2025 Recap – Renewable Energy Insights”; Gawoon Philip Vahn, Neo Rong Wei and Newsdesk-Vietnam, “Vietnam hopes to become self-reliant on oil products with 2027 mega refinery target,” S&P Global, 2023, https://www.spglobal.com/energy/en/news-research/latest-news/crude-oil/010623-vietnam-hopes-to-become-self-reliant-on-oil-products-with-2027-mega-refinery-target; “Philippines streamlines licensing for nuclear projects,” World Nuclear News, February 2026, https://www.world-nuclear-news.org/articles/philippines-streamlines-licensing-for-nuclear-projects; Kris Crismundo, “PH installs record-high renewable energy capacity of 794 MW in 2024,” Philippines News Agency, 2025, https://www.pna.gov.ph/articles/1243853; “Solar Shines the Path for the Philippines to Reduce Reliance on Fossil Fuel Imports,” BloombergNEF, 2025, https://about.bnef.com/insights/clean-energy/solar-shines-the-path-for-the-philippines-to-reduce-reliance-on-fossil-fuel-imports/; “Vietnam: Power Sector Snapshot,” Norton Rose Fulbright, November 2025, https://www.nortonrosefulbright.com/en/knowledge/publications/1d041eb0/vietnam-power-sector-snapshot; Junaid Shah, “Vietnam Plans Two Renewable Energy Hubs by 2030 Under Revised JETP Roadmap,” Saur Energy, March 2026, https://www.saurenergy.com/solar-energy-news/vietnam-plans-two-renewable-energy-hubs-by-2030-under-revised-jetp-roadmap-11259111.

[61] Philippine Information Agency, “President Marcos Declares State of National Energy Emergency; Activates Uplift as Whole-Of-Government Response Framework,” 2026, https://pia.gov.ph/news/president-marcos-declares-state-of-national-energy-emergency-activates-uplift-as-whole-of-government-response-framework/.

[62] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis.”

[63] “Philippines Fuel Supply: 45-Day Reserve, Price Hikes Expected,” News Usa Today, March 25, 2026, https://news-usa.today/philippines-fuel-supply-45-day-reserve-price-hikes-expected-march-2026/.

[64] Stacey Nicole Bellido, “Philippines First Nation to Declare Energy Emergency Amid Iran War,” Asia Times, March 28, 2026, https://asiatimes.com/2026/03/philippines-first-nation-to-declare-energy-emergency-amid-iran-war/

[65] Edjen Oliquino, “Garin Pushes Shift to EV, Review of Oil Deregulation Law,” Daily Tribune, April 13, 2026, https://tribune.net.ph/2026/04/13/garin-pushes-shift-to-ev-review-of-oil-deregulation-law.

[66] Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability.”

[67] James Karuga, “Philippines Faces Energy Emergency as Global Oil Crisis Exposes Deep Vulnerabilities,” Development Aid, April 21, 2026,

https://www.developmentaid.org/news-stream/post/206233/philippines-energy-emergency.

[68] Philippine Institute for Development Studies, Republic of the Philippines, “Oil Price Surge May Push 1.34 Million Filipinos into Poverty,” April 17, 2026, https://www.pids.gov.ph/details/news/press-releases/oil-price-surge-may-push-1-34-million-filipinos-into-poverty-pids.

[69] Hilotin, ” More Asean States turn to Russian Fuel as Hormus Strait Disruptions Batter Global Energy Supply.”

[70] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis”

[71] James Karuga, “Philippines Faces Energy Emergency as Global Oil Crisis Exposes Deep Vulnerabilities.”

[72] “It Is Unclear if LNG imports can Guarantee Southeast Asia’s Energy Security.”

[73] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis.”

[74] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[75] “ASEAN Countries Exposed by Middle East Oil Dependence.”

[76] Kiatgrajai, “Energy Security in the Shadow of Geopolitical Conflict: How CASE Countries are Navigating the 2026 Fuel Crisis;” “ASEAN Countries Exposed by Middle East Oil Dependence.”

[77] Michael Sullivan, ” Southeast Asia is being hit hard by Iran’s cutoff of oil and gas,” NPR, March 26, 2026, https://www.npr.org/2026/03/26/nx-s1-5760763/southeast-asia-is-being-hit-hard-by-irans-cutoff-of-oil-and-gas.

[78] “It Is Unclear if LNG imports can Guarantee Southeast Asia’s Energy Security.”

[79] Hilotin, “More Asean States turn to Russian Fuel as Hormus Strait Disruptions Batter Global Energy Supply.”

[80] “The Race to Invest in Southeast Asia’s Green Economy.”

[81] Francesco Guarascio, “Exclusive: Vingroup Proposes Scrapping LNG-Powered Plant Plan for Renewables amid Iran War, Document Shows,” Reuters, March 31, 2026, https://www.reuters.com/sustainability/climate-energy/vingroup-proposes-scrapping-lng-powered-plant-plan-renewables-amid-iran-war-2026-03-31/.

[82] Sullivan, “Southeast Asia Is Being Hit Hard by Iran’s Cutoff of Oil and Gas.”

[83] Jayant Menon, “Fuel Shock Hits Southeast Asia’s Poorest,” East Asia Forum, April 24, 2026, https://eastasiaforum.org/2026/04/24/fuel-shock-hits-southeast-asias-poorest/.

[84] ASEAN Centre for Energy, ASEAN Energy in 2026, February 2026, https://aebf.aseanenergy.org/publications/asean-energy-in-2026; Sudarshan Varadhan, “Cambodia turns to Singapore, Malaysia for fuel as Vietnam, China restrict supplies,” Reuters, March 2026, https://www.reuters.com/business/energy/cambodia-turns-singapore-malaysia-fuel-vietnam-china-restrict-supplies-2026-03-18/; “Global Oil Shock and Myanmar’s Energy Security,” ISP OnPoint, March 12, 2026, https://ispmyanmar.com/op2026-01/; Ruengsak Thitirasakul, “Energy Supply Security of Lao PDR and Implications for ASEAN,” ERIA, https://www.eria.org/uploads/3_Part_2-Ch_2_Energy-Supply-Security.pdf; Eric Koons, “Renewable Energy in Cambodia: Continued Growth,” Energy Tracker Asia, 2024, https://energytracker.asia/renewable-energy-in-cambodia/; Enerdata, Cambodia energy report, https://www.enerdata.net/estore/country-profiles/cambodia.html; “Cambodia reaffirms renewable energy target with 900 MW of wind projects,” Enerdata, 2025, https://www.enerdata.net/publications/daily-energy-news/cambodia-reaffirms-renewable-energy-target-900-mw-wind-projects.html; Joao Boavida, “The oil shock to Timor-Leste’s economy,” Lowy Institute, March 2026, https://www.lowyinstitute.org/the-interpreter/oil-shock-timor-leste-s-economy; Country Statement of Timor-Leste, https://www.unescap.org/sites/default/d8files/event-documents/24.%20Timor-Leste_1.pdf, 2026; MDPI Energies, Prioritization of Renewable Energy for Sustainable Electricity Generation and an Assessment of Floating Photovoltaic Potential in Lao PDR, 2022; Republic of Myanmar, Nationally Determined Contributions, 2021; ASEAN Centre for Energy, Lao PDR Ministry of Energy and Mines, “An Energy Sector Roadmap to Net Zero Emissions for Lao PDR,” 2025, https://storage.googleapis.com/aceweb-bucket-261225/files/publication/1766846384_An-Energy-Sector-Roadmap-to-Net-Zero-Emissions-for-Lao-PDR.pdf; “Myanmar implements 11 solar power plant projects,” Global New Light of Myanmar, February 2025, https://www.gnlm.com.mm/myanmar-implements-11-solar-power-plant-projects/; “Myanmar to develop 1.8-MW biomass plant,” Southeast Asia Infrastructure, https://southeastasiainfra.com/myanmar-to-develop-1-8-mw-biomass-plant/; Chea Vannak, “Cambodia’s Power Capacity Grows 14.4% to Almost 6,000 MW in 2025,” AKP Agence Kampuchea Presse, February 2026, https://www.akp.gov.kh/post/detail/362129.

[85] Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability.”

[86] Sebastian Strangio, “In Southeast Asia, the Scramble for Energy Is On,” The Diplomat, March 20, 2026, https://thediplomat.com/2026/03/in-southeast-asia-the-scramble-for-energy-is-on/.

[87] Purba, “The War Against Iran and the Fragility of Southeast Asia’s Energy Responses.”

[88] Devjyot Ghoshal and Josh Smith, “Global Fuel Crisis Adds Urgency to Cambodian Push to Tap $300 Billion Energy Resources,” Reuters, May 27, 2026, https://www.reuters.com/business/energy/global-fuel-crisis-adds-urgency-cambodian-push-tap-300-billion-energy-resources-2026-05-27/.

[89] Yatt Malai, ‘Cambodia’s Oil and Fuel Import Bill Reaches Over $2 Billion,’ Kiripost, June 10, 2026, https://kiripost.com/stories/cambodias-oil-and-fuel-import-bill-reaches-hits-over-2-billion.

[90] “Laos Adjusts Fuel Pricing Mechanism due to Soaring Oil Prices Amid West Asia Tensions” The Star, March 13, 2026, https://www.thestar.com.my/aseanplus/aseanplus-news/2026/03/13/laos-adjusts-fuel-pricing-mechanism-due-to-soaring-oil-prices-amid-west-asia-tensions#goog_rewarded.

[91] Storey, “Southeast Asia and the Third Gulf War: Impact, Responses and Implications;” Michael Sullivan, “Southeast Asia Is Being Hit Hard by Iran’s Cutoff of Oil and Gas.”

[92] Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability”

[93] “Global Oil Shock and Myanmar’s Energy Security,” ISP OnPoint, March 12, 2026, https://ispmyanmar.com/op2026-01/.

[94] Banerjee and Sharma, “The Middle East Crisis and Southeast Asia’s Energy Vulnerability” ; Spencer Feingold, “Middle East war: 6 ways countries are responding to the historic energy shock,” World Economic Forum, April 24, 2026, https://www.weforum.org/stories/2026/04/middle-east-war-iran-us-ways-countries-respond-oil-energy-shock/.

[95] Sebastian Strangio, “In Southeast Asia, the Scramble for Energy Is On.”

[96] Wirjawan, “Southeast Asia’s Agency Amid the New Oil Crisis.”

[97] Strangio, “In Southeast Asia, the Scramble for Energy Is On.”

[98] International Monetary Fund, Democratic Republic of Timor-Leste, 2025, https://www.imf.org/en/publications/cr/issues/2025/09/25/democratic-republic-of-timor-leste-2025-article-iv-consultation-press-release-staff-report-570720.

[99] Menon, “Fuel Shock Hits Southeast Asia’s Poorest.”

[100] “The Race to Invest in Southeast Asia’s Green Economy”

[101] Menon, “Fuel Shock Hits Southeast Asia’s Poorest.”

[102] “Indonesia proposes hosting ASEAN oil storage hub to boost regional reserves,” Channel News Asia, May 12, 2026, https://www.channelnewsasia.com/asia/indonesia-proposes-asean-oil-storage-hub-boost-regional-reserves-6115311?cid=FBcna.

[103] Syahpati Alfatarah, “Plugging into Reality: The ASEAN Power Grid,” The Diplomat, April 17, 2026, https://thediplomat.com/2026/04/plugging-into-reality-the-asean-power-grid/.

[104] ASEAN Energy Security Insights: Implications of the Middle East Situation.”

[105] Indira Pradnyaswari, Rhea Oktaqiara, Edelweis Agatha Zaneta Devi and Zahrah Zafira, et al., 2025 Recap – Renewable Energy Insights, ASEAN Centre for Energy, 2026, https://aseanenergy.org/publications/2025-recap-renewable-energy-insights.

[106] Pradnyaswari et al., 2025 Recap-Renewable Energy Insights.