Occasional Paper | 17 April, 2026 Download Report (PDF)

The Egypt-GCC Economic Relationship in an Era of Strategic Transformation

Despite unprecedented political alignment and substantial capital inflows between the Arab Republic of Egypt and the Gulf Cooperation Council (GCC) states in the past 15 years, economic integration between the two remains structurally shallow, asymmetric, and inconsistent. This paper diagnoses the root cause of this paradox as the ‘missing middle’—the systemic absence of institutional, financial, and logistical mechanisms needed to translate macro-level strategic alliances into micro-level industrial co-creation. With approximately 76 percent of foreign direct investment concentrated in non-tradable sectors like real estate, and over US$3 billion in annual export potential unrealised, Egypt remains trapped in a low-value ‘farm and quarry’ export model. The paper proposes a three-pillar policy framework—institutional architecture, financial pipelines, and digital trade corridors—to forge the connective tissue required for a sustainable, diversified, and mutually beneficial economic partnership.

Attribution: Ahmed Dawoud and Samriddhi Vij, “The Egypt-GCC Economic Relationship in an Era of Strategic Transformation,” ORF Occasional Paper No. 537, Observer Research Foundation, April 2026.

Introduction

Since the political realignments of 2011, the strategic axis between the Arab Republic of Egypt and the Gulf Cooperation Council (GCC) states has functioned as the geopolitical centre of gravity in the Middle East and North Africa region. This relationship—characterised by unprecedented coordination on security, regional diplomacy, and regime stabilisation—has been reinforced by substantial financial flows, evolving from emergency fiscal support (2013–2016) into an era of sovereign investment and asset acquisition (2017–present).

This transition is unfolding amid a profound geoeconomic transformation. The aggressive national development strategies of GCC states—such as Saudi Vision 2030 and We the UAE 2031—alongside the global energy transition and intensifying United States (US)–China competition over supply chains, are collectively redefining the logic of capital allocation, localisation, and industrial policy across the region.

Yet, beneath this deep strategic alignment lies an economic paradox. Despite historic levels of political convergence and sovereign capital inflows—exemplified by the US$35-billion Ras El Hekma deal—Egyptian–GCC economic integration remains structurally shallow, asymmetric, and inconsistent. While Egypt has successfully attracted billions of dollars in foreign direct investment (FDI), an estimated 76 percent of these inflows remain concentrated in non-tradable sectors such as real estate and construction, limiting their capacity to generate sustainable industrial upgrading or balance-of-payments relief.

A closer examination of the trade relationship reveals the core of this asymmetry. Despite geographical proximity and massive capital injections, Egypt’s exports to the GCC remain trapped in a low-value-added “farm and quarry” model, dominated by primary agricultural and extractive goods. At the same time, GCC investments in Egypt have largely bypassed tradable, productivity-enhancing sectors. As GCC states intensify localisation mandates and industrial nationalisation policies, this structure leaves Egypt increasingly exposed to emerging “localisation traps” and regulatory barriers.

This paper argues that this outcome is not accidental, nor can it be explained by a lack of political will. Rather, it reflects a deeper structural failure: the absence of a functional “missing middle”. This refers to the systemic lack of institutional, financial, and logistical connective tissue required to translate macro-level strategic alliances into micro-level industrial co-creation. In the absence of this middle layer, sovereign capital flows and private sector trade flows remain disconnected, preventing Egyptian Small and Medium Enterprises (SMEs) from integrating into GCC value chains despite strong complementarities.

By departing from generalised narratives of so-called “Arab economic integration,” this analysis provides a granular, corridor-specific diagnosis of the Egypt–GCC economic relationship. It identifies three core structural divergences that collectively constrain integration: a regulatory misalignment exemplified by the growing tension between GCC localisation policies—such as the Saudi Regional Headquarters Program—and Egypt’s export capacities; logistical frictions that sever production hubs from high-potential markets like the UAE; and a persistent investment–trade disconnect, whereby capital is systematically channelled into non-tradable sectors that fail to support industrial upgrading.

By quantifying the cost of these divergences—estimated at over US$3 billion annually in unrealised Egyptian export potential[1]—the paper moves beyond diagnosis towards institutional architecture. It challenges the persistence of an outdated model of comparative advantage based on raw material exchange and factor substitution, proposing instead a transition towards industrial co-creation, in which Gulf capital, Egyptian industrial capacity, and shared value-chain governance are strategically aligned.

To rigorously diagnose this failure, the study adopts a targeted analytical scope. While the Egypt–GCC relationship encompasses vital flows of labour migration, remittances, tourism, and services, this analysis deliberately focuses on merchandise trade and industrial investment. This scoping reflects the analytical premise that although labour and remittances have historically functioned as stabilising mechanisms, they do not provide a pathway to sustainable structural transformation. The bottleneck lies specifically within the trade–investment nexus of the industrial sector, which requires distinct policy interventions.

The paper is organised in three sections. Section 1 establishes the geoeconomic context, tracing the evolution from “geopolitical rent” to conditional capital and mapping the convergences and divergences between Egypt’s development trajectory and GCC national strategies. Section 2 deconstructs the architecture of trade, introducing country-specific archetypes—from Saudi Arabia’s “Industrial Wall” to the UAE’s “Re-export Hub” model—to explain why integration fails differently across partners. Finally, Section 3 synthesises these findings into a policy framework, outlining a three-pillar architecture designed to construct the “missing middle” and unlock the latent industrial potential of the Egypt–GCC economic corridor.

I. Geoeconomic Context: Structural Divergence in an Era of Strategic Alignment

To understand the paradox of deep strategic alignment alongside shallow industrial integration between Egypt and the GCC states, it is necessary to examine the structural evolution of Egypt’s political economy since 2011.[a] The current phase represents a transition from a stabilisation-based relationship—anchored in geopolitical considerations—to an asset-based paradigm governed by commercial logic. This transition has exposed long-standing structural weaknesses within Egypt’s industrial base that constrain its capacity to function as a credible partner in regional value chains.

1.1. From “Geopolitical Rent” to Conditional Capital

In the aftermath of the 2011 political transitions, Egypt’s economic relationship with key GCC partners was shaped by a logic of “geopolitical rent.” Severe capital flight, declining foreign reserves, and macroeconomic instability necessitated large-scale external support. Between 2013 and 2022, Egypt received an estimated US$92–114 billion in financial assistance from Saudi Arabia, the United Arab Emirates (UAE), and Kuwait, primarily in the form of central bank deposits, grants, and fuel support. While this inflow helped avert macro-fiscal collapse, it also contributed to an “aid-for-reform” trap, whereby the availability of external liquidity reduced the urgency of implementing politically costly structural reforms.

This model reached its limits in 2023. Amid tightening global financial conditions and rising domestic investment needs within the Gulf, unconditional support was formally curtailed. This shift was articulated during the World Economic Forum in Davos in January 2023, when policymakers from the Gulf region signaled that future engagement would be guided by investment discipline and return-on-investment (ROI) considerations.[2] Consequently, Egypt–GCC economic relations have transitioned towards equity-based participation and asset acquisition, exemplified by large-scale transactions such as the Ras El Hekma development deal—a US$35-billion agreement between Egypt and Abu Dhabi’s ADQ sovereign wealth fund for the development of a next-generation city on Egypt’s Mediterranean coast.[3] Under this new paradigm, capital inflows are no longer politically agnostic; they are increasingly contingent on commercial viability and institutional reform.

1.2. The Investment–Industrial Disconnect

Despite a headline surge in FDI, the sectoral allocation of capital reveals a persistent misalignment between investment inflows and productive capacity. In fiscal year 2023/2024, Egypt recorded a historic US$46.1 billion in net FDI inflows. However, data from the General Authority for Investment indicate that approximately 76 percent of this capital was concentrated in non-tradable sectors, particularly construction and real estate, driven largely by land-based mega-projects.[4]

In contrast, the manufacturing sector—which is central to export diversification and regional supply-chain integration—attracted less than 3 percent of total FDI.[5] This pattern suggests that FDI is functioning primarily as a store of value rather than as a catalyst for industrial upgrading. The resulting dynamic resembles a “Dutch Disease” effect, in which capital gravitates toward high-rent, non-tradable activities while the tradable sector remains structurally undercapitalised. As a result, record investment figures have not translated into a commensurate expansion of export capacity or technological upgrading, limiting Egypt’s ability to integrate into higher-value GCC production networks.

1.3. Structural Determinants of Industrial Fragility: The “Missing Middle”

At the core of Egypt’s limited industrial integration lies the “missing middle” phenomenon. Unlike peer economies such as Türkiye—where medium-sized enterprises (20–100 employees) play a central role in driving export complexity—Egypt’s industrial structure is characterised by a pronounced dualism. A vast number of low-productivity micro-enterprises coexist with a small number of large, often state-affiliated conglomerates, while medium-sized firms account for a disproportionately small share of employment and output.

Two interrelated structural factors reinforce this imbalance. First, the expansion of state-owned enterprises and military-affiliated entities into civilian economic sectors has contributed to distortions in market competition. These entities often operate under differentiated regulatory and cost structures, which can discourage private investment and raise entry barriers. The cement sector provides a salient example: the entry of large state-owned capacity in 2018 generated excess supply, contributing to price compression and the exit of several private producers.

Second, Egypt’s weak integration into global value chains constrains industrial upgrading. High-technology products account for only an estimated 4–8 percent of total manufacturing exports, reflecting limited technological depth and skills absorption. This structural profile positions Egypt predominantly as a supplier of primary commodities and low-value-added goods, while GCC economies increasingly source advanced industrial inputs from East Asia and other technologically advanced regions.

In summary, the Egypt–GCC economic corridor is situated between two temporal logics: a political alliance that has matured into a strategic partnership, and an Egyptian industrial structure that remains insufficiently equipped to meet the commercial demands of that partnership. Without targeted reforms to address capital allocation, competitive neutrality, and firm-level scaling, the shift from geopolitical support to investment-led engagement risks reinforcing existing asymmetries rather than generating meaningful industrial co-creation.

1.4. Strategic Determinants: National Visions, Localisation, and Global Shifts

The transformation of the Egypt–GCC economic relationship is being driven by a synchronised wave of national development strategies aimed at post-hydrocarbon diversification. While Egypt’s Vision 2030 and State Ownership Policy Document prioritise fiscal stabilisation through FDI attraction, GCC frameworks—most notably Saudi Vision 2030, We the UAE 2031, Oman Vision 2040, and Qatar National Vision 2030—are backed by capital surpluses and increasingly enforce industrial localisation as a regulatory objective. This divergence in strategic intent has produced a complex convergence–divergence dynamic, reshaping the contours of regional economic integration.

1.4.1 Convergences: Pathways for Industrial Co-Creation

Despite growing competitive pressures, several niche areas continue to offer scope for non-zero-sum integration where factor endowments are complementary rather than duplicative.

Green Hydrogen and Renewable Energy:

Renewable energy represents the most significant axis of strategic alignment. Saudi Arabia (through the NEOM Green Hydrogen Project), Oman (via large-scale targets under Vision 2040), and Egypt are leveraging high solar and wind endowments to access European energy markets.[6] This has enabled cross-border integration rather than pure competition. Notably, Saudi Arabia’s ACWA Power has committed substantial investment in green ammonia production within Egypt’s Suez Canal Economic Zone (SCZONE), effectively embedding Egyptian geography into a broader Gulf-led energy value chain.

Food Security and Agribusiness:

Qatar’s Third National Development Strategy (2024–2030) and parallel food security initiatives in the UAE rely on outward investment rather than domestic self-sufficiency. Given severe climatic constraints, Gulf states increasingly view Egypt as a strategic agricultural reservoir. Investments by firms such as Al Dahra and large-scale projects in sugar and grain production illustrate a form of vertical integration that links Gulf capital with Egyptian land and labour, sustaining a durable corridor of complementarity.[7]

Selective Industrial Synergies:

Bahrain offers a distinct model of cooperation shaped by tighter fiscal constraints. The potential integration between Aluminium Bahrain (Alba) and Egypt’s metallurgical and refining capacity illustrates how specific supply-chain gaps—rather than broad industrial overlap—can generate mutually beneficial value chains without triggering localisation-driven competition.[8]

1.4.2 Divergences: The Emergence of the “Localisation Trap”

Alongside these convergences, the dominant regional trend is a shift from donor-based engagement toward competitive industrial policy. This transition has given rise to what may be described as a “localisation trap”, whereby regulatory frameworks in GCC states increasingly incentivise firms to relocate production and capital locally rather than exporting from Egypt.

Saudi Arabia’s Procurement and Headquarters Mandates:

Saudi Arabia’s Regional Headquarters (RHQ) Program and the enforcement mechanisms of the Local Content and Government Procurement Authority (LCGPA) exemplify this shift. Mandatory local content thresholds—reaching approximately 40–42 percent in sectors such as electrical infrastructure—function as de facto non-tariff barriers. As a result, Egyptian conglomerates have been compelled to establish manufacturing facilities within the Kingdom to retain market access, redirecting fixed capital formation away from Egypt’s domestic industrial base.[9]

Technological Divergence in the UAE:

The UAE’s Operation 300bn strategy prioritises advanced Industry 4.0 sectors, including aerospace, advanced pharmaceuticals, and clean technologies. This focus exceeds the current technological depth of Egyptian manufacturing, creating a widening capability gap. The UAE’s In-Country Value (ICV) framework further reinforces this divergence by structurally favoring domestically produced inputs in public procurement, disadvantaging imported Egyptian goods.

Logistics and Port Competition:

Regional competition is also intensifying in logistics and transport. Oman’s Duqm port and green hydrogen hub, alongside Kuwait’s Mubarak Al-Kabeer Port under New Kuwait 2035, are positioning themselves as alternative transshipment and bunkering nodes. These initiatives increasingly compete with Egypt’s SCZONE and Ain Sokhna, raising the risk of overcapacity and fragmenting regional logistics flows.[10]

1.4.3 Global Strategic Context: Corridor Competition and Multi-Alignment

These regional dynamics are further shaped by global geopolitical shifts. The proposed India–Middle East–Europe Economic Corridor (IMEC), backed by the United States and key Gulf states, presents a long-term strategic challenge to the Suez Canal by offering alternative ship-to-rail connectivity. While GCC capitals frame IMEC as a diversification and resilience tool, Egypt remains cautious, seeking complementarities that preserve the canal’s centrality.[11]

Simultaneously, deeper GCC engagement with China through the Belt and Road Initiative (BRI) and BRICS platforms reinforces a multi-alignment strategy that heightens competition among regional logistics hubs. In this context, Egypt faces mounting pressure to upgrade its industrial and logistical offerings to remain relevant within both Western- and China-linked trade architectures.[12]

Synthesis:

These trends indicate that the era of automatic Arab economic integration is receding. Strategic alignment at the political level now coexists with regulatory and industrial competition at the economic level. Without targeted reforms to enhance technological capability, competitive neutrality, and export sophistication, Egypt risks being drawn into a localisation-driven equilibrium in which regional integration increasingly occurs through capital relocation rather than cross-border industrial co-creation.

II. Institutional Frameworks, Trade Architecture, and Comparative Analysis

2.1. The Institutional Deficit: Bilateralism Over Multilateralism

To properly situate the trade patterns and country-specific divergences analysed in Sections 2.2 and 2.3, it is first necessary to examine the institutional architecture governing Egypt–GCC economic relations. Despite the scale and strategic importance of these ties, the relationship remains weakly institutionalised at the bloc level and overwhelmingly driven by bilateral arrangements between Cairo and individual Gulf capitals.

Unlike Egypt’s economic relationship with the European Union (EU)—anchored in a legally binding Association Agreement that governs tariffs, standards, competition policy, and dispute resolution—Egypt’s engagement with the GCC operates through fragmented and shallow multilateral mechanisms. In formal terms, trade is governed by the Greater Arab Free Trade Area (GAFTA), which entered into full force in 2005 and successfully eliminated most tariff barriers on goods. However, GAFTA has proven largely ineffective in addressing non-tariff barriers (NTBs), harmonising technical standards, or constraining national industrial policies. As a result, it has failed to function as a platform for meaningful production integration or value-chain coordination.

Efforts to deepen collective economic cooperation have been sporadic and largely symbolic. In the aftermath of the 2011 regional uprisings, the GCC floated a proposal for a form of confederal expansion to include Jordan and Morocco, with Egypt positioned as a strategic partner. This initiative, however, stalled quickly and did not translate into binding economic arrangements. Over the past decade, the Egypt–GCC Strategic Dialogue—launched in 2011 and periodically revitalised—has served primarily as a forum for political and security coordination rather than a vehicle for economic rule-making. Issues central to trade integration, such as local content rules, industrial subsidies, or procurement policies, remain firmly outside its scope.

In practice, the relationship is structured around a pronounced “hub-and-spoke” model. Major investment decisions, trade concessions, and industrial partnerships are negotiated bilaterally between Egypt and individual GCC states—most notably Saudi Arabia, the UAE, and Qatar—rather than through the GCC Secretariat or a unified institutional framework. This preference for bilateralism allows Gulf states to fully leverage their national development visions, fiscal capacities, and regulatory autonomy. For Egypt, however, it produces an asymmetric bargaining environment in which access to Gulf markets is contingent on compliance with country-specific rules rather than predictable, bloc-wide norms.

This institutional deficit has direct implications for trade outcomes. In the absence of binding multilateral constraints on industrial policy and non-tariff barriers, economic integration has not evolved towards diversification or intra-industry trade. Instead, it has crystallised into a narrow and repetitive exchange structure, where national strategies—rather than collective rules—shape commercial flows. The following section demonstrates how this institutional configuration translates into a standardised trade basket characterised by low-complexity Egyptian exports and strategic, high-value imports from the GCC, setting the foundation for the asymmetries and country-specific divergences analysed thereafter.

2.2. General Patterns: The Standardised Trade Basket

An examination of Egypt’s bilateral trade matrices with GCC states reveals a strikingly stable and homogeneous structure across destinations. Despite differences in market size and political relations, Egypt’s trade profile with Saudi Arabia, the UAE, Kuwait, and Qatar exhibits a high degree of standardisation, reflecting a factor-driven rather than efficiency-driven pattern of exchange. This structural uniformity points to a persistent division of labour in which Egypt supplies low-complexity goods, while the GCC provides energy and industrial inputs.[13]

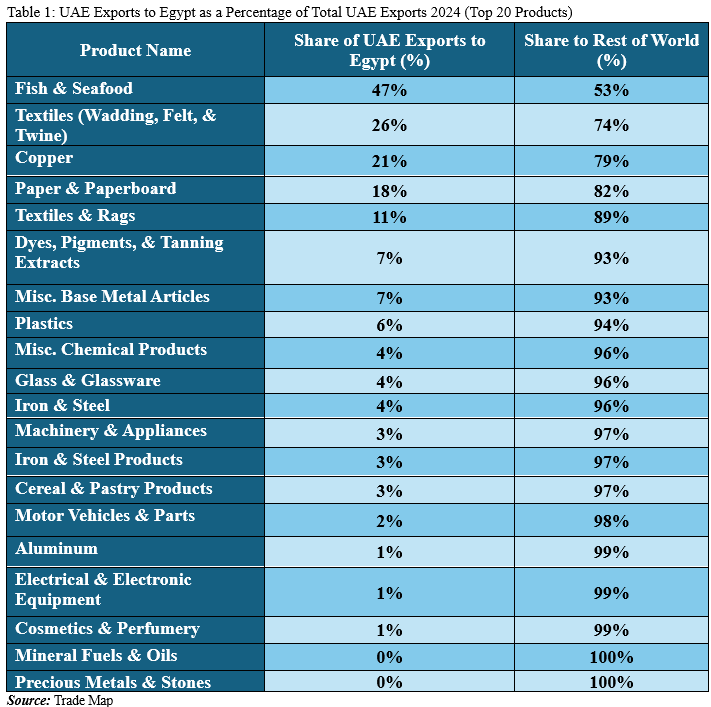

2.2.1. The Export Profile: The “Farm and Quarry” Model

Egypt’s export basket to the GCC is dominated by primary commodities and semi-processed materials, a configuration that can be described as a “farm and quarry” model. Exports are largely derived from natural endowments rather than industrial upgrading, and the composition remains broadly consistent across partner states.

The “Farm” Component (Agribusiness):

Agricultural products (HS Codes 07 and 08) constitute the most consistent non-oil export category. Fresh fruits and vegetables account for a substantial share of Egyptian exports across the bloc. For instance, edible vegetables alone account for 16 percent of Saudi Arabia’s total imports from Egypt, while in the UAE, processed foods represent 7 percent of the export basket.[b] This trade is driven primarily by the GCC’s structural food security deficit rather than by Egypt’s competitive advantage in high-value agribusiness.

The “Quarry” Component (Raw and Semi-Finished Materials):

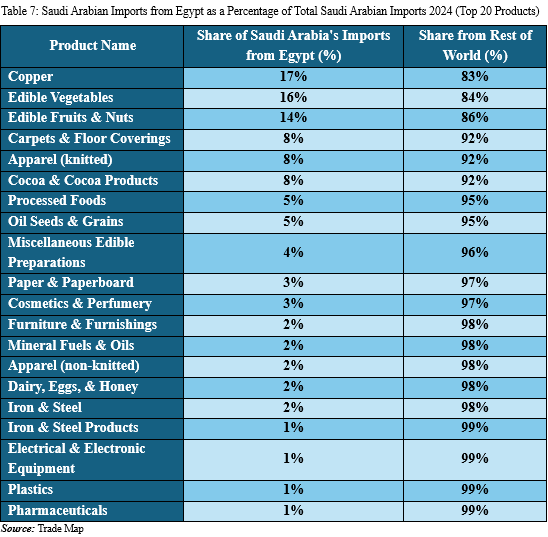

The second dominant export category comprises mineral products and construction inputs (HS Codes 25 and 74). These goods feed the Gulf’s infrastructure and real estate megaprojects but are typically exported in raw or semi-finished form. A prime example is the Saudi market, where refined copper exports capture a 17-percent share of the inbound trade flow from Egypt.[c] The limited presence of downstream processing reflects Egypt’s persistent “missing middle,” constraining its ability to move up regional value chains.

Crucially, complex manufactured goods—such as machinery, electronics, or automotive components—remain statistically insignificant in Egypt’s export basket to the GCC. This is starkly illustrated by the UAE market, where Egypt holds a 0-percent market share in the multi-billion-dollar “miscellaneous manufactured articles” category.[d] This confirms the absence of meaningful industrial integration despite decades of trade engagement.

Table 2.1: Standardised Export Basket: Egypt’s Market Share in Key ‘Farm & Quarry’ Sectors (2024)

| Partner Country | ‘Farm’ Component (Agriculture Share) | ‘Quarry’ Component (Materials Share) |

| Saudi Arabia | 16% (Edible Vegetables) | 14% (Edible Fruits) | 17% (Refined Copper) | 8% (Apparel & Textiles) |

| UAE | 7% (Processed Foods) | 6% (Edible Vegetables) | 3% (Precious Metals/Stones) | 2% (Apparel) |

| Kuwait | 9% (Edible Vegetables) | 7% (Edible Fruits) | 31% (Carpets & Floor Coverings) | 5% (Chemicals) |

| Qatar | 10% (Edible Vegetables) | 9% (Edible Fruits) | 6% (Cocoa Preps) | 5% (Furniture & Bedding) |

| Oman | 22% (Edible Fruits) | 18% (Edible Vegetables) | 71% (Raw Cotton) | 38% (Tobacco) |

| Bahrain | 15% (Edible Fruits) | 14% (Edible Vegetables) | 23% (Tobacco) | 18% (Printed Matter) |

Source: Trade Map[14]

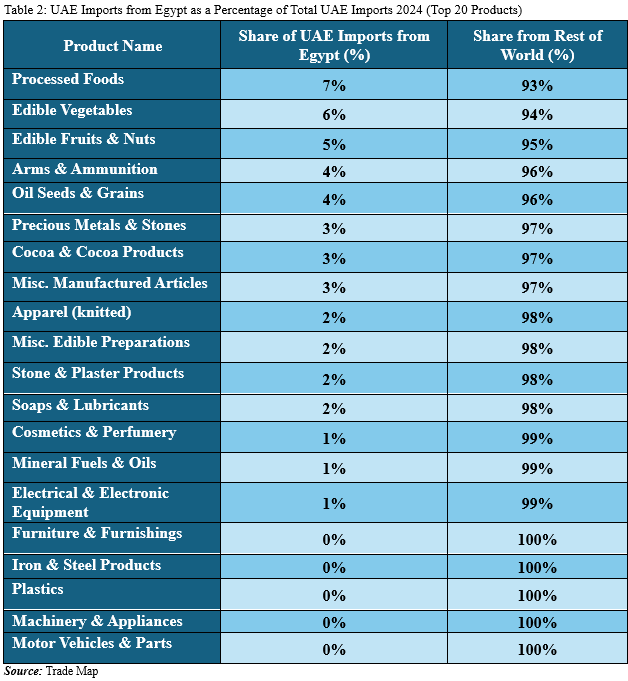

2.2.2. The Import Profile: Energy and Petrochemical Dependence

In contrast, Egypt’s import basket from the GCC is equally standardised but strategically concentrated. Imports are anchored in the energy value chain, reinforcing a structural dependence on Gulf hydrocarbons and petrochemical derivatives.

Hydrocarbon Dominance:

Mineral fuels and energy-intensive inputs account for the overwhelming majority of imports. While direct fuel shipments are often managed through strategic channels, the reliance is evident in related sectors. For instance, “Inorganic Chemicals”—a key energy-derivative sector—account for 6 percent of Saudi Arabia’s total exports to Egypt, ranking among the top industrial categories. This volume renders the trade balance highly sensitive to global energy price fluctuations, maintaining a deficit that non-oil exports struggle to cover.

Petrochemical Inputs:

Plastics and polymer derivatives (HS Code 39) represent the second-largest import category, serving as essential feedstock for Egypt’s domestic industrial base. For example, “Plastics and articles thereof” constitute 7 percent of Saudi Arabia’s total global exports that are directed to Egypt, highlighting the heavy reliance on Gulf inputs for Egyptian manufacturing[e]. Similarly, in the UAE–Egypt channel, plastics represent a steady 6 percent of the export flow, confirming a dependency loop where Egypt imports intermediate goods to manufacture finished consumer products.[f]

Table 2.2: The Industrial Disconnect: Egypt’s Absence in High-Value GCC Import Markets

| Target Market | High-Value Import Category | Total GCC Import Demand (Approx.) | Egypt’s Market Share |

| Saudi Arabia | Machinery & Mechanical Appliances | ~$9 Billion+ | ~0% |

| UAE | Miscellaneous Manufactured Articles | $15.9 Billion | 0% |

| Kuwait | Optical & Precision Instruments | $811 Million | < 0.1% |

| Qatar | Electrical Machinery & Equipment | ~$6 Billion | 0% |

| Oman | Motor Vehicles & Parts | $3 Billion | ~0% |

| Bahrain | Machinery & Appliances | High Demand | 0% |

Source: Trade Map14

2.2.3. The Structural Trade Deficit

The interaction between low-value, factor-based exports and high-value, strategically essential imports produces a chronic structural trade deficit between Egypt and the GCC bloc, aside from episodic anomalies such as gold re-exports. This imbalance is not merely a function of trade volumes but reflects an underlying terms-of-trade inequality driven by a persistent complexity gap.

Egypt must export large quantities of agricultural produce and raw materials to offset the cost of energy and petrochemical imports, a gap that currency depreciation has historically failed to close. Absent a shift toward higher-complexity manufacturing and deeper integration into regional value chains, the standardised nature of this trade basket is likely to perpetuate asymmetrical outcomes despite sustained political alignment.

Table 2.3: Generalised Structure of Egypt–GCC Trade Patterns (2024)

| Partner Country | ’Farm’ Component (Top Agribusiness Exports) | ’Quarry’ Component (Top Material Exports) | ‘Import Trap’ (Key Imports from GCC) | Structural Logic |

| Saudi Arabia | Vegetables & Fruits (~16% market share) | Refined Copper

(~17% market share) |

Petroleum Products & Plastics

(Industrial inputs) |

“Industrial Wall”

(Food-for-fuel exchange under localisation constraints) |

| United Arab Emirates | Processed Foods

(~7% market share) |

Precious Metals

(~3% market share) |

Electronics & Refined Fuels

(Re-export intensive) |

“Tech Arbitrage”

(Transit and value-chain upgrading hub) |

| Kuwait | Vegetables & Fruits

(~9% market share) |

Carpets & Flooring

(~31% market share) |

Diesel & Oil Products

(Energy inputs) |

“Labour Substitute”

(Goods–remittances linkage) |

| Qatar | Vegetables & Fruits

(~10% market share) |

Cocoa & Furniture

(~6% market share) |

Chemicals & Plastics

(Gas derivatives) |

“Food Security Alignment”

(Strategic agribusiness dependence) |

| Oman | Edible Fruits

(~22% market share) |

Raw Cotton

(~71% market share) |

Iron Ores & Metals

(Raw materials) |

“Factor-Driven Exchange”

(Limited industrial depth) |

| Bahrain | Edible Fruits

(~15% market share) |

Tobacco & Printed Products

(~23% market share) |

Aluminum & Metal Inputs

(Manufacturing integration) |

“Niche Complementarity”

(Sector-specific value chains) |

Source: Trade Map14

2.3. Strategic Divergences: Country-Specific Archetypes of Engagement within the GCC

While the aggregate data confirms the dominance of a standardised Egyptian export basket centred on agribusiness and basic materials, bilateral trade relationships with GCC partners are far from homogeneous. Beneath this apparent uniformity lie distinct country-specific mechanisms shaped by regulatory regimes, logistical roles, demographic structures, and strategic state objectives. This section identifies six archetypal modes of engagement that explain how similar trade baskets generate divergent economic outcomes across the bloc.

2.3.1. Saudi Arabia: The ‘Industrial Wall’ (Regulatory Divergence)

Saudi Arabia represents the most structurally complex and contested market for Egyptian exports. Unlike other GCC partners where trade remains largely consumption-driven, the Saudi market exhibits absorption capacity for intermediate industrial goods. Egypt maintains a notable market share in refined copper and related articles (approximately 17 percent), as well as textile floor coverings, indicating partial integration into Saudi construction and industrial supply chains.[g]

However, this integration is increasingly constrained by regulatory transformation. The Local Content and Government Procurement Authority (LCGPA) and its Mandatory List requirements have introduced localisation thresholds (e.g., 40 percent local content in transmission and infrastructure projects). As a result, the relationship is shifting from complementary trade toward regulatory competition. Egyptian firms are now incentivised to relocate capital and production to Saudi Arabia rather than export from Egypt, reinforcing a vertically asymmetric structure in which Egypt exports semi-finished inputs while importing high-value energy derivatives and polymers.

2.3.2. United Arab Emirates: The ‘Re-export Hub’ (Logistical Divergence)

Trade with the UAE is statistically inflated and structurally distinct. High bilateral trade values are driven disproportionately by pearls, precious stones, and metals (notably gold), reflecting a transit-oriented relationship rather than deep industrial integration.

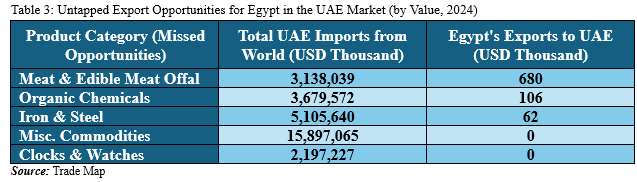

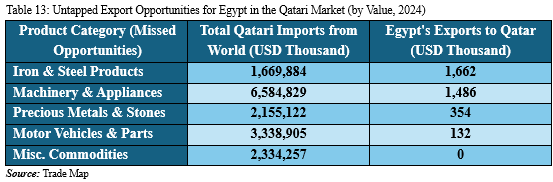

The UAE functions as a logistical hub mediating triangular trade. This creates a “tech arbitrage” dynamic where value is captured through logistics rather than manufacturing. This disconnect is starkly evident in the unrealised potential data: while the UAE imports a colossal US$15.8 billion in “Miscellaneous Commodities” globally, Egypt captures a zero-percent share of this market.[h] Similarly, Egypt holds a zero-percent market share in the high-value “Clocks and Watches” segment, highlighting the failure to penetrate core Emirati luxury and industrial sectors.³

2.3.3. Qatar: The ‘Procurement Nexus’ (Strategic Divergence)

Trade with Qatar follows a distinct state-led logic. The post-2017 expansion in Egyptian agricultural exports is closely aligned with Qatar’s food security strategy rather than private-sector market dynamics. Data shows that “Edible Vegetables” and “Edible Fruits” now account for 10 percent and 9 percent of Qatar’s total imports from Egypt, respectively.[i]

This relationship operates as a procurement corridor insulated from broader industrial competition, anchored in government-to-government coordination through entities such as Hassad Food. While this model provides stability, it remains narrow in scope, limited to specific food security mandates.

2.3.4. Kuwait: The ‘Factor Substitution’ Model (Demographic Divergence)

Kuwait represents a legacy model in which merchandise trade is structurally weak relative to the size of the economy. Egypt’s high market shares in “Edible Vegetables” and “Edible Fruits” accounting for 9 percent and 7 percent of imports, respectively, are closely correlated with household demand linked to the Egyptian expatriate community.[j]

This pattern suggests that trade flows are shaped less by strategic business-to-business integration and more by demographic-driven consumption. The broader economic relationship is characterised by factor substitution: Egypt exports labour, while Kuwait exports capital in the form of remittances and financial inflows. As Kuwait accelerates labor nationalisation policies, this model faces increasing fragility due to the absence of a robust industrial trade backbone.

2.3.5. Oman: The ‘Factor-Driven Exchange’ and Emerging Logistics Rivalry

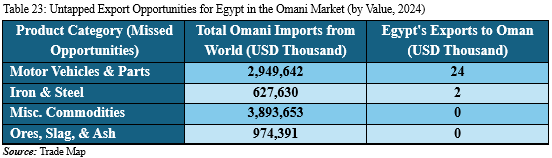

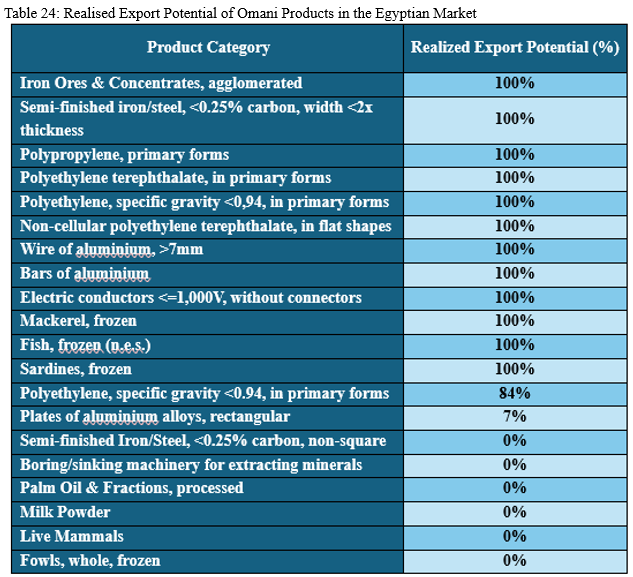

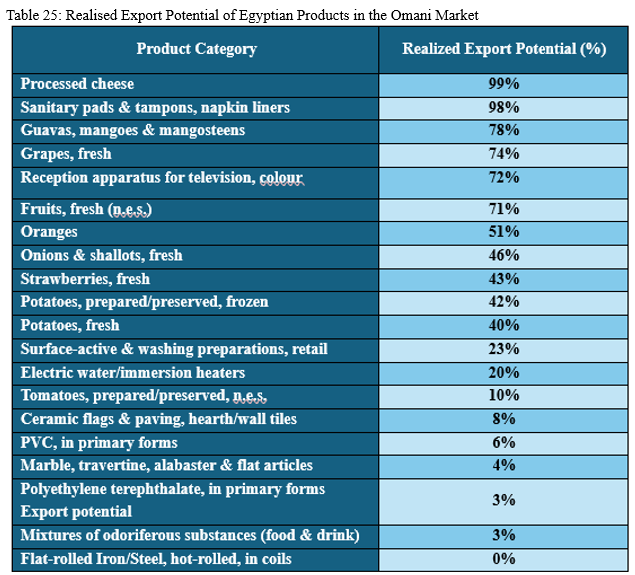

Trade with Oman is characterised by a highly concentrated factor-based exchange. Egypt holds a substantial market share in specific niches, such as “Tobacco Products”, which account for 38 percent of Oman’s imports from Egypt, and “Edible Fruits” at 22 percent.[k] This pattern highlights a persistent value-added gap, where trade is driven by raw or semi-processed goods.

Looking forward, the relationship is evolving into a latent logistics rivalry. Oman’s Vision 2040, centered on the Port of Duqm and green hydrogen infrastructure, positions the country as a potential competitor to Egypt’s Suez Canal Economic Zone. Unlike regulatory barriers in Saudi Arabia, the Omani divergence is infrastructure-driven, with both countries developing parallel capabilities to serve overlapping global trade routes.

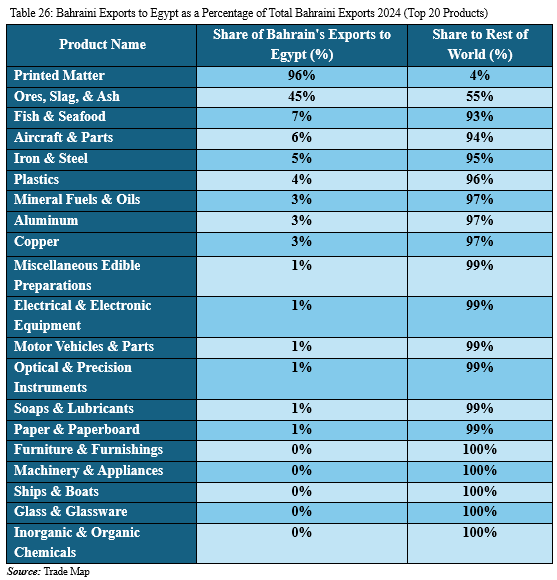

2.3.6. Bahrain: The ‘Niche Complementarity’ Model (Fiscal Divergence)

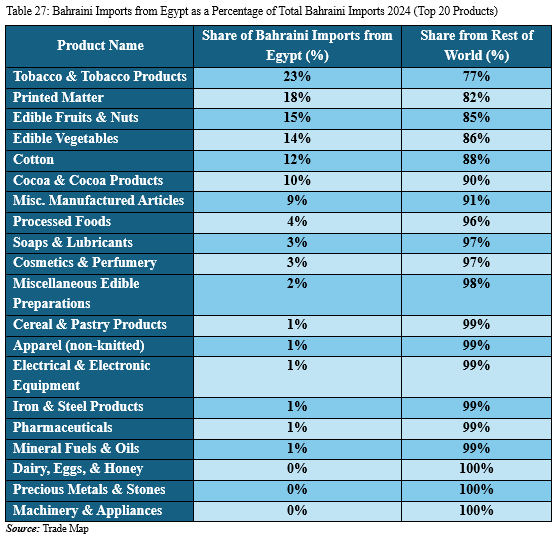

Bahrain’s trade relationship with Egypt is constrained by scale and fiscal capacity. Unlike larger GCC economies, trade is concentrated in narrow industrial verticals. Egypt holds a significant 23-percent share in “Tobacco Products” and 18 percent in “Printed Matter”, reflecting a targeted value-chain linkage.[l]

This results in a pattern of niche complementarity rather than comprehensive economic integration. While structurally limited in aggregate impact, these targeted value-chain linkages exhibit higher sectoral synergy than broader but shallower trade relationships elsewhere in the bloc.

2.4. The Cost of Misalignment: Unrealised Export Potential

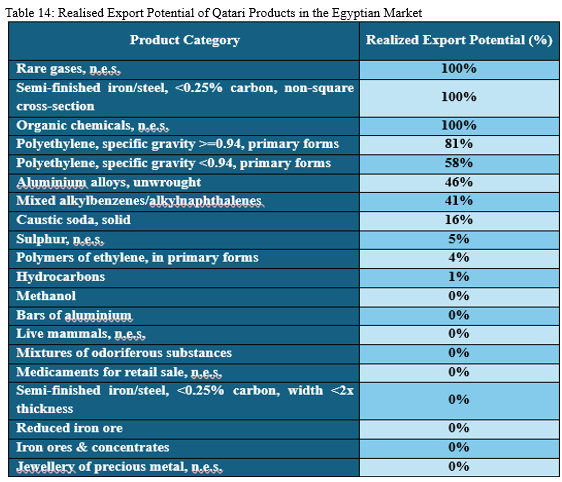

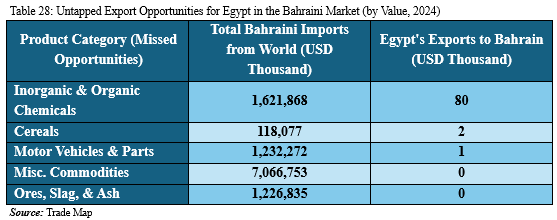

The structural disconnects analysed above—whether regulatory (Saudi Arabia), logistical (UAE), or demographic (Kuwait)—have a quantifiable economic cost. Data from the International Trade Centre (ITC) reveals massive “unrealised export potential” for Egypt across the GCC. This gap represents the difference between what Egypt could theoretically export based on its supply capacity and GCC demand, versus what it actually exports.14

Table 2.4: Unrealised Export Potential Matrix (2024 Estimates)

| Target Market | Actual Exports (Approx.) | Unrealised Potential (Lost Opportunity) | Top Sector with Potential |

| Saudi Arabia | ~$2.7 Billion | $1.4 Billion | Processed Foods & Cables |

| UAE | ~$2.2 Billion | $1.1 Billion | Agricultural Produce & Textiles |

| Kuwait | ~$480 Million | $350 Million | Fresh Produce & Carpets |

| Qatar | ~$100 Million | $29 Million | Fruits & Vegetables |

| Oman | ~$180 Million | $110 Million | Citrus & Building Materials |

| Bahrain | ~$50 Million | $40 Million | FMCGs & Foodstuffs |

Source: Trade Map14

The structural divergences identified in the matrix in Table 2.4 have a quantifiable economic cost. Aggregate data indicates over US$3 billion in annual unrealised export potential for Egypt across the GCC. This table represents the tangible price of the “missing middle” and the “localisation trap”. Crucially, the majority of this untapped potential lies not in hypothetical high-tech industries, but within Egypt’s existing productive capacity—specifically in agribusiness, textiles, and building materials. The failure to capture this value is driven less by a lack of demand and more by the specific non-tariff barriers, logistical frictions, and regulatory misalignments diagnosed in this section. Consequently, bridging this gap requires moving beyond traditional trade diplomacy toward the targeted institutional and industrial interventions proposed in the following framework.

III. From Analysis to Architecture: A Policy Framework for Forging the ‘Missing Middle’

3.1. The Strategic Imperative: Beyond Optimisation to Co-Creation

The preceding analysis confirms that the Egypt-GCC relationship suffers from a critical failure of architecture, not intention. The quantifiable cost of this failure—over US$3 billion in unrealised export potential identified in Section 2.4—is driven not by a lack of demand, but by a structural void. The core pathology identified throughout this study is the “missing middle”—the absence of the essential connective tissue required to translate macro-level strategic alliances into micro-level commercial reality. This “middle” consists of the institutional, financial, and logistical ecosystems that allow SMEs to integrate into cross-border value chains.

The failure to construct this middle ground is the direct legacy of an obsolete division of labour—with the Gulf as the industrial engine and Egypt as the agricultural heartland—that is no longer compatible with the era of co-creation. Therefore, the challenge for the next decade is not to generate more political will nor allocate more top-level sovereign capital, but to deliberately and strategically architect this “missing middle”.

Consequently, any policy intervention aimed merely at optimising the existing trade framework is destined to fail. The strategic imperative is to engineer a paradigm shift towards “Industrial Co-Creation”. The following framework proposes a three-pillar architecture designed to forge these missing links.

3.2. Pillar I: The Institutional Architecture: Forging the Missing Links

The critical failure of the “missing middle” is, at its core, an institutional void. The current landscape lacks the executive capacity and operational focus to perform the granular work of true economic integration. The solution lies in launching a series of targeted, agile, and results-oriented initiatives designed to forge the missing institutional links.

3.2.1. Sector-Specific Market-Creation Taskforces

The first step should be to launch sector-specific “Market-Creation Taskforces”. These would be temporary, high-impact teams focused on priority industries like construction materials, pharmaceuticals, or food processing. A KSA-Egypt Construction Supply Chain Taskforce, for example, would be composed of procurement executives from Saudi giga-projects and technical experts from leading Egyptian materials firms. Their mandate would be highly specific and time-bound: within six to nine months, identify a concrete portfolio of supply chain gaps and produce a bankable roadmap for a pre-vetted group of Egyptian suppliers to fill them. This shifts the dynamic from passively seeking market access to actively engineering market creation. These taskforces would function as strategic “advance teams”, doing the on-the-ground due diligence and technical alignment needed to connect major GCC demand directly to Egyptian industrial capacity.

3.2.2. A Curated GCC-Egypt Industrial Opportunity Platform

To overcome the informational asymmetries that prevent SMEs from connecting with large-scale projects, the second initiative is to build a curated, digital B2B platform. This will not be a simple business directory but a secure, transactional ecosystem. On the GCC side, major corporations and projects would post specific, long-term, high-volume procurement needs. On the Egyptian side, only industrial firms that have passed a rigorous, jointly-agreed-upon audit for capacity, quality control and financial stability would be listed. This platform would serve as a trusted digital intermediary, de-risking the discovery and engagement process for both parties. It would provide the informational certainty that the current market lacks, allowing a procurement manager in Dubai to confidently identify and engage a certified specialty chemical manufacturer in Egypt, knowing they have already met a verified standard.

3.2.3. A Bilateral Regulatory Coherence Programme

Non-tariff barriers, particularly divergent standards and certifications, remain a critical hurdle. Rather than attempting a monumental, top-down harmonisation of all regulations, a more pragmatic approach is a Bilateral Regulatory Coherence Programme focused on mutual recognition in priority sectors. This programme would establish permanent working groups between counterpart national standards bodies. Their task would not be to rewrite entire rulebooks, but to establish regulatory green lanes. For products within a priority sector identified by a Market-Creation Taskforce, this programme would ensure that a product certified as safe and high-quality in Cairo is automatically accepted as such in Riyadh or Kuwait City, and vice versa. This surgical approach eliminates specific, critical barriers to trade without the immense effort of full regulatory alignment, creating the predictability necessary for building resilient supply chains.

3.3. Pillar II: The Financial Architecture: Building the Capital Pipelines

The institutional void is mirrored by a critical financial disconnect. While GCC sovereign capital is abundant and has been deployed at scale in Egyptian megaprojects and acquisitions, these headline figures mask a profound market failure. Capital flows move through a few large, well-established channels, while the vast industrial and SME ecosystem, the very engine required for diversified co-creation, remains capital-starved. The financial “missing middle” is a problem as sovereign capital at the top is immense, but the pipelines to deliver it to the productive base are narrow.

3.3.1. Capital Aggregation through Co-Investment Platforms

There is a fundamental scale mismatch. GCC sovereign investors have a large capital appetite, while Egyptian industrial SMEs require multiple small investments. The transaction costs and perceived risks of managing dozens of small, individual deals are prohibitive for large institutional investors. The solution is to launch specialised Co-Investment Platforms led by trusted financial intermediaries, such as established regional investment banks or private equity firms with a deep footprint in Egypt. These lead partners would perform the granular due diligence to identify and bundle a portfolio of 10-15 high-potential, pre-vetted Egyptian industrial firms. This curated portfolio would then be offered as a single, investable vehicle to GCC sovereign wealth funds and large family offices. To catalyse the creation of these platforms, the government can offer a “first-loss” guarantee, absorbing a pre-defined initial percentage (e.g., 10-15 percent) of any potential losses on the portfolio. This powerful de-risking mechanism incentivises the lead partner and attracts end-investors. This can be coupled with targeted tax incentives, such as a reduced capital gains tax for returns generated through these certified platforms.

3.3.2. Strategic Capital through Anchor-Led Supply Chain Funds

Financial capital alone is not enough. To be truly effective, it must be paired with strategic direction and guaranteed market access. Many Egyptian firms lack not only the funds to expand, but also the certainty of offtake required to justify the investment. This initiative involves major GCC industrial champions anchoring smaller, dedicated Supply Chain Development Funds. The anchor corporation’s fund would make strategic equity investments in its own potential Egyptian suppliers. For example, a GCC construction giant could invest directly into several Egyptian manufacturers of high-grade steel, glass and aluminum. The Egyptian firm receives strategic capital, funds that come with a guaranteed customer. The GCC anchor secures a resilient, cost-effective and geographically proximate supply chain. This creates a powerful, self-reinforcing ecosystem where investment directly fuels trade. The government’s role here will be of strategic alignment. The government can offer a “Golden License” package specifically for the Egyptian SMEs receiving these funds. This would grant them an expedited approval for permits, factory expansions and import licenses for machinery. This directly enhances the investment’s ROI and operational speed, making the proposition significantly more attractive to the GCC anchor.

3.3.3. Risk Mitigation through Joint Trade Finance & Hedging Facility

Currency volatility and access to affordable trade finance are significant operational barriers that deter both equity investment and cross-border trade, particularly for SMEs. The final piece of the financial architecture is a crucial enabling tool: a specialised Trade Finance & FX Hedging Facility, established as a joint venture between GCC and Egyptian commercial banks. This facility would offer two core products. First, accessible, multi-currency lines of credit to finance the trade flows generated by the other two initiatives. Second, it would provide affordable, long-term currency hedging instruments.

By mitigating the foreign exchange risk for GCC investors repatriating profits and for Egyptian exporters managing costs, this facility removes a key source of friction. This facility requires a direct government and central bank catalyst. The Central Bank of Egypt (CBE), in coordination with its GCC counterparts, can provide a crucial liquidity backstop or favorable swap lines to participating commercial banks, lowering their cost of funds and enabling more competitive financing rates. Furthermore, the government can provide sovereign guarantees on a portion of the trade finance extended to SMEs through this facility, expanding the pool of eligible companies and encouraging commercial banks to lend to a segment they might otherwise deem too risky. This proactive de-risking by the state is essential to get a private sector-led facility off the ground.

3.4. Pillar III: The Logistical and Digital Architecture: The ‘Green Lane’ Digital Corridor

The analysis reveals that the primary logistical challenge between Egypt and the GCC is a crippling “information deficit” and a high degree of procedural friction. The corridor is characterised by opaque and paper-intensive processes that impose immense time and cost burdens. The strategic imperative is to replace this archaic system with a digital corridor. This requires moving beyond optimising individual ports to creating an integrated, end-to-end ecosystem.

3.4.1. Digital AEO Green Lane

Traditional Authorised Economic Operator (AEO) or trusted trader programmes are a step in the right direction, but they are often siloed nationally and their benefits are not always realised in practice at the destination port, still requiring manual checks and paperwork. The first step is to create a joint, digitally-native GCC-Egypt Trusted Partner status. This status would be programmatically linked to the “Industrial Opportunity Platform”. A pre-vetted Egyptian supplier on the platform would automatically be eligible for this tier. Crucially, their certification and all required shipping documentation on a secure digital ledger. When a shipment from a “Trusted Partner” leaves a departure port, its digital credentials are automatically and instantly transmitted to customs officials in the arrival port. This allows for true pre-arrival clearance, with the system flagging the shipment for a green lane upon arrival. This transforms customs from a bureaucratic hurdle into a simple, predictable tollgate.

3.4.2. Interoperability Bridge for Connecting National Single Windows

Most countries have invested heavily in their own national “Single Window” customs platforms (e.g., Egypt’s Nafeza,[15] KSA’s Fasah,[16] and UAE’s Dubai Trade[17]). These are powerful domestic systems, but they often do not communicate well with each other, forcing exporters and freight forwarders into manual data entry for each leg of the journey. Instead of attempting to build a single, monolithic super-system, the far more pragmatic approach is to begin by building bilateral secure Interoperability Bridges that can later be expanded. A focused, bilateral pilot programme between high-volume ports, for instance, between Egypt’s Nafeza and Saudi Arabia’s Fasah, would be launched. This would include mapping core data fields (e.g., shipper, consignee and vessel number) and develop mechanisms for the two systems to communicate. When an exporter files their manifest on Nafeza, the essential data is automatically pushed to Fasah. Saudi customs can then perform risk assessment and even issue preliminary clearance while the vessel is still in transit. This single step eradicates the information lag that is responsible for a significant portion of port dwell time and associated costs. This system can be expanded to include multiple ports to communicate with each other.

3.4.3. Predictive Logistics Platform

Strategic agreements between key logistical hubs, like the MOU between Egypt’s Suez Canal Economic Zone (SCZONE) and Oman’s Special Economic Zone Authority at Duqm (SEZAD), are rich in potential but often remain dormant due to a lack of operational integration. The key to activating this corridor is to provide predictability. This can be achieved by launching a Predictive Logistics Platform. Using data from containers, real-time vessel tracking and port terminal information, the platform would provide all parties in the supply chain with a single source of highly accurate, dynamic Estimated Time of Arrival (ETA). This transparency will be revolutionary. It allows an importer in the Gulf to shift from a costly “just-in-case” inventory model to a lean “just-in-time” model, unlocking immense working capital. It transforms the physical corridor from a simple shipping lane into a reliable, intelligent and financially attractive supply chain model, a powerful incentive for businesses to shift their trade flows onto this route.

Conclusion

This study demonstrates that the paradox of the Egypt–GCC economic relationship—characterised by high strategic alignment yet limited industrial integration—is not a predetermined outcome, but the result of a structural gap: the “missing middle”. While sovereign capital flows and basic commodity trade exist, the connective tissue required for deep value-chain integration—robust institutions, financial mechanisms, and logistics infrastructure—remains largely absent.

The consequences of this inertia are measurable. Over US$3 billion in potential annual exports remain unrealised due to regulatory divergence, logistical friction, and the prevailing investment bias toward non-tradables, particularly real estate. These patterns reinforce dependency rather than foster partnership, leaving Egypt vulnerable to external shocks and regulatory barriers, such as Saudi Arabia’s localisation mandates or the UAE’s re-export hub dynamics.

Correcting this asymmetry is a strategic imperative. In a rapidly shifting global order, characterised by intensified US–China competition and the expansion of the BRICS+ bloc, the Egypt–GCC corridor must leverage its combined strengths: Gulf capital and energy resources, alongside Egyptian labor and industrial depth. The opportunity lies in moving beyond the “Farm and Quarry” model towards genuine industrial co-creation.

This transition requires both internal and external reforms. Domestically, Egypt must dismantle bureaucratic barriers, empower the private sector, and align investment incentives with industrial development. Externally, the GCC states and Egypt must construct institutional, financial, and logistical architectures to facilitate value-chain integration. Policy tools such as co-investment platforms, market-creation taskforces, and digital trade corridors could operationalise this vision.

Ultimately, the sustainability and strategic value of the Egypt–GCC relationship will be measured not by capital inflows or real estate projects, but by the density and resilience of integrated industrial supply chains. The foundation for this transformation exists—the political will and financial resources are present. The task ahead is to build the architecture that converts alignment into shared industrial capacity, ensuring a durable and mutually beneficial partnership.

Annexure

(Data used for all the appended tables are from the International Trade Centre: https://www.trademap.org/Index.aspx.)

Ahmed Dawoud is Head, Data Analytics Unit, Egyptian Center for Economic Studies (ECES).

Samriddhi Vij is Associate Fellow, Geopolitics, ORF Middle East.

All views expressed in this publication are solely those of the authors, and do not represent the Observer Research Foundation, either in its entirety or its officials and personnel.

Endnotes

[a] The 2011 revolution marked the end of the Mubarak era and triggered severe macroeconomic instability—including capital flight, a collapse in tourism revenues, and a sharp decline in foreign reserves—creating Egypt’s structural dependence on GCC financial support in the years that followed.

[b] See Annexure, Table 7 and Table 2.

[c] See Annexure, Table 7.

[d] See Annexure, Table 3.

[e] See Annexure, Table 6.

[f] See Annexure, Table 1.

[g] See Annexure, Table 7.

[h] See Annexure, Table 3.

[i] See Annexure, Table 12.

[j] See Annexure, Table 17.

[k] See Annexure, Table 22.

[l] See Annexure, Table 27.

[1] International Trade Centre, “Export Potential Map: Egypt–GCC Countries Data,” ITC, 2025, https://exportpotential.intracen.org/en/

[2] Mohammed Al-Jadaan (Saudi Finance Minister), remarks at the World Economic Forum, Davos, January 2023, cited in “Why Unconditional Gulf Financing for Egypt Is Dwindling,” The New Arab, February 15, 2023, https://www.newarab.com/analysis/why-unconditional-gulf-financing-egypt-dwindling

[3] ADQ, “ADQ-Led Consortium to Invest USD 35 Billion in Egypt,” ADQ, February 2024, https://www.adq.ae/newsroom/adq-led-consortium-to-invest-usd-35-billion-in-egypt/

[4] General Authority for Investment and Free Zones (GAFI), Annual Investment Report 2023/2024 (Cairo: GAFI, 2024), https://www.gafi.gov.eg/

[5] GAFI, Annual Investment Report 2023/2024

[6] Keninstitute, “Green Hydrogen Projects in Oman and Egypt: Mechanical Systems Behind the Revolution”, keninstitute, https://keninstitute.com/green-hydrogen-projects-in-oman-and-egypt-mechanical-systems-behind-the-revolution/

[7] Lara Moussa et al., “Impact of Water Availability on Food Security in GCC: Systematic Literature Review-Based Policy Recommendations for a Sustainable Future,” Environmental Development 54, no. 9 (2024), https://doi.org/10.1016/j.envdev.2024.101122

[8] Mysteel, “Alba Chooses Egypt for Its First Alumina Refinery,” Mysteel, 2025, https://www.mysteel.net/news/5097806-alba-chooses-egypt-for-its-first-alumina-refinery

[9] Ministry of Economy and Planning, Kingdom of Saudi Arabia, “Accelerating the Economic Transformation of Saudi Arabia through Investments,” 2024, https://mep.gov.sa/files/en/KnowledgeBase/EconomicReports/Documents/Ministry%20of%20Economy%20&%20Planning%20-%20Investment%20Report.pdf

[10] Karim Tolba, “Powerlist: Top Ports in the Middle East,” Logistics Middle East, 2022, https://www.logisticsmiddleeast.com/news/top-middle-east-ports

[11] Afaq Hussain and Nicholas Shafer, “The India–Middle East–Europe Economic Corridor: Connectivity in an Era of Geopolitical Uncertainty,” Atlantic Council, 2025, https://www.atlanticcouncil.org/in-depth-research-reports/report/the-india-middle-east-europe-economic-corridor-connectivity-in-an-era-of-geopolitical-uncertainty/

[12] Chen, “Strategic Synergy between Egypt ‘Vision 2040’ and China’s ‘Belt and Road’ Initiative,” Outlines of Global Transformations: Politics, Economics, Law 11, no. 5 (2018), https://doi.org/10.24942/2542-0240-2018-11-5-219-245

[13] International Trade Centre, “Export Potential Map: Egypt–GCC Countries Data,” ITC, 2025, https://exportpotential.intracen.org/en/

[14] International Trade Centre, “Trade Map: Bilateral Trade Statistics,” ITC, 2024, https://www.trademap.org/Index.aspx

[15]Nafeza, “National Single Window for Trade ‘Nafeza’”, https://www.nafeza.gov.eg/en

[16] Fasah, https://www.fasah.sa/trade/home/en/

[17] Dubai Trade, https://www.dubaitrade.ae/en/