Commentaries | 16 April, 2026

Has the Iran War Triggered Another Semiconductor Crisis?

The looming threat of a helium shortage amid the Iran war, coupled with a global memory chip crisis, underscores the urgent need to diversify semiconductor supply chains

The COVID-19 pandemic exposed the intricate and fragile nature of the global semiconductor supply chain. That shock prompted major powers to reassess their technology development strategies and brought the issue of technological and supply chain sovereignty to the forefront. Now, amid a massive global push to restructure supply chains, the Iran war has sparked fresh concerns about another potential crisis. The conflict is gradually contributing to shortages of a critical element underpinning the semiconductor manufacturing ecosystem: helium. This comes on top of an existing and widespread memory chip shortage, driven by surging AI data centre demand. While each factor alone is cause for concern, their combined impact could have severe ramifications for semiconductor and broader technology supply chains in the near future. Together, they reiterate the pressing need to strengthen and diversify supply chains.

The closure of the Strait of Hormuz, accompanied by multiple Iranian attacks on QatarEnergy’s Ras Laffan Industrial City, the world’s largest LNG export facility, has effectively halted production and shipping. This poses a significant risk to future global helium supply.

The Iran War and Its Impact on Helium Supply

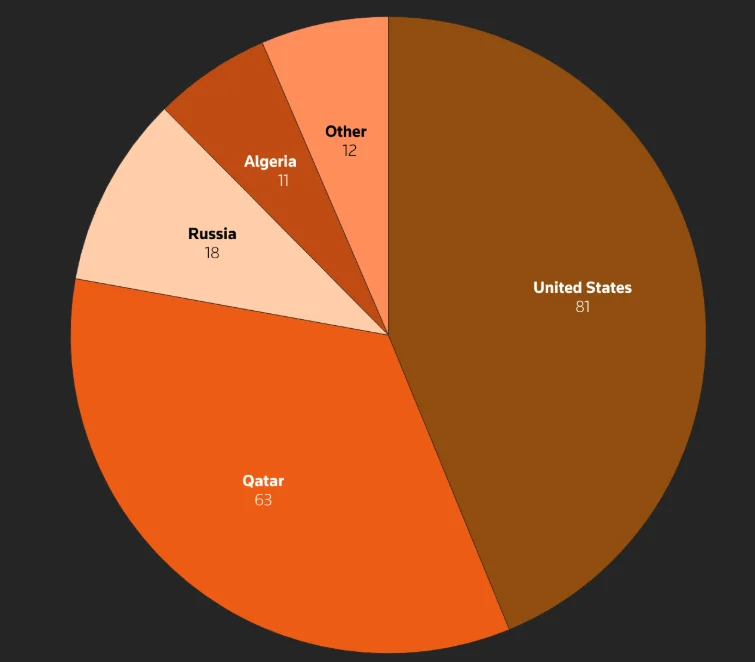

Semiconductor fabrication relies heavily on helium, particularly during the etching process. Over time, this dependence has made the semiconductor industry the gas’s largest global consumer. Helium, however, is largely obtained as a waste gas from liquefied natural gas (LNG) plants. Qatar provides nearly 34 percent of the global supply via three plants, two of which utilise LNG byproducts. The closure of the Strait of Hormuz, accompanied by multiple Iranian attacks on QatarEnergy’s Ras Laffan Industrial City, the world’s largest LNG export facility, has effectively halted production and shipping. This poses a significant risk to future global helium supply.

Figure 1: Global Helium Production in 2025 (in million cubic metres)

Source: Reuters

Though helium spot prices have already shot up, this is not an immediate concern because the industry largely operates on long-term contracts. Moreover, the oversupply of preceding years is effectively acting as a cushion against short-term shocks. However, a prolonged shortage will likely force suppliers to declare force majeure on their contract customers. While this is a concern for all major semiconductor manufacturers, it is particularly worrisome for Taiwan and South Korea, both of which procure the majority of their helium supplies from Gulf Cooperation Council (GCC) nations.

The Memory Chip Supply Crunch

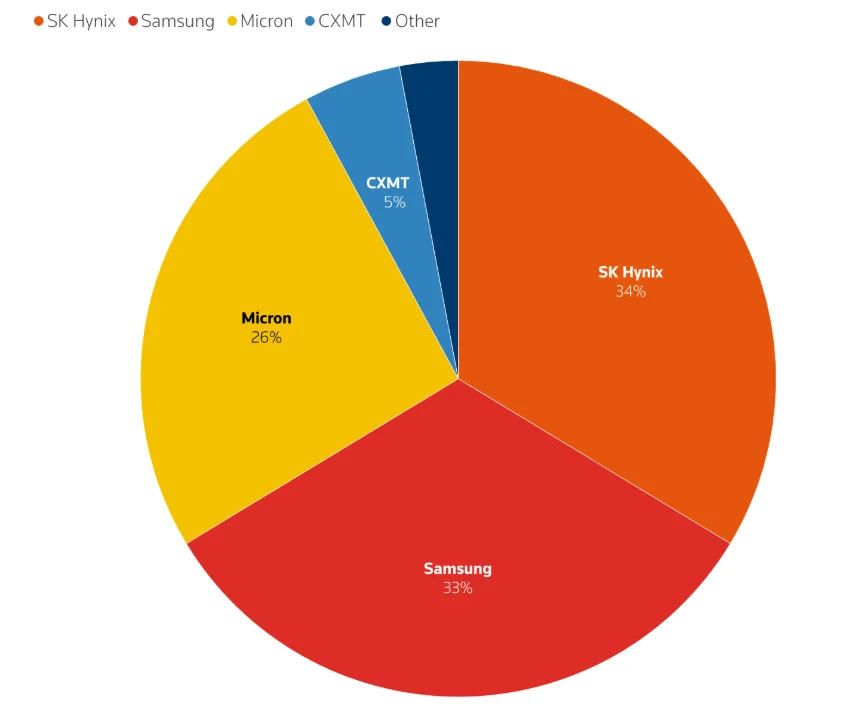

Memory chips constitute one of the most critical categories of semiconductors, forming a cornerstone of modern digital and consumer electronics. However, the prevailing supply chain model, established over multiple decades, led to the concentration of memory chip manufacturing largely in three companies: South Korean giants Samsung Electronics and SK Hynix, along with the US-based Micron Technology. Collectively, they account for over 90 percent of the dynamic random-access memory (DRAM) market.

Figure 2: DRAM Market Share by Revenue

Source: Reuters

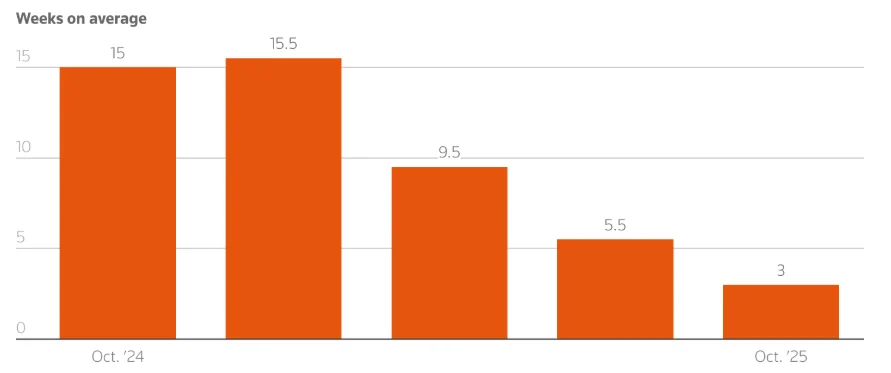

With the rapidly accelerating demand for high-bandwidth memory (HBM), driven by global hyperscaler AI data centres, all major memory chip manufacturers have gradually shifted production toward HBM. However, due to a much more complex manufacturing process, HBM chip yields are lower than those of DRAM, and its expansion has come at the cost of DRAM manufacturing capacity and efficiency. This shift has created a supply chain chokepoint for traditional memory chips used in consumer electronics such as smartphones and PCs. As a result, DRAM inventory levels have declined, accompanied by steep price increases over the past year.

Figure 3: Decline in Average DRAM Supplier Inventory Levels

Source: Reuters

Furthermore, the shortage presents a broader macroeconomic risk: it threatens to derail billions of dollars’ worth of digital infrastructure investments committed by AI hyperscalers. While both Samsung and SK Hynix have committed investments to expand memory chip capacity, the latter has indicated that the shortfall is expected to last at least until 2027.

Compounding Disruptions

While each of the above factors is sufficient cause for concern in isolation, their convergence could have severe consequences for technology supply chains and national economies in the near future. An example is already playing out in South Korea, where the stock market plummeted by over 12 percent on March 4, 2026, its worst drop in history.

An impending helium shortage in the coming months could further escalate the situation, leading to an even larger global memory chip supply crunch.

South Korean industry, including semiconductor manufacturing, is heavily reliant on fossil fuels, with over 70 percent of its crude oil imported from the Middle East, largely through the Strait of Hormuz. With Samsung and SK Hynix collectively accounting for 80 percent of the HBM market and 70 percent of the DRAM market, disruptions could trigger cascading effects across the global economy. This risk is amplified by growing investments from AI hyperscalers and steadily rising demand for consumer electronics. An impending helium shortage in the coming months could further escalate the situation, leading to an even larger global memory chip supply crunch.

Rethinking the Architecture of Tech Supply Chains

The supply shortages triggered by the COVID-19 pandemic prompted a near-universal push to diversify semiconductor supply chains. However, these efforts come after nearly four decades of deep, globalisation-led economic interdependence. As such, it will likely be a while before these initiatives can fully materialise. During this period of transition, the industry remains ill-prepared to absorb supply chain shocks, whether from rapidly escalating demand driven by technological innovation or from large-scale regional conflicts that disrupt critical trade routes.

Although this does spell trouble for the global economy in the short run, it nevertheless serves to underscore the importance of ongoing supply chain diversification initiatives, placing a reminder on their criticality. Simultaneously, it places renewed responsibility on emerging manufacturing hubs such as India, which recently inaugurated its first Assembly, Test, Marking, and Packaging (ATMP) facility in partnership with Micron.

As the global semiconductor supply chain evolves, these new entrants will play a critical role in stabilising markets against future shocks and disruptions. In the meantime, the industry is left grappling with the remnants of a largely profit-centric offshoring model, one whose failures should serve as a crucial reminder when formulating the tech supply chains of the future.

Prateek Tripathi is an Associate Fellow with the Centre for Security, Strategy and Technology (CSST) at the Observer Research Foundation.