Expert Speak | 30 May, 2026

Global South in the Crossfire: Strategic Competition and Managed Interdependence

The following excerpt is from Chapter 6 — New Arenas of Great-Power Competition of ORF Global Quarterly: Disruption and Recalibration.

The Global South is no longer a peripheral arena in United States (US)-China competition. Trade, technology, industrial policy, logistics corridors, and development finance have become instruments through which strategic rivalry is projected outward.[1] For countries across Asia, Africa, and Latin America, the challenge is no longer simply how to engage Washington or Beijing diplomatically, but how to preserve developmental autonomy in an environment where great-power competition is restructuring markets, supply chains, and industrial choices.

India sits at the heart of this dilemma. Its relationship with China is economically consequential, politically sensitive, and strategically constrained. Bilateral merchandise trade remains substantial yet deeply imbalanced, with Chinese capital goods, intermediates, and processed inputs embedded across Indian manufacturing.[2] Yet the relationship is no longer understood in New Delhi solely through a commercial lens. Since 2020, the security environment has hardened, prompting India to pay closer attention to how concentrated dependence in critical sectors can constrain autonomy under stress. The result is neither wholesale rupture nor effortless coexistence but rather managed interdependence under strategic competition: keeping commercial channels open where growth requires them, tightening guardrails where vulnerability is too high, and diversifying wherever feasible.

That wider logic is now visible across the Global South. Indonesia faces rising imports of Chinese steel and textiles that undercut its own industrialisation efforts, even as it remains dependent on Chinese investment in nickel processing.[3] Vietnam, deeply integrated into China-linked electronics supply chains, is navigating pressures from both sides as US tariffs increasingly target Chinese content routed through third countries. Brazil contends with an influx of low-cost Chinesemanufactured goods, particularly in autos and steel, while remaining reliant on China as its dominant buyer of commodities.[4] South Africa, similarly, has experienced pressure on local manufacturing from Chinese consumer goods, even as Chinese demand sustains its mining sector.[5] Each case differs in specifics, but the underlying dilemma mirrors India’s challenge of capturing the benefits of Chinese economic engagement without ceding industrial ground or strategic leverage

China’s trade position is adjusting to rising tariff barriers, Western industrial policies, and slower access to mature markets by pushing more aggressively into developing economies. In the first two months of 2026, China’s exports rose 21.8 percent year-on-year, with its trade surplus reaching US$213.6 billion. It closed 2025 with a record surplus of US$1.2 trillion, as exporters increasingly redirected goods toward Southeast Asia, Africa, and Latin America.[6] As the past year witnessed US tariffs on Chinese goods escalate to historically high levels, Beijing responded with export controls on critical minerals and retaliatory duties. The combined effect of these measures has squeezed Global South economies between costlier imports, disrupted supply chains, and narrowing market access for their own exports. At the same time, the Gulf crisis, triggered by the US-Israeli strikes on Iran in February 2026 and Iran’s subsequent closure of the Strait of Hormuz, has heightened concerns over shipping, energy prices, and trade-route vulnerability, particularly for import-dependent economies such as India.[7]

This essay frames US-China strategic competition and China’s export surge to the Global South as two dimensions of the same geoeconomic transformation. The first establishes the strategic context: rising tariffs, technology controls, industrial subsidies, and selective decoupling that are fragmenting the global trading system. The second illustrates how that fragmentation is absorbed elsewhere: as access to advanced markets becomes more contested, Chinese goods, capital, and industrial capacity are increasingly redirected into developing economies. These trends demonstrate that the Global South is no longer merely responding to great-power rivalry but is increasingly becoming the arena where the economic consequences of that rivalry are being redirected, negotiated, and contested.

China’s Export Push and the Reordering of Developing-Country Markets

The US is shaping the development landscape of the Global South, through a distinct set of instruments. While China’s presence remains market-deep and trade-heavy, Washington’s approach is more selective, standards driven, and security-inflected. It involves friend-shoring through regional supply-chain arrangements, export controls on sensitive technologies, development finance through the US International Development Finance Corporation, coordination in critical minerals through the Minerals Security Partnership, AI and semiconductor supply-chain alignment through the Pax Silica initiative launched in December 2025, and clean-energy platforms such as the Clean Energy Demand Initiative. This has resulted in a reconfiguration, not a retreat, of US influence—shifting from broad market access toward targeted corridor-building, trusted supply chains, and strategic sectors.

The geography of economic competition has shifted. Rather than simply decoupling from one another, the US and China are seeking to shape the external environment in which others trade, invest, and industrialise. China’s response to tariffs, export controls, and industrial pressure has not been retreat[8] but an outward commercial push, particularly toward developing markets where demand for affordable manufactures, green technologies, digital hardware, and industrial machinery remains strong. For many Global South economies, this makes China more than a supplier and instead a structuring force in development choices.

The Global South is no longer merely responding to great-power rivalry but is increasingly becoming the arena where the economic consequences of that rivalry are being redirected, negotiated, and contested.

The Global South has become central to China’s export strategy for structural reasons. Demand in many advanced economies is weakening, trade barriers are rising, and the politics of overcapacity have intensified. In contrast, developing economies continue to absorb growing volumes of industrial inputs, consumer goods, digital equipment, and transition technologies. This makes them attractive not only as markets, but also as political and strategic constituencies in a shifting trade order. For importing economies, this creates a double-edged reality where goods can lower costs, support infrastructure expansion, accelerate renewable deployment, and relieve supply shortages. Yet they may also arrive at a pace and scale that domestic industries struggle to absorb. When Chinese export surges enter economies with shallow supplier bases, they can widen trade deficits, compress local margins, and complicate the execution of industrial policy.

India’s case is instructive because it shows why this is not a straightforward story of dependence versus resistance. India still relies on Chinese inputs across electronics, machinery, chemicals, renewables, and pharmaceuticals.[9] In a region where production is fragmented across multiple stages, diversification does not necessarily mean replacing China; more often, it means reconfiguring exposure while continuing to operate within value chains where China remains the dominant upstream node. That is why India’s policy is beyond decoupling, and rather an effort to separate developmental necessity from strategic overexposure.

Dependence, Deficits, and the Sectoral Politics of Exposure

A bilateral trade deficit is not inherently exploitative; in fragmented production system, it often reflects value-chain position rather than simple unfairness.[10] Yet deficits become politically and strategically salient when they are large, persistent, and concentrated in sectors that are difficult to substitute. That is why India’s deficit with China matters: it is not merely a macroeconomic issue, but a map of industrial vulnerability.

The key question is composition. Dependence on final consumer goods is one thing; dependence on intermediates, machinery, chemicals, APIs, and critical inputs is another. The more deeply Chinese products are embedded in domestic production, the harder it becomes to absorb disruption without wider economic costs. For India, this vulnerability is especially visible in electronics, renewable energy, pharmaceuticals, and heavy industrial equipment. The issue is less whether trade exists and more of particular forms of trade risk becoming crisis multipliers.

This is also where China’s export surge into the Global South assumes wider significance. Cheap imports may support downstream manufacturing and accelerate access to green technologies, but if they overwhelm domestic firms before local ecosystems mature, they risk trapping countries in a cycle where industrialisation remains shallow and import dependence deepens. The politics of dependence, therefore, is not about rejecting imports but about managing their pace, sectoral concentration, and developmental consequences.

Not all dependence is economically equivalent. Consumer-goods dependence is usually the least binding; it affects prices, inflation, and household welfare, but substitute suppliers can often be found with manageable adjustment costs. Intermediate-goods dependence is more consequential as it is transmitted through production networks—disruptions here can slow domestic output, delay exports, and propagate cost shocks across sectors. Strategicinput dependence is the most significant. Where imports are tied to health security, digital systems, energy transition hardware, or critical minerals, the central issue is not efficiency but continuity, bargaining power, and resilience under stress.

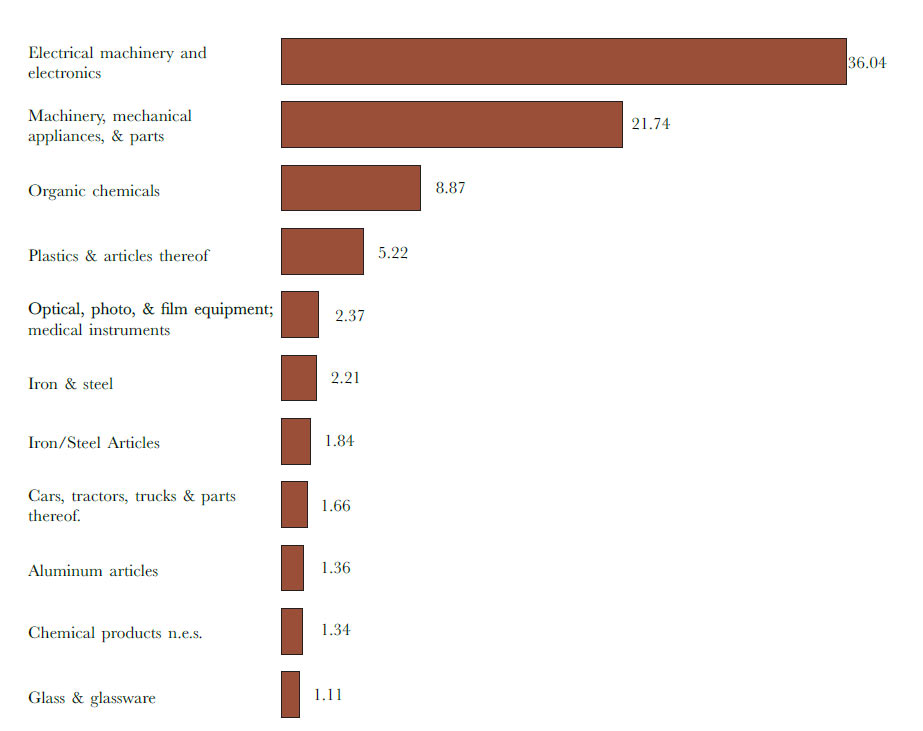

Figure 1: Composition of India’s Imports from China, by Product Category (2024)

Source: Observatory of Economic Complexity[11]

China’s export push into the Global South is not uniform. In solar modules and batteries, China’s scale lowers the cost of energy transitions for developing countries. In industrial machinery and electronics, it supports manufacturing expansion where local capabilities remain limited. In telecommunications equipment and digital systems, however, the issue is not only price but trust, auditability, and infrastructure integrity. In steel, chemicals, and consumer manufactures, Chinese scale can easily become a source of competitive pressure for weaker industrial ecosystems.

The current Gulf crisis sharpens this dynamic. Rising oil prices and disrupted shipping routes have increased the urgency of energy diversification across the Global South, which is likely to accelerate demand for Chinese solar modules, wind turbines, and battery storage.

Yet, this same acceleration deepens supplychain concentration risks: China currently accounts for over 80 percent of global solar module manufacturing and dominates lithiumion battery cell production.[12] A crisis-driven rush to deploy renewables sourced overwhelmingly from a single supplier could exchange one form of energy vulnerability (fossil-fuel dependence routed through contested sea lanes) for another (concentrated dependence on Chinese cleanenergy hardware) at a moment when Beijing’s willingness to use economic leverage is itself under scrutiny.

For India, this sectoral variation is critical. Chinese strength in upstream clean-energy components can advance India’s decarbonisation goals while simultaneously complicating indigenous manufacturing. Chinese machinery helps sustain industrial output but reinforces supplier dependence. Telecom and digital systems raise sharper strategic concerns because the risks involve system control, data integrity, and continuity under stress; which are ultimately questions of technological sovereignty, rather than of mere import competition.[13] Not all dependencies carry the same weight, and a serious policy response must therefore be differentiated, pragmatic, and non-ideological.

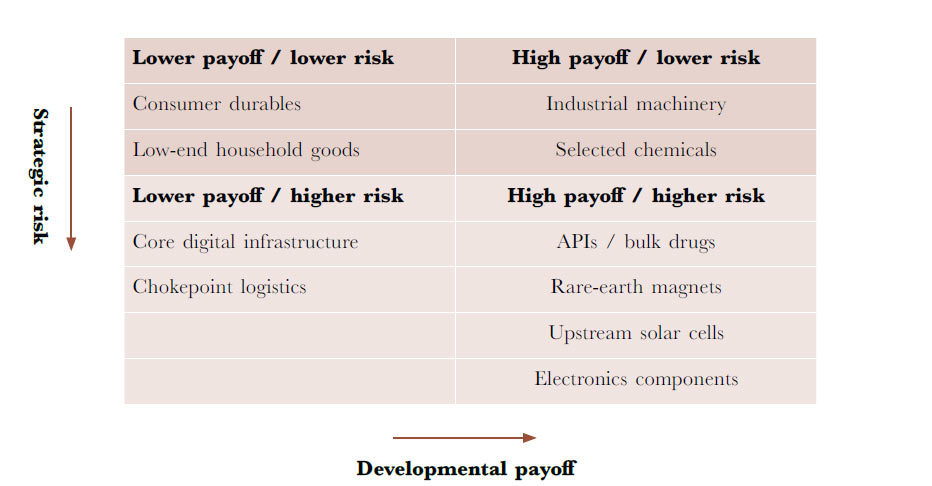

Figure 2: Development and Strategic Risk Trade-offs, Select Sectors

Source: Authors’ own

India’s Response: Managed Interdependence in Practice

India’s response has evolved into a layered toolkit built on three pillars: capability building, rule enforcement, and strategic guardrails. First, industrial policy, especially production-linked incentives, aims to draw supplier ecosystems onshore, deepen value addition, and gradually reduce dependence on single sources. Second, standards, conformity requirements, and trade remedies shape import composition and create space for domestic scaling. Third, strategic hardening targets sectors with especially high failure costs, including telecom, sensitive digital systems, data-rich platforms, and critical infrastructure. This is not a push for autarky, but an effort to reduce risky, weaponisable dependence by accepting limited continued reliance on Chinese inputs while diversifying exposure and tightening controls in sensitive areas.

The limitations of India’s policy toolkit are equally important and should be factored into the analysis. The Performance Linked Incentive (PLI) scheme has been effective in attracting investment, scaling assembly operations, and improving export performance, particularly in electronics.[14] However, deeper upstream localisation remains incomplete in components, materials, and process technologies. Standards and conformity requirements can create policy space for domestic firms, yet they also impose compliance costs and may slow diffusion when local capacity is limited.[15]

Chokepoints, Coercion, and the Gulf Shock

Developing countries face a policy dilemma: Chinese exports can provide affordable infrastructure and clean technology essential for rapid growth, but they can also undermine domestic industry and create long-term strategic dependence if left unmanaged. India reflects this broader Global South challenge, as it seeks to leverage low-cost Chinese inputs to support development while simultaneously mitigating excessive vulnerability in an increasingly coercive global environment.

The key lesson from across the developing world is that the real issue is not imports themselves, but the policy context within which they are absorbed. Pakistan’s solar expansion demonstrates how Chinese scale can accelerate development by reducing costs and expediting deployment, while South Africa’s experience illustrates that high import penetration may suppress manufacturing employment, constrain sales growth, and undermine firm survival. Ultimately, Chinese trade is beneficial only when it reinforces domestic capability-building rather than displacing it before it can mature.[16]

Developing countries face a dilemma: Chinese exports can provide affordable infrastructure and clean tech essential for rapid growth, but they can also undermine domestic industry and create long-term strategic dependence.

The most serious risk in India’s relationship with China is not a blanket collapse of trade, but selective coercion through chokepoints. When dependence is concentrated in processed materials, critical minerals, Active Pharmaceutical Ingredients (APIs), electronics components, or other hard-to-substitute intermediates, even narrow restrictions can cascade into broader production losses.[17] India’s resilience strategy has therefore evolved in two directions: targeted domestic capacity creation in identified bottleneck sectors, and diversification through trusted partnerships in critical minerals, advanced manufacturing, and supply-chain resilience.

The challenge for India and much of the Global South is increasingly one of dual derisking: reducing concentrated exposure not only to China but also to the US. Washington’s willingness to deploy tariffs, sanctions, and technology restrictions against partners as well as adversaries means that over-alignment with either pole introduces distinct vulnerabilities. A policy architecture built around a single axis of dependence reduction risks substituting one source of coercive leverage for another. Genuine strategic autonomy, therefore, requires diversifying supply chains, technology partnerships, and market access away from both major powers simultaneously. Although politically more difficult, this remains the only approach capable of safeguarding developmental flexibility in an era when economic statecraft is exercised from multiple directions.

The Gulf crisis has made clear that India’s vulnerability is not confined to bilateral dependence, but extends to a wider system in which China-related supply chains, maritime chokepoints, energy flows, and trade logistics are tightly interconnected. Disruption in the Strait of Hormuz affects not only oil supplies, but also freight rates, insurance costs, delivery schedules, inventory management, and the viability of just-in-time production across import-dependent economies.[18] For India, this implies that de-risking from China cannot be separated from reducing exposure to maritime and energy disruptions. Strategic autonomy, therefore, is no longer only about tariffs, incentives, or diplomacy, but also about strengthening systemic resilience through secure shipping routes, expanded storage capacity, and alternative trade corridors.

Conclusion: Strategic Autonomy in an Age of Redirected Rivalry

US–China strategic competition is increasingly reshaping the Global South, as the contest now extends well beyond tariffs and summit diplomacy to encompass production, supply, finance, and the absorption of industrial surplus. China’s export surge into the Global South is therefore not merely a trade trend, but part of a wider reordering of global commerce shaped by tariff fragmentation, industrial overcapacity, and geopolitical pressures. India’s response provides a useful lens on this shift: it has neither embraced full decoupling nor accepted passive dependence, but instead pursued managed interdependence—remaining open where growth requires it, building domestic capability where substitution is feasible, and imposing guardrails where dependence becomes strategically risky.

Gaps still exist. Domestic capability-building in semiconductors, advanced chemicals, and critical minerals processing is still at an early stage, and PLI-supported manufacturing has not yet achieved the scale or cost-competitiveness required to reduce import dependence in most targeted sectors. Diversification of supply chains away from China has advanced only gradually, as alternative sourcing from Vietnam, South Korea, or Japan remains limited in volume and is frequently more prohibitive. Regulatory enforcement against circumvention, including transhipment and under-invoicing, has been inconsistent. Moreover, India has yet to articulate a coherent framework for dual de-risking that addresses vulnerability to US economic statecraft alongside Chinese leverage. Managed interdependence, in other words, is a credible strategic direction, but one whose implementation continues to lag behind its stated ambition.

The pressures of 2026 only reinforce this logic. China’s export surge, weak global trade growth, and the Gulf crisis together underscore an increasingly volatile external environment in which diverted trade, energy shocks, and coercive leverage can reinforce one another. For India and the wider Global South, the task is not to choose sides in great-power rivalry, but to develop sufficient industrial depth, logistical resilience, and policy autonomy to prevent that rivalry from determining development outcomes. The challenge, therefore, is not disengagement from China, but disciplined engagement on terms that safeguard developmental agency: importing where it lowers transition costs, diversifying where concentration is dangerous, and building domestic depth where external dependence is susceptible to coercion.

Soumya Bhowmick is Fellow, Centre for New Economic Diplomacy (CNED), Observer Research Foundation.

Arya Roy Bardhan is Junior Fellow, CNED, Observer Research Foundation.

[1] Henry Farrell and Abraham L. Newman, “Weaponized Interdependence: How Global Economic Networks Shape State Coercion,” International Security 44, no. 1 (2019): 42–79,https://www.jstor.org/stable/10.2307/26777882.

[2] India Brand Equity Foundation, “China Overtakes US as India’s Top Trading Partner in FY24: GTRI,” IndBiz, May 13, 2024,https://indbiz.gov.in/china-overtakes-us-as-indias-top-trading-partner-in-fy24-gtri.

[3] Brendan Kelly and Shay Wester, “ASEAN Caught Between China’s Export Surge and Global De-Risking,” Asia Society Policy Institute, February 20, 2025, https://asiasociety.org/policy-institute/asean-caught-between-chinas-export-surgeand- global-de-risking.

[4] Lucas Lorimer, “Brazil Plans Response as Steel Sector Hit by Chinese Imports and U.S. Tariffs,” Datamar News, December 11, 2025, https://datamarnews.com/noticias/brazil-plans-response-as-steel-sector-hit-by-chinese-imports-and-u-stariffs/.

[5] Marvellous Ngundu, “South Africa’s Trade Deficit Dilemma with China,” Institute for Security Studies, March 5, 2025, https://issafrica.org/iss-today/south-africa-s-trade-deficit-dilemma-with-china.

[6] Joe Cash, “China’s Exports Turbocharge into 2026 after Record-Breaking Year,” Reuters, March 10, 2026, https://www. reuters.com/world/asia-pacific/chinas-exports-turbocharge-into-2026-after-record-breaking-year-2026-03-10/.

[7] United Nations Conference on Trade and Development (UNCTAD), “Hormuz Shipping Disruptions Raise Risks for Energy, Fertilizers and Vulnerable Economies,” March 10, 2026, https://unctad.org/press-material/hormuz-shippingdisruptions- raise-risks-energy-fertilizers-and-vulnerable-economies.

[8] Tatjana Schulze and Weining Xin, Demystifying Trade Patterns in a Fragmenting World, IMF Working Paper No. 2025/129 (Washington, DC: International Monetary Fund, June 27, 2025), https://www.imf.org/en/publications/wp/ issues/2025/06/27/demystifying-trade-patterns-in-a-fragmenting-world-567071.

[9] Ministry of Commerce and Industry, Government of India, “Unstarred Question No. 4948: Trade with China,” Lok Sabha, April 1, 2025,https://www.commerce.gov.in/wp-content/uploads/2025/04/LS-USQ-No.4948- dated.-01.04.2025-1.pdf.

[10] Organisation for Economic Co-operation and Development (OECD) and World Trade Organization (WTO), Trade in Value Added: OECD–WTO Database Brochure, January 2013, https://www.wto.org/english/res_e/statis_e/miwi_e/ tradedataday13_e/oecdbrochurejanv13_e.pdf.

[11] Observatory of Economic Complexity, “India (IND) and China (CHN) Trade,” https://oec.world/en/profile/bilateralcountry/ ind/partner/chn?selector538id=HS2.

[12] International Energy Agency (IEA), Solar PV Global Supply Chains, July 2022, https://www.iea.org/reports/solar-pv-globalsupply- chains/executive-summary.

[13] Department of Telecommunications, Government of India, “Trusted Telecom Portal,” https://trustedtelecom.gov.in/.

[14] Press Information Bureau, Government of India, “Electronics Manufacturing in India Expanded Significantly in the Last 11 Years; India Emerges as the Second-Largest Mobile Manufacturer in the World,” February 6, 2026, https://www.pib. gov.in/PressReleasePage.aspx?PRID=2224503®=3&lang=2.

[15] Sudarshan Varadhan, “India Mandates Use of Locally-Made Solar Cells in Clean Energy Projects from June 2026,” Reuters, December 10, 2024, https://www.reuters.com/business/energy/india-mandates-use-locally-made-solarcells- clean-energy-projects-june-2026-2024-12-10/.

[16] Sofia Torreggiani and Antonio Andreoni, “Rising to the Challenge or Perish? Chinese Import Penetration and Its Impact on Growth Dynamics of Manufacturing Firms in South Africa,” Structural Change and Economic Dynamics 64 (2023): 199–212, https://doi.org/10.1016/j.strueco.2022.12.010.

[17] Guillaume Beaumier and Madison Cartwright, “Cross-Network Weaponization in the Semiconductor Supply Chain,” International Studies Quarterly 68, no. 1 (2024), https://academic.oup.com/isq/article/68/1/sqae003/7578750.

[18] International Energy Agency, “Strait of Hormuz,” Oil Security and Emergency Response, https://www.iea.org/about/oilsecurity- and-emergency-response/strait-of-hormuz.